India’s “Extractive Localization” Runs Into China’s Technology Export Firewall

After absorbing hard lessons from India, China is redrawing the boundary between selling products, exporting capacity, and leaking the industrial capability behind its manufacturing power.

India’s “extractive localization” has been recognized by China for what it is: not ordinary localization, but a pathway for turning Chinese capital, equipment, engineers, and process know-how into Indian industrial capability.

This essay is part of the China and the Global South Series.

Key Discussions

What happened inside Baoding Tianwei’s India venture, and why does this case matter far beyond one transformer company?

How does India’s “extractive localization” model work through market access, joint ventures, local-content rules, procurement pressure, tax scrutiny, and eventual asset transfer?

Why is the real technology in heavy industry often hidden in engineers, production routines, testing systems, training, and tacit know-how rather than patents alone?

How did Chinese equipment makers help India accelerate its solar manufacturing buildout, and why does this reveal a collective-action problem inside Chinese industry?

Why is consumer electronics another front line of extractive localization, from smartphones and ODM capability to Chinese supply-chain know-how?

How does China’s new outbound-investment regulation shift the boundary from capital-flow management to the governance of technology, data, engineers, training, and industrial capability?

Whether Chinese firms can continue globalizing without exporting the production systems that created China’s industrial advantage.

, Guanyin After Early Tang Style, 1947 - Alain.R.Truong")

Guanyin After Early Tang Style (初唐风格观音), by Zhang Daqian (张大千), 1947

Its Dunhuang-inspired Buddhist imagery mirrors the central tension of this essay: when transmission becomes absorption, and when absorption forces a civilization to redraw the boundary around what must remain under its own control.

This is not an argument against India’s industrial ambition. It is an argument about how technology transfer, localization policy, and capability leakage work in practice.

1. A Transformer Factory in Gujarat

A transformer factory is not where most people would begin a story about technology competition.

It does not have the glamour of semiconductors. It does not have the consumer visibility of smartphones. It does not have the political symbolism of rare earths. It is made of steel, copper, insulation materials, windings, oil, testing systems, thermal design, engineering drawings, supplier routines, production discipline, and technicians who know why a machine may fail before the failure appears in the data.

But that is precisely why it matters.

High-voltage transformers and reactors are not simple industrial commodities. A country cannot build them well by buying metal and machines alone. It needs design judgment, manufacturing discipline, insulation systems, winding techniques, oil processing, testing capacity, reliability validation, supplier coordination, field-service knowledge, and engineers who have learned from failures across many production cycles. In heavy electrical equipment, the most important knowledge is often not written in one patent. It is embedded in people, processes, tests, routines, and the memory of a factory.

This is why the case of Baoding Tianwei’s India venture deserves close attention.

In 2025, Baoding Tianwei announced that it would sell its 90% equity stake in Baoding Tianwei–Atlanta Transformer India Pvt. Ltd. to Atlanta Electricals for about RMB 136.82 million. The transaction looked, at first sight, like the exit of a Chinese company from a money-losing overseas subsidiary. The Indian company’s 2024 revenue had fallen to only RMB 330,000, with a net loss of RMB 12.36 million. In the first quarter of 2025, its revenue was zero, with another RMB 3.18 million in losses.

On a purely financial reading, this was an overseas investment failure.

But industrial history is not written only on income statements.

The Indian subsidiary was established in March 2012. Its registered capital was about RMB 237 million, equivalent to roughly 2.25 billion rupees. Its business scope covered the production, sale, repair, maintenance, installation, commissioning, on-site testing, renovation, upgrading, training, and consulting services for 220kV to 765kV power transformers and reactors. Its annual capacity was designed at about 11 million kVA.

This was not a sales office. It was a manufacturing and technology platform.

Baoding Tianwei had brought into India a production base for high-voltage and extra-high-voltage transformer equipment. In 2018, the Indian factory produced its first 765kV reactor, which reportedly passed testing on the first attempt. The facility was designed to serve India’s central and state-grid markets, and to support India’s growing demand for higher-voltage transmission infrastructure.

The key question is therefore not whether the Indian subsidiary made money. It is what capability entered India through that subsidiary.

2. What Atlanta Wanted

The Indian partner in this story was Atlanta Electricals, a local transformer manufacturer that had historically operated at lower voltage levels. Its own later explanation is revealing.

Atlanta’s chairman described the company’s earlier path as beginning from 66kV and then moving toward 132kV and 220kV. The ambition was to enter 400kV and eventually 765kV. That ambition could be achieved in several ways: by developing internally, by buying technology, or by entering a joint venture.

Baoding Tianwei–Atlanta provided the route.

The partnership was not merely a financial arrangement. It created a window into a higher-voltage manufacturing system. According to Atlanta’s later account, there was a clear division of territory: Atlanta would not enter 400kV and 765kV, while Baoding Tianwei–Atlanta would not enter 66kV, 132kV, and 220kV. On paper, this protected both sides.

In practice, it also placed Atlanta close to a higher-voltage production platform that it had long wanted to understand.

This is the first lesson of the case. In strategic manufacturing, a joint venture is not only a shareholding structure. It is a learning structure.

Factories teach. Engineers teach. Production problems teach. Customer requirements teach. Testing procedures teach. The partner who stands near the design process, the manufacturing process, the testing process, and the debugging process learns things that no contract fully captures.

This is why the most important sentence in the entire Baoding Tianwei case did not come from a Chinese nationalist commentator. It came from Atlanta itself.

In a later interview, Atlanta was asked whether there had been a transfer of know-how from Baoding Tianwei–Atlanta. The answer was blunt:

“The acquisition of knowhow is over.”

Atlanta further said that it had been present when transformers were being designed and manufactured at the facility, and that it could now make a 765kV transformer, though it would have to sell it under its own branding.

That sentence is the core of the story.

A Chinese company lost money. An Indian partner gained a pathway into high-voltage capability. The asset was financially distressed, but the know-how had already moved.

This is what I call extractive localization.

3. What Extractive Localization Means

Extractive localization is not ordinary localization.

Ordinary localization means that a foreign firm builds local production, hires local workers, sources local inputs where possible, serves the domestic market, and gradually contributes to the host economy. This is normal. It is legitimate. Every developing country wants some version of it. China once demanded technology transfer. South Korea, Taiwan, Japan, and many others did the same in different ways.

Extractive localization is different.

It is a model in which the host country uses market access, tax incentives, joint ventures, local-content rules, procurement pressure, regulatory leverage, and eventual asset transfer to absorb foreign industrial capability while gradually reducing the original foreign firm’s control over the capability it brought in.

The Baoding Tianwei case is a textbook example.

The Chinese firm entered India because the market was large and the power-grid opportunity looked attractive. It built a local manufacturing platform. It brought equipment, engineering knowledge, production routines, training capacity, and high-voltage know-how.

The Indian partner gained proximity to design and production. The factory suffered financially. The Chinese parent eventually exited. The Indian partner acquired control of the platform. The know-how, by the Indian partner’s own account, had already been absorbed.

The key point is not that India committed a simple legal violation. The issue is more subtle. Extractive localization often works through legal, semi-legal, and policy-mediated channels. It does not require a single dramatic act of theft. It works through proximity, time, policy pressure, local market dependence, training, production learning, regulatory asymmetry, and the final transfer of assets.

This is why it is hard to see from the outside.

A factory opens. A joint venture is formed. Engineers cooperate. Local workers are trained. The host market grows. Procurement rules change. Local-content expectations rise. The foreign firm loses money. The local partner becomes stronger. The foreign firm sells its stake. The host country keeps the capability.

Each step can be explained as ordinary business. Together, they form a transfer of industrial capability.

4. The Knowledge Was Not in One Document

The Baoding Tianwei case also shows why China’s new regulatory thinking is moving beyond patents and formal technology-transfer contracts.

The real knowledge in high-voltage equipment is not a single file. It is distributed across the whole production system.

A 765kV transformer or reactor requires design capability, materials selection, winding quality, insulation control, oil treatment, thermal management, mechanical stability, transport judgment, testing discipline, and long-term reliability. It requires the ability to diagnose what has gone wrong when something fails in testing. It requires knowledge of how to make one unit pass inspection, then how to make that repeatable at scale.

That knowledge moves through people.

It moves when Chinese engineers stand next to Indian technicians during installation. It moves when production lines are debugged. It moves when Indian engineers visit headquarters or when Chinese engineers visit India. It moves through training manuals, test data, process adjustments, procurement lists, supplier recommendations, and conversations after a failed test. It moves through the repeated correction of mistakes.

This is why Atlanta’s phrase matters so much. “The acquisition of knowhow is over” does not mean the Indian company instantly became Siemens or GE. Atlanta itself acknowledged that customers, especially major grid clients, still care about technical references and recognized technology partners. The company also noted that global giants such as GE or Siemens would not simply sell it technology.

That is exactly the point.

If Western giants would not easily sell such technology, and an Indian partner could nevertheless move toward 765kV capability through a Chinese-linked platform, then the Baoding Tianwei case shows why Chinese industrial globalization has become strategically sensitive.

The Chinese company did not simply export products. It helped create a manufacturing platform that allowed a local firm to climb the voltage ladder.

5. A Financial Failure, an Industrial Success

The ending of the case looks contradictory only if one reads it through finance alone.

For Baoding Tianwei, the Indian subsidiary became a financial burden. Revenue collapsed. Losses continued. The parent company sold its stake. From the Chinese firm’s balance-sheet perspective, the exit was understandable.

For Atlanta, however, the same asset had a different meaning. It was not merely buying a loss-making company. It was acquiring a high-voltage manufacturing platform, testing facilities, production routines, trained people, local market access, and a pathway into 765kV transformers. Later Indian commentary around the acquisition described the Jambusar facility near Vadodara as a platform capable of mass-producing 765kV transformers, with future room to move toward even higher voltage capability.

This is the asymmetry.

The Chinese firm saw a failing investment. The Indian partner saw an industrial ladder.

A Chinese factory abroad can lose money and still transfer capability. This is the hidden danger.

6. Why the New Chinese Rules Matter

This is the context in which China’s new outbound-investment regulation should be read.

It is not only a rule about money leaving China. It is not only about whether a company can invest abroad. It is about whether overseas investment becomes a channel for the transfer of strategic technology, data, services, personnel, training, and production know-how.

The new framework brings several previously separate issues into one governance perimeter: technology exports, cross-border services, data flows, personnel movement, export controls, cybersecurity, and national-security review. Most importantly, it recognizes that controlled technology can move not only through documents or machines, but through cross-border personnel dispatch, overseas work arrangements, technical guidance, and training.

This is a major conceptual shift.

For many years, Chinese firms treated these services as normal parts of globalization. Sell the equipment. Send engineers. Train local workers. Help the customer debug the line. Provide after-sales technical support. Build goodwill. Win the next order.

Now Beijing is asking a harder question:

When does after-sales support become technology transfer?

When does training become capability export?

When does an overseas joint venture become a channel for losing control of industrial know-how?

When does an asset sale transfer not only shares, but the production system itself?

The Baoding Tianwei case gives a concrete answer. By the time the equity was sold, the know-how had already moved.

7. Solar: When an Entire Industry Repeats the Pattern

Baoding Tianwei shows how one company can lose control of capability. Solar shows how an entire industry can do something similar.

The Indian solar story is not a simple tale of India defeating China. That would be too crude. China still dominates the global solar supply chain. It remains much stronger in polysilicon, wafers, cells, production equipment, process depth, cost control, and supplier ecosystems. India’s solar rise is still uneven, incomplete, and dependent on imported upstream inputs.

But the direction of travel is clear.

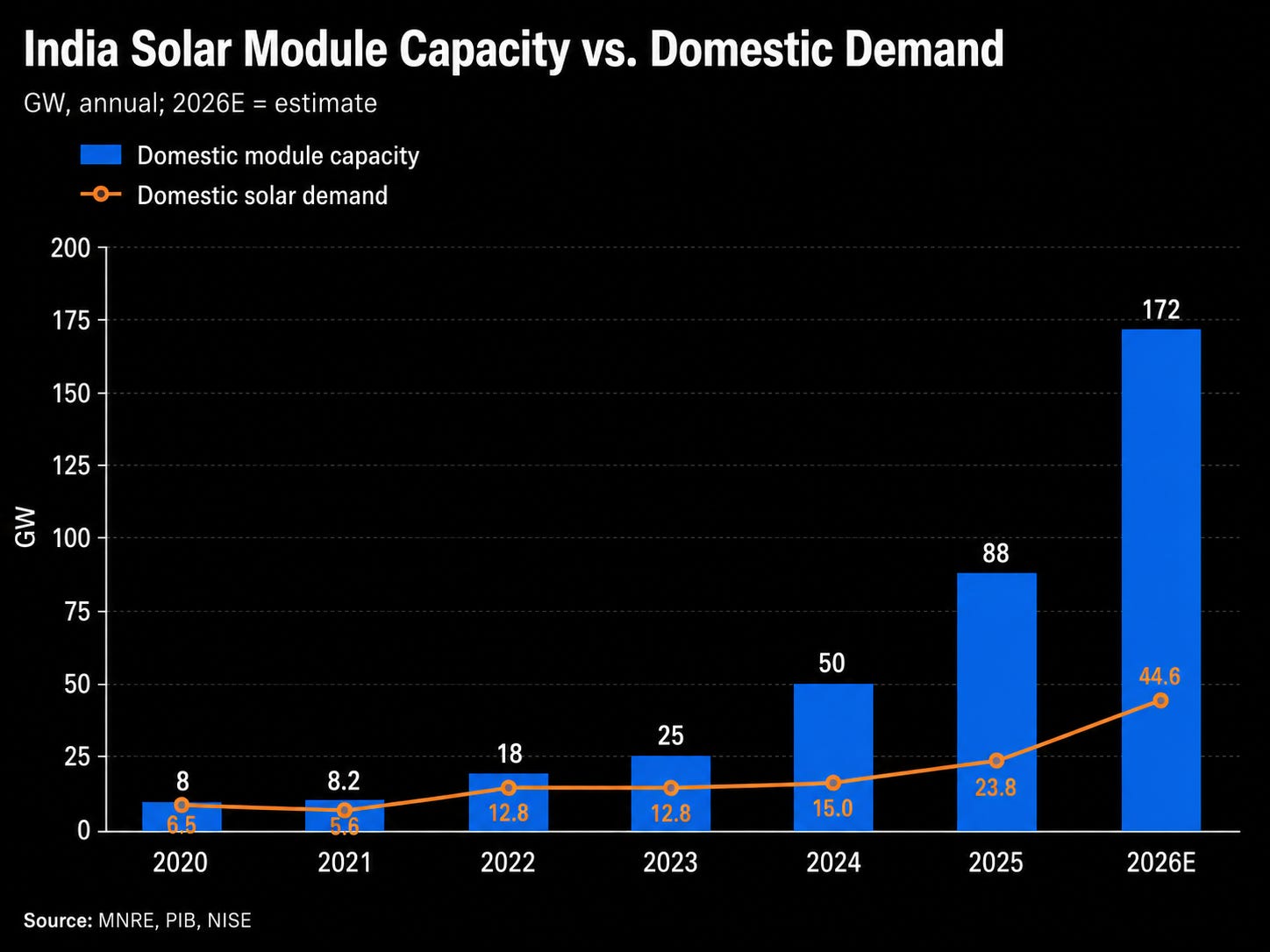

India has used tariffs, domestic-content pressure, production-linked incentives, approved-manufacturer lists, public procurement rules, and strategic demand creation to build a domestic solar manufacturing base at remarkable speed.

Its solar module manufacturing capacity rose from a marginal position a decade ago to more than 100GW, and by early 2026 Indian official data put the figure at about 172GW.

This does not mean India has built a fully integrated photovoltaic supply chain. It has not. Its upstream capabilities remain weak. Polysilicon is still heavily import-dependent. Wafer capacity is only beginning to emerge. Cell capacity lags module capacity. Many critical production tools still depend on foreign suppliers, especially Chinese suppliers.

But modules are the visible layer of solar industrialization, and India has built that layer quickly.

The method was not passive. India did not simply wait for firms to arrive. It built a protected domestic market. It imposed duties on imported cells and modules. It created PLI support. It used approved-manufacturer lists to shape demand. It encouraged large domestic business groups to enter the sector. The message was clear: India did not want only Chinese solar products. It wanted Chinese-style solar capacity.

And that capacity needed equipment.

This is where Chinese firms entered.

A solar production line is not just a set of machines. It is a package of layout, installation, process parameters, production recipes, yield management, worker training, debugging, materials compatibility, quality control, and supplier coordination. In photovoltaic manufacturing, as in transformer manufacturing, the most valuable technology is often embedded in how a line is stabilized and scaled.

Chinese photovoltaic equipment firms became the most practical suppliers for India’s ambitions. Their equipment was cheaper, faster to deliver, and more closely tied to mass-production experience than most Western alternatives. A Chinese turnkey line could give an Indian manufacturer a shortcut into production that would otherwise take far longer and cost much more.

Reliance’s order for heterojunction production lines from China’s Maxwell is a revealing example. The Indian conglomerate wanted to build solar manufacturing capability at scale. Maxwell had the equipment and process experience. Other Chinese suppliers have also helped Indian firms expand in TOPCon, cell, module, wafer, and related production.

Each contract made sense at the company level.

For the Chinese equipment maker, it meant revenue, overseas validation, and access to a large market. For Indian manufacturers, it meant a faster learning curve. For the Indian state, it meant that policy targets could be converted into visible factories. But for China’s solar system as a whole, the result was more ambiguous.

A Chinese equipment firm can tell itself: if I do not sell, another supplier will. An engineer can say: this is only installation support. A listed company can tell investors: this is overseas growth. A local government can see exports and orders. Each decision looks rational in isolation.

When every firm follows the same logic, however, an industry begins to export not only equipment, but the operating system of production.

This is the collective-action problem inside Chinese solar.

China’s solar crisis was not caused by India alone. The deepest reason for the losses of Chinese solar manufacturers has been domestic overcapacity, rapid technology cycles, aggressive capital expenditure, falling module prices, and the brutal commoditization of midstream and downstream production. China built more capacity than global demand could absorb. Prices fell. Margins collapsed. Many leading firms entered deep losses.

But India changes the external environment. Once Indian module capacity expands, it does not stay inside India. Protected by tariffs at home and supported by policy, Indian manufacturers can compete in third markets, especially where geopolitical rules favor non-Chinese supply. India does not need to replace China overnight to create pressure. It only needs to become an additional source of capacity in a global market already suffering from oversupply.

Here again, extractive localization appears.

India does not merely import Chinese solar products. It uses Chinese equipment, Chinese process experience, Chinese engineering support, and Chinese supplier knowledge to build production capacity behind a policy wall. The local market is protected. The production line is imported. The engineering knowledge is absorbed. The future competitor is born.

This does not mean every Chinese solar equipment export should be stopped. That would be too simplistic.

But it does mean China must distinguish between product exports, equipment exports, capacity exports, and capability exports.

Selling a solar module is one thing. Selling a full production line is another. Installing and debugging that line is more serious. Training local engineers, transferring process parameters, and teaching yield improvement is closer to capability transfer. Helping a protected market create a future competitor is no longer only a commercial transaction. It is an industrial-security question.

Solar shows that the gray zone is large. A cell line, a wafer line, a coating tool, a furnace, a deposition system, a laser process, a materials recipe, a yield-improvement routine, a production-debugging team — none of these looks as dramatic as a semiconductor lithography machine. Together, they define whether a country can build a photovoltaic manufacturing ecosystem.

India is trying to climb this ladder. That ambition is understandable. China once climbed by absorbing foreign knowledge as well. But China is now on the other side of the table. It is no longer mainly the latecomer seeking technology. It is the holder of the world’s most complete renewable-energy manufacturing system.

That changes the responsibility of the Chinese state.

8. Consumer Electronics: The Most Familiar Front Line

If transformers show the transfer of heavy-equipment know-how, and solar shows the leakage of production systems through equipment and turnkey lines, consumer electronics shows the most familiar and politically sensitive form of extractive localization.

At first glance, India’s consumer electronics story looks like a success. Smartphone production has increased. Apple’s supply chain has expanded in India. Indian contract manufacturers are growing. Electronics manufacturing has become one of the most visible achievements of Make in India.

This progress is real.

But it is not a simple story of autonomous Indian manufacturing. Much of the system still depends on Chinese firms, Chinese suppliers, Chinese engineers, Chinese components, Chinese ODM capability, Chinese tooling, and Chinese production-management experience.

The real capability in consumer electronics is not merely final assembly. It lies in the details: PCB layout, motherboard design, display modules, camera modules, battery management, structural parts, connectors, acoustic components, testing fixtures, yield management, supplier coordination, production cadence, quality control, after-sales feedback, and rapid iteration.

A country can build assembly plants relatively quickly. Turning these hidden layers into domestic capability is much harder.

India’s strategy has been clear. It does not want Chinese firms merely to assemble low-value products inside India. It wants Chinese firms, through joint ventures, local partners, ODM cooperation, technology transfer, training, and supply-chain migration, to leave more capability behind.

Again, the goal is understandable. Every late industrializer wants to learn.

The problem is the method.

India’s approach often combines market access, policy approval, localization requirements, tax pressure, security review, and joint-venture structures.

Foreign firms are pulled into the market, but their room for independent control can narrow over time. The host country wants the capability but not necessarily the foreign company’s long-term dominance.

Xiaomi is the clearest warning.

Xiaomi was once one of the most successful Chinese brands in the Indian smartphone market. It expanded rapidly through products, channels, supply-chain efficiency, and local manufacturing. But as India intensified regulatory, security, and tax scrutiny of Chinese firms, Xiaomi became entangled in disputes over frozen funds, foreign-exchange rules, royalty payments, and customs valuation.

The later customs dispute is especially revealing. At issue was whether royalties paid to technology providers such as Qualcomm should be included in the customs valuation of components imported by contract manufacturers. This question goes to the heart of India’s electronics-manufacturing model.

In contract manufacturing, where does technology licensing end and component valuation begin?

Who owns the design?

Who controls the intellectual property?

Who should be taxed?

How should India treat a model in which a foreign brand brings software, design, standards, supplier management, and technology licensing while local or contract manufacturers carry out production?

These questions are not legal footnotes. They define whether foreign firms feel safe putting deeper capabilities into India.

If tax and customs rules can be reinterpreted years later, firms will not necessarily leave, but they will adjust. Assembly may stay. Deeper design may not. Production lines may be localized. Core process knowledge may remain outside. Local procurement may rise, but the highest-value modules, engineering iteration, supply-chain management, and software-controlled systems may be kept elsewhere.

India faces a contradiction. It wants to reduce dependence on Chinese brands, but it still needs Chinese supply-chain capability. It wants local champions, but those champions still need Chinese ODMs, Chinese components, Chinese design support, and Chinese manufacturing experience. It wants technology transfer, but foreign firms want legal stability and control over their know-how.

This is why Indian electronics policy has increasingly pushed Chinese firms toward local partners, minority structures, joint ventures, and technology-transfer arrangements. Indian contract manufacturers such as Dixon are becoming important platforms. Their partnerships with Chinese ODM firms show the direction of travel. India does not necessarily want Chinese companies to dominate the Indian consumer market as brands. It increasingly wants Chinese firms to become suppliers of design, manufacturing experience, components, equipment, and engineering support for Indian firms.

This is extractive localization in consumer electronics.

First, use the market and policy incentives to attract external capability. Then restrict the foreign firm’s full control.

Then pressure or incentivize it to work through domestic partners.

Then use tax, customs, security, and approval mechanisms to reshape the boundary of control. Finally, try to transfer the production system to domestic firms.

This is not always illegal. It is not always crude. But it is structurally extractive.

For China, the danger is that its consumer-electronics ecosystem can be broken into transferable modules: ODM design, display modules, camera modules, PCB, casing, batteries, testing equipment, production management, process debugging, and on-site engineers. Each item can appear to be ordinary business cooperation. Together, they constitute the migration of a national electronics-manufacturing system.

This explains why India’s electronics industry worries about China’s new rules. India does not only need Chinese phones or Chinese parts. It needs the engineering capability behind the Chinese electronics system. Equipment, drawings, engineers, debugging, training, components, software parameters, supplier coordination — these are the things that allow assembly to become manufacturing.

If China begins to treat these channels as part of the technology-export boundary, India’s learning curve will lengthen.

9. China’s Old Overseas Logic Has Become Riskier

For many years, Chinese industrial globalization followed a simple commercial logic: go where the market is, build factories, sell equipment, win orders, localize production, train workers, and use Chinese engineering capability to expand abroad.

That logic was reasonable when Chinese firms were still climbing global value chains and fighting for recognition. But the balance has changed.

China is no longer only exporting low-cost capacity. In many sectors, it is exporting the results of decades of industrial accumulation: power equipment, solar manufacturing systems, batteries, electronics supply chains, electric vehicles, industrial machinery, grid equipment, materials, and process know-how.

This changes the meaning of overseas investment.

A Chinese company going abroad may not only transfer products. It may transfer factory design, equipment configuration, engineering training, supplier-management methods, quality-control routines, testing systems, data, software parameters, and troubleshooting knowledge. Once these capabilities are transferred, they can be absorbed by the host country, redirected by policy, localized through procurement, or used by future competitors.

The old assumption was that overseas production simply expanded Chinese firms. The new reality is more complicated: overseas production can also become a channel through which Chinese industrial capability is detached from Chinese control.

For a Chinese equipment maker, selling a production line to India may be a good contract. For China’s industrial system, it may be the beginning of a future competitor.

10. From Exporting Products to Governing Capability

China’s new outbound-investment regulation marks a shift from managing capital flows to governing capability flows.

The state is not saying Chinese companies should stop going abroad. It is saying that overseas investment can no longer be treated as a purely commercial decision when it involves sensitive technology, data, services, training, engineering support, and the transfer or disposal of overseas assets.

The most important change is conceptual.

Technology is no longer understood only as a patent, a machine, or a formal licensing contract. It can move through engineers. It can move through training. It can move through technical guidance. It can move through a debugging team. It can move through production-line installation. It can move through software parameters, process recipes, testing routines, supplier lists, and the sale of an overseas subsidiary after years of accumulated know-how.

This is the border China is now trying to govern.

The old customs border controlled goods. The new industrial border controls capability.

This does not mean China should become closed. China’s industrial firms still need global markets. They need customers, revenue, overseas operations, after-sales networks, and local presence. But globalization must become more disciplined. The question can no longer be only whether a contract is profitable. It must also be whether the contract transfers a capability that China may later need to defend.

This requires a different relationship between the Chinese state and Chinese capital.

If every firm acts only according to its own short-term order book, the national industrial system can suffer long-term erosion. If every equipment maker says “I will sell because others will sell,” the result is collective self-hollowing. If every factory treats engineers, training, process guidance, and debugging as ordinary services, China may gradually export the very operating knowledge that made its manufacturing advantage possible.

The state has to solve this collective-action problem.

Conclusion: The Border Has Moved

The most important border in industrial competition is no longer the customs border.

It is the border around know-how.

Machines can cross borders. Engineers can cross borders. Drawings can cross borders. Training can cross borders. Data can cross borders. A joint venture can change ownership. An overseas subsidiary can be sold after years of technical accumulation. A local partner can become a competitor. A host-country policy can turn market access into localization pressure.

India’s extractive localization strategy has made this border visible.

The Baoding Tianwei case shows how a financially weak overseas venture can still transfer high-voltage industrial capability. Solar shows how an entire industry, under pressure from overcapacity and short-term commercial incentives, can export the production systems that help create future competitors. Consumer electronics shows how supply-chain capability can be broken into modules and gradually absorbed through contract manufacturing, ODM partnerships, tax pressure, and local champions.

India’s ambition is understandable. It wants to industrialize. It wants to absorb technology. It wants to reduce dependence on imports. It wants to use market scale and policy leverage to build domestic capability. These are the ambitions of every late industrializer.

China’s caution is also understandable. It spent decades building the world’s most complete manufacturing system. It can no longer allow that system to leak outward too cheaply, too casually, and too naively through the commercial decisions of individual firms.

The old globalization moved products. The next phase moves capability.

And China is now beginning to decide which capabilities should no longer move freely.

Related Reads:

If this framework helps you understand China, industrial power, state capacity, capital, technology, and global order beyond the usual headlines, please consider subscribing to China as a System.

Paid subscriptions help support this work, but likes, restacks, and shares are also meaningful forms of support.

For a full guide to the publication and its main research series, start here: China as a System: Publication Map.

From a historical perspective, technology transfer is inevitable and there is no need to avoid it. Of course, areas involving national security are an exception, but national security must have a clear boundary. As China's population continues to decline, China cannot forever maintain 35% of the world's manufacturing output. Rather than preventing this transfer, it is better to let other countries integrate into one's own industrial chain. This will make the industrial chain centered on China's standards and systems larger in scale and more efficient. Building a community with a shared future and sharing prosperity with the world is a sustainable path. Instead of fearing competition and trying to prevent it from happening, it is better to strengthen oneself.

I believe this to be a huge blunder on China’s part to restrict technology transfer. Why? Look at how much control the US has over its allies’ technology - a lot of which has to do with technology transfer.

The US could cut off high end semiconductors to China simply because all the countries in that sector are part of American supply chains, giving the US power over the technology.

China could have this sort over power over India too. Instead, by issuing blanket restrictions, China has made India double down on technology transfer, only this time from countries that are willing to find alternative suppliers. As an example, India is using Japanese technology to build up ingot and wafer capacity in the solar supply chain. China will have little, if any, control over this.

The same is being applied from batteries to shipbuilding, where other countries seeking to reduce their China dependence are building up India’s supply chains. This is does not bode well for China’s future.