Inside Cambricon’s AI workload Test

Cambricon is moving from a domestic AI-chip narrative into a fundamentals test of revenue, delivery, customer structure, and platform closure

The most important thing about Cambricon is that it is taking an independent third-party route based on its self-developed DSA architecture: it has no internal hyperscaler order pool, no CUDA compatibility advantage, yet it has begun entering real AI workloads through revenue, shipments, model adaptation, and large-customer rumors.

This essay is part of China’s AI Chip Companies, a sub-series under China’s AI Infrastructure Stack, tracking China’s domestic AI chip firms, data-center compute suppliers, and the industrial system behind AI infrastructure.

Three questions this essay tracks

First, what has changed in Cambricon’s fundamentals?

It has moved from long-term losses to annual profitability, followed by another record quarter in revenue, net profit, and operating cash flow.

Second, where does Cambricon sit inside China’s AI chip market?

It is a mid-share domestic AI accelerator supplier, but one of the few independent companies with self-designed architecture, instruction set, compiler, software stack, and cloud AI chip products.

Third, what still needs to be tested?

MLU690 scale-up, large internet-customer recurrence, and platform closure across chips, software, model adaptation, supply chain, and cash flow.

Eagle and Rock (鹰石图), in the spirit of Pan Tianshou (潘天寿)

Its solitary eagle, hard rock, sharp posture, and large areas of controlled emptiness echo the central argument of this essay: Cambricon’s position in China’s AI chip industry is defined by an independent and difficult route.

Cambricon has long been one of the most symbolic companies in China’s AI chip industry. It has a Tsinghua-linked technical background, early AI processor IP accumulation, cloud AI accelerator products, and the label of being the STAR Market’s “first AI chip stock.” Its long-term problem was equally clear: the technological direction mattered, but the financial statements had not yet proven the business model.

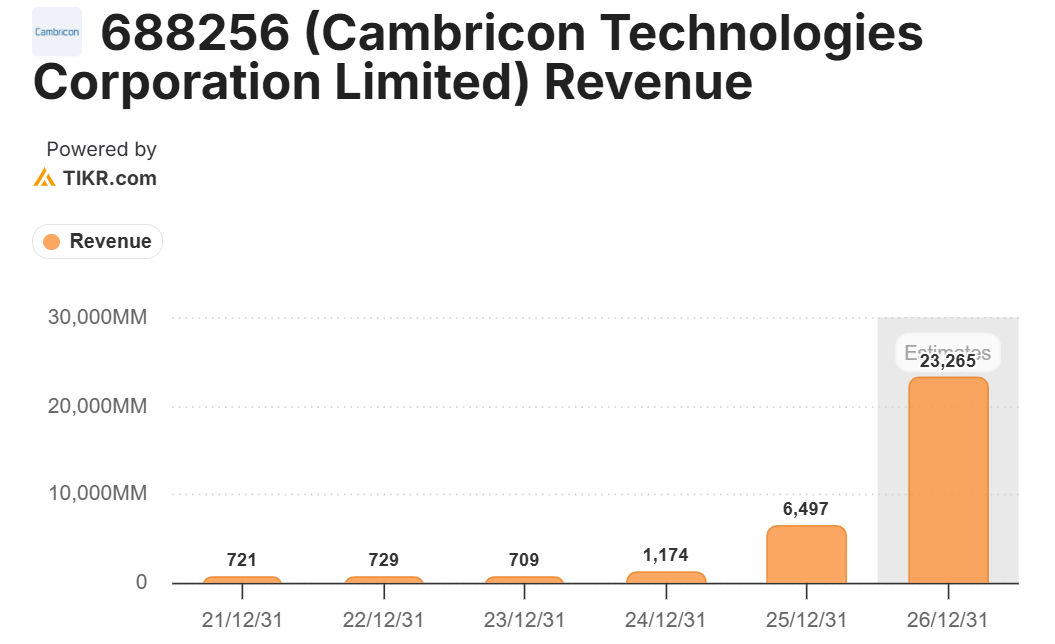

That changed after 2025. The company generated RMB 6.497 billion in revenue in 2025, up 453.21% year over year. Net profit attributable to shareholders reached RMB 2.059 billion, turning around from a RMB 452 million loss in the previous year. Non-GAAP net profit reached RMB 1.770 billion. Growth continued in the first quarter of 2026: quarterly revenue reached RMB 2.885 billion, up 159.56%; net profit reached RMB 1.013 billion, up 185.04%; non-GAAP net profit reached RMB 934 million, up 238.56%; operating cash flow turned positive at RMB 834 million, compared with negative RMB 1.399 billion a year earlier.

This puts Cambricon in a new phase. Revenue growth corresponds to scaled product procurement. Profitability shows that the expense structure is being absorbed by revenue. Positive operating cash flow points to better collection. Continued R&D growth shows that profitability did not come from cutting research. The company is beginning to move from an R&D-heavy firm into a hardware platform company driven by product delivery and supply-chain organization.

Cambricon’s position in China’s AI accelerator market

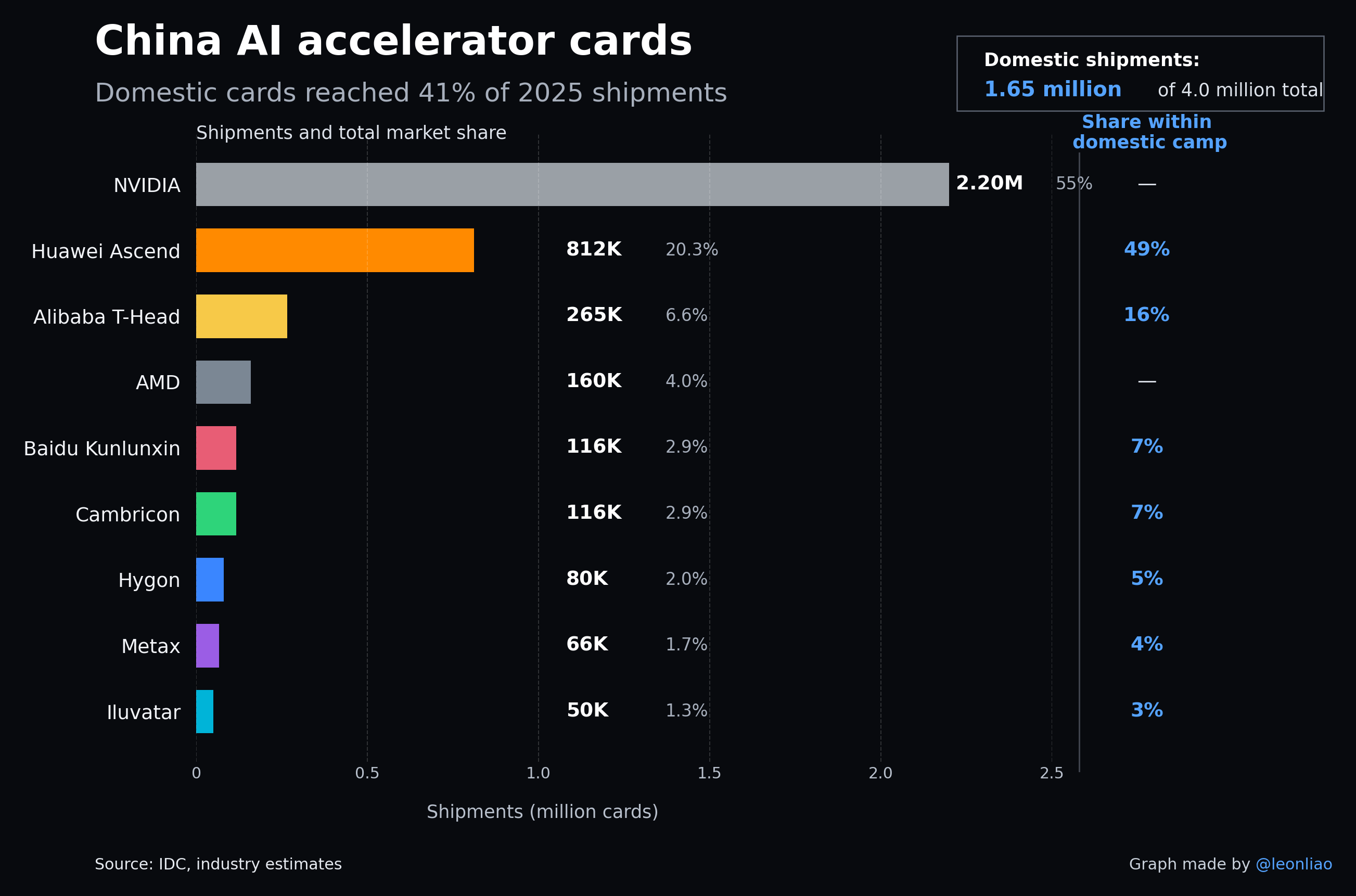

According to IDC’s framework, China shipped roughly 4 million AI accelerator cards in 2025, including about 1.65 million domestic AI accelerator cards. The domestic share reached roughly 41%, up from about 30% in 2024. NVIDIA remained the largest supplier in China, with about 2.2 million cards shipped and an overall market share of roughly 55%. Within the domestic camp, Huawei Ascend is overwhelmingly first.

This table gives Cambricon a more accurate position. Its overall market share is only about 2.9%, and its share within the domestic camp is about 7%, roughly comparable to Baidu Kunlunxin. It trails Huawei Ascend and Alibaba T-Head, while sitting above Hygon, Metax, and Iluvatar by this shipment estimate.

Beyond market share, Cambricon’s difference lies in its identity. Huawei Ascend has Huawei Cloud, servers, government-enterprise channels, and a full-stack ecosystem. Alibaba T-Head serves Alibaba Cloud and is expanding external sales. Baidu Kunlunxin sits behind search, intelligent cloud, and autonomous-driving workloads. ByteDance’s SeedChip is more internally oriented. Cambricon has no internal business unit to absorb capacity and belongs to no internet platform. It has to win external orders.

That independent third-party identity gives Cambricon a window. China’s internet giants compete with one another. ByteDance may not want to buy Alibaba chips, and Alibaba may not want to use a Baidu solution. Cambricon belongs to none of them, which theoretically allows it to enter multiple customer supplier lists at the same time. The duration of this window depends on the pace of large-platform in-house chip development. Google built TPU, Amazon built Trainium and Inferentia, Alibaba built T-Head, Baidu built Kunlunxin, and ByteDance is also advancing its own AI chips. Neutrality can slow procurement migration, but it cannot remove the long-term cost incentive for large customers to develop chips in-house.

Financial quality now faces a hardware-cycle test

Cambricon’s strong growth continued in the first quarter of 2026: quarterly revenue reached RMB 2.885 billion, up 159.56%, and the market now expect full year revenue of RMB 23.26bn, up 257%.

Several first-quarter indicators matter more than revenue growth alone.

The first is operating cash flow. Cambricon generated RMB 834 million in operating cash flow in the first quarter, compared with negative RMB 1.399 billion a year earlier. For a hardware company, revenue recognition can be affected by delivery timing; cash flow shows collection quality and customer payment arrangements more directly.

The second is prepayments. At the end of the first quarter, prepayments reached RMB 1.897 billion, up 154.72% from the end of 2025. This usually means the company is locking in supply-chain resources ahead of future delivery, including wafers, packaging, boards, key components, and capacity arrangements.

The third is inventory. At the end of the first quarter, inventory was about RMB 4.497 billion. The company booked about RMB 245 million in combined credit impairment and asset impairment losses in the quarter, including about RMB 246 million in inventory write-downs, mainly because some raw materials from earlier strategic stocking had aged.

These indicators show that Cambricon has entered a real hardware ramp cycle. As product shipments expand, supply-chain management, inventory turnover, raw-material aging, customer delivery timing, and cash conversion will all affect profit quality.

R&D is moving from chips to system platforms

Cambricon has not reduced R&D intensity after becoming profitable. In 2025, R&D spending reached RMB 1.169 billion. The company had 887 R&D employees, accounting for 80.13% of total staff; more than 80.95% of R&D personnel had master’s degrees or above. In the first quarter of 2026, R&D spending reached RMB 324 million, up 18.88% year over year. The R&D-to-revenue ratio fell to 11.23%, mainly because revenue expanded rapidly.

The R&D focus is moving from chip specifications toward system platforms. In its 2025 annual report, the company said it was advancing next-generation intelligent-processor microarchitecture and instruction-set development. Its training software platform continued improving model adaptation breadth, training performance, and tooling experience. Its inference software platform advanced technical innovation, open-source ecosystem work, and productization.

Cambricon needs to build sustained usability after customer migration. NeuWare, vLLM support, Day 0 model adaptation, training software, inference toolchains, and cluster-deployment capability will jointly decide whether customers are willing to place Cambricon inside long-term AI infrastructure.

Customer structure determines revenue quality

Cambricon rarely discloses major-customer names.

In its financial reports, only 2021 and 2022 clearly disclosed the largest customer, both being state-backed intelligent-computing-center project companies in Kunshan, Jiangsu and Nanjing. In other years, the company used vague descriptions such as “local state-owned computing-infrastructure investment entities” or “leading companies in telecom, finance, and internet.”

Customer concentration numbers are clearer.

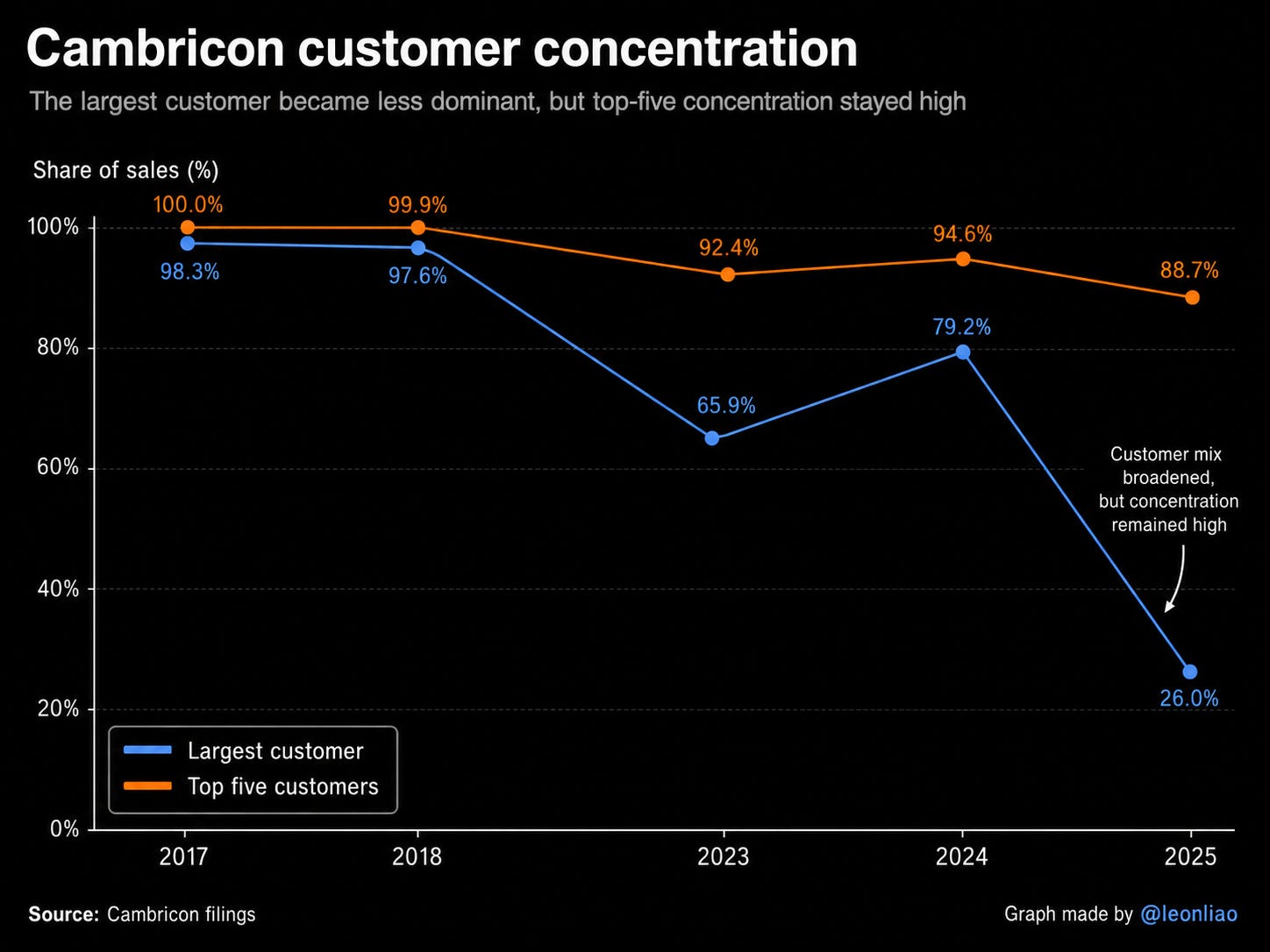

Cambricon has never been a truly diversified customer company. In 2025, the top five customers still accounted for 88.7% of sales. The change was that the largest customer share fell from 79.2% in 2024 to just above 26%. The top five share fell by only about six percentage points, which means revenue did not spread across dozens of customers; it moved from one extremely large customer to several still-large customers. The 2025 annual report disclosed that the third-largest customer was a “long-term partner,” while the other four were newly added in 2025. The top five customer sales were approximately RMB 1.703 billion, RMB 1.401 billion, RMB 1.237 billion, RMB 764 million, and RMB 655 million.

The 85.31% figure in the 2025 interim report needs to be separated from revenue concentration. It refers to the top five customers’ share of accounts receivable and contract assets at period end, not sales revenue. The five shares were 42.5%, 18.0%, 8.9%, 8.4%, and 7.6%. It measures collection concentration. Sales dispersion and receivables concentration can coexist, but if receivables remain concentrated among a few customers, collection risk requires separate attention.

There are many market rumors about who these major customers are. Bloomberg reported in 2025 that ByteDance was Cambricon’s largest customer at the time, with orders accounting for more than 50%. China Mobile’s Harbin intelligent-computing center went online in August 2024 and deployed more than 18,000 AI accelerator cards, with public reporting saying a meaningful number were Cambricon Siyuan 590 cards. There have also been rumors of cooperation with Alibaba and Tencent, but the scale is unknown. None of these has been confirmed one by one by Cambricon.

These rumors matter because they reveal the real debate over revenue quality. If the largest customer is indeed ByteDance, Cambricon has entered the inference system of one of China’s largest AI application companies. If revenue still mainly comes from local state-backed intelligent-computing centers, growth quality is more tied to policy and infrastructure cycles. If Alibaba, Tencent, China Mobile, and financial customers are all making recurring purchases, the customer structure would look much healthier.

The most complex point is that the market-suspected largest customer is also developing its own AI chips. Public reports say ByteDance’s AI chip team already exceeds 1,000 people and plans mass production in 2026. Cambricon once had deep cooperation with HiSilicon, before Huawei Ascend moved toward a self-developed full stack. If ByteDance is now a major Cambricon customer, that history matters. A large customer brings orders, and may also bring future substitution.

The DSA route: the instruction-set bet

AI chips globally fall into two broad technical routes.

The first is GPGPU. NVIDIA and AMD follow this route. GPUs were originally designed for graphics rendering. After NVIDIA introduced CUDA in 2006, GPUs became general-purpose parallel-computing platforms. AI training, scientific computing, simulation, and graphics workloads can all share the same hardware and software ecosystem. GPGPU’s advantages are flexibility, mature developer ecosystems, and low migration cost. The tradeoff is that hardware resources cannot be fully dedicated to AI matrix computation.

The second route is ASIC / DSA. This route is designed directly for AI computation, stripping out graphics-rendering burden and allocating silicon area toward matrix computation, tensor calculation, on-chip memory, interconnect, and AI workload optimization. Google TPU is the representative case; Huawei Ascend, Cambricon, Alibaba T-Head, and Baidu Kunlunxin also belong to this direction. The advantage is better performance and energy efficiency. The tradeoff is weaker generality and the need to rebuild software adaptation and ecosystem support.

The route choice depends on AI workload stability. When algorithms change rapidly, GPGPU flexibility matters more. Once dominant architectures stabilize, DSA efficiency becomes easier to monetize. Over the past decade, AI computation moved from CNNs and RNNs to Transformers. Transformers are now dominant, but world models, state-space models, nonlinear-dynamics computation, and other directions are still evolving. Cambricon’s DSA bet is a bet that AI workloads will have a long enough stable window for specialized architecture efficiency to become commercial advantage.

Chinese companies are also splitting along these two routes.

Hygon follows a CPU + DCU route with visible AMD CDNA lineage, giving it advantages in CUDA-like / ROCm migration and x86 data-center ecosystems.

Moore Threads follows a full-function GPU route, with a founding team carrying NVIDIA experience and an ambition to replicate an NVIDIA-style general GPU platform.

Metax has a clear AMD lineage and leans toward general GPU / GPGPU.

Biren is closer to an “original architecture + high compute” route, with challenges around high-end chip supply chains and cluster delivery.

Cambricon comes from the Institute of Computing Technology of the Chinese Academy of Sciences. It follows a self-developed Cambricon ISA, MLUarch microarchitecture, and NeuWare software stack, and focuses only on AI computation rather than graphics rendering. It is not an internet giant’s internal chip effort, not a CUDA-compatible path, and not an NVIDIA / AMD alumni project.

The instruction set is Cambricon’s largest technical bet. It can be simplified as the bottom-level language between chip and software, but above it sit microarchitecture, compilers, operator libraries, AI frameworks, inference services, training tools, and debugging environments. NVIDIA’s CUDA is not just a language; it is a full development ecosystem. Hygon can use AMD ROCm and CUDA-like migration to reduce customer code changes. Huawei Ascend has Da Vinci architecture, CANN heterogeneous computing, MindSpore, servers, cloud, and government-enterprise channels behind it.

Cambricon’s difficulty is that each customer requires migration from the CUDA system, PyTorch / TensorFlow operator adaptation into its own software stack, and then training, inference, debugging, and performance optimization. Market discussion around DeepSeek and other domestic models often mentions “Day 0 support” and “rapid adaptation.” That mostly means the model can quickly run at the model layer. Long-term production migration still depends on operator coverage, stability, debugging tools, performance-analysis tools, and engineering support.

The reward for this route is high. If AI architectures stay relatively stable, ASIC / DSA performance and energy-efficiency advantages can become a moat, making Cambricon’s decade-plus accumulation in instruction sets, microarchitecture, and patents more valuable. The risk is equally high. If mainstream architectures move sharply away from Transformers, compilers, operator libraries, memory scheduling, debugging tools, and software ecosystems will all face another engineering cycle.

This path could win deeply, or fail painfully.

Cloud products and the Siyuan 690 transition

Cambricon’s revenue structure is now highly concentrated. In 2025, cloud product-line revenue reached RMB 6.477 billion, accounting for more than 99% of total revenue. Edge products, IP licensing and software, and other businesses were all small. The company’s revenue center has shifted to cloud AI chips, intelligent accelerator cards, boards, and data-center products.

In 2025, production of intelligent chips and boards reached 127,700 cards, while sales reached 117,400 cards, up 409.84% and 201.57% year over year. A rough calculation using cloud-product revenue and card sales implies an ASP of about US$8,000. There are also market rumors that 2026 expansion could reach 300,000 cards.

2025 revenue mainly came from Siyuan 590. Market commentary generally believes Siyuan 590’s effective performance can reach roughly 80%–90% of A100, while pricing is about one-third of comparable NVIDIA products. For domestic customers, that means “good enough, purchasable, and available”: sufficient for inference, domestic substitution, and some training scenarios.

The next validation point is Siyuan 690 / MLU690. Public information indicates that Siyuan 690 reached scaled production in early 2026. Market materials say the chip is based on SMIC’s N+2 advanced process. There is dispute over its process equivalence: mainstream views place it near 7nm+, while Sigmaintell classifies it as a 5nm node. The chip uses a dual-die Chiplet design, carries 196GB of HBM3, reportedly delivers more than 700 TFLOPS of FP16 compute, has interconnect bandwidth above 890Gbps, and is priced at roughly RMB 135,000. Compared with Siyuan 590, both compute and HBM capacity are more than doubled. The market’s common performance target is 80%–85% of NVIDIA H100.