Inside China’s Robot Export Breakout

China’s Industrial Robots Are Moving from Domestic Substitution to the Export of Global Manufacturing-Automation Systems

What China is now exporting is no longer just robot hardware. It is an automation capability package repeatedly refined on Chinese manufacturing floors: lower cost, faster deployment, stronger scenario adaptation, and an increasingly complete engineering-service system.

This essay is part of China Industry Signals.

Executive Summary

China’s industrial robot exports are entering a critical inflection point. In April 2026, China exported 25,375 industrial robots, up 89.2% year on year, with monthly exports surpassing 25,000 units. This shows that China’s robotics industry has crossed the threshold for large-scale global supply.

A surge in export volume is occurring alongside a decline in average export price. In April, China’s industrial robot exports reached RMB 943 million in value, up only 1.3% year on year, implying an average unit export price of roughly RMB 37,200. During the same month, China imported 10,887 industrial robots, with import value reaching RMB 1.056 billion, implying an average unit import price of roughly RMB 97,000. This price gap suggests that China’s robot exports are first breaking through in high-cost-performance, standardized, mobile, and application-driven products.

The foundation of China’s robot exports comes from the world’s largest domestic market. In 2024, China installed 295,000 industrial robots, accounting for 54% of global deployments. Its operational stock exceeded 2 million units. Chinese domestic suppliers also exceeded foreign suppliers in local market share for the first time, reaching 57%. China first became the world’s largest robot testing ground, and only then became a net exporter of industrial robots.

Mobile robots are the first segment to achieve a global breakthrough. The share of export orders for Chinese mobile robots rose from 25.87% in 2022 to 37.12% in 2024, and exceeded 40% in 2025. Behind this is the systemic capability incubated over many years in China’s e-commerce, warehousing, retail, and third-party logistics sectors.

The overseas path is moving from following customers to localized operations. STEP’s SCARA robots and desktop six-axis robots have already followed customers such as Foxconn, Biel Crystal, and BYD into overseas 3C electronics and new-energy supply chains, with annual sales of related products exceeding 1,200 units. Estun, meanwhile, is advancing globally through overseas service networks, acquired brands, and localized teams.

China’s industrial robot industry is still on an upgrading path. Export growth shows that Chinese suppliers already possess large-scale supply capability. The fact that import unit prices remain significantly higher than export unit prices shows that high-end scenarios, complex processes, core components, overseas service networks, and global brand trust remain the key competitive frontiers for the next stage.

1. April Exports Surpassed 25,000 Units, Up 89%

China’s industrial robot export data for April 2026 was striking. GG Robot, citing data from China Customs, reported that China exported 25,375 industrial robots in April, up 89.2% year on year. Export value reached RMB 943 million, up 1.3% year on year. In the same month, China imported 10,887 industrial robots, up 28.1% year on year, while import value reached RMB 1.056 billion, up 27.3%. In volume terms, China has continued to maintain its position as a net exporter of industrial robots. In value terms, imports still exceeded exports, showing that the product structures of imports and exports remain clearly different.

Industrial robot export volume nearly doubled year on year in April, while export value barely grew at the same pace. The implied average export price was roughly RMB 37,200 per unit, compared with an implied import price of roughly RMB 97,000 per unit. In other words, China can already export industrial robots at scale, but the current export mix is still more concentrated in standardized, high-cost-performance, rapidly deployable products. Imported robots still correspond more to high-price, high-complexity, and process-intensive application scenarios.

This price structure does not weaken the significance of the export data. It makes this shift more worth studying. The competitive pattern China’s manufacturing sector has developed over many years often begins by lowering the cost curve in large numbers of real-world scenarios, improving reliability, delivery speed, maintenance capability, and application fit, and then moving upward along the complexity curve. Industrial robots are now repeating a path already seen in many Chinese manufacturing sectors: using scale and cost-performance to enter the market first, then using iteration and application density to expand the capability boundary.

Data from the National Bureau of Statistics provides a broader industrial backdrop for this export inflection point. From January to April 2026, value-added output of industrial enterprises above designated size rose 5.6% year on year in real terms. In April, it rose 4.1% year on year. Within the industrial system, equipment manufacturing and high-tech manufacturing continued to outperform overall industry. Sun Xiao, chief statistician of the Department of Industry at the National Bureau of Statistics, noted in his interpretation of April industrial production that value-added output of equipment manufacturing above designated size rose 8.3% year on year in April, contributing 74.5% of total growth in above-scale industry. High-tech manufacturing value-added output rose 12.8% year on year, contributing 52.1% of total growth.

Robotics sits at the intersection of high-end manufacturing and equipment manufacturing. Sun Xiao specifically noted that new growth drivers such as embodied intelligence and human-machine collaboration helped accelerate robotics development. In April, output of robot reducers, industrial robots, and service robots rose 38.3%, 15.1%, and 12.3%, respectively. According to the National Bureau of Statistics, from January to April, output of robot reducers and industrial robots rose 73.3% and 25.7%, respectively. This shows that robot export growth is embedded within China’s broader expansion in equipment manufacturing, high-tech manufacturing, digital-product manufacturing, and the industrial spillover effects of “AI+”.

The real signal behind industrial robot exports is that China’s automation supply chain is beginning to diffuse outward from domestic manufacturing sites into external markets. Over the past few years, Chinese robotics companies first completed supply-chain training, price training, application training, and customer training at home. These capabilities are now being converted into export orders, localized services, and overseas application scenarios.

2. The World’s Largest Robot Testing Ground Is the Underlying Advantage Behind Chinese Firms’ Overseas Expansion

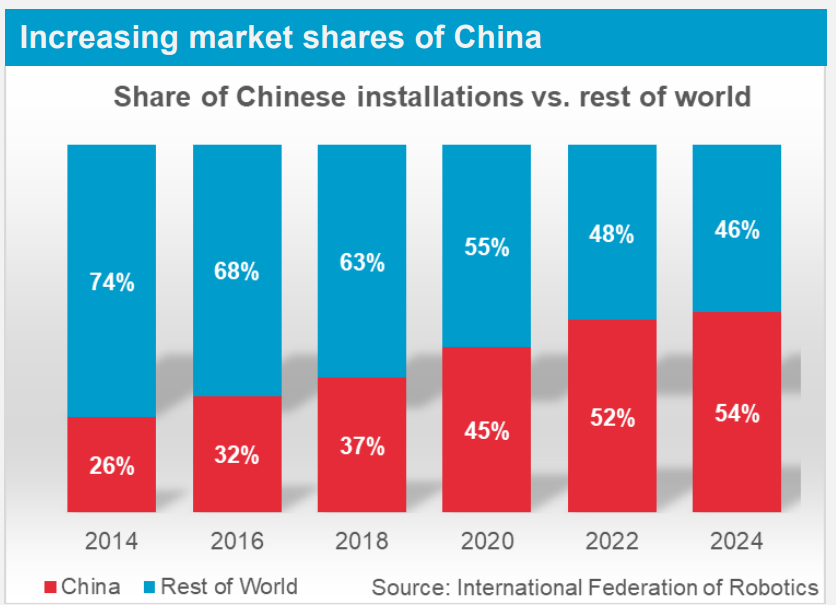

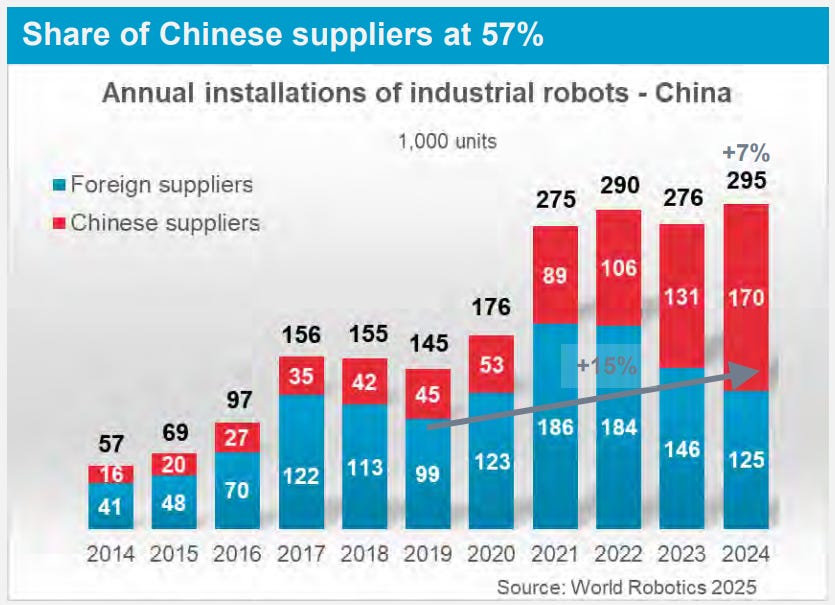

China’s ability to export industrial robots quickly starts with the scale of its domestic market. According to IFR’s World Robotics 2025 data, China installed 295,000 industrial robots in 2024, accounting for 54% of global deployments and making it the world’s largest industrial robot market. China’s operational stock of industrial robots has exceeded 2 million units.

More importantly, in 2024, Chinese domestic suppliers surpassed foreign suppliers in China’s market for the first time, reaching a 57% local market share, compared with roughly 28% over the previous decade.

This shows that Chinese industrial robot companies are no longer relying only on low-cost competition. They have already completed a round of domestic validation inside the world’s densest, most complex, and fastest-updating manufacturing environment. China’s manufacturing sector is characterized by long supply chains, broad product categories, short delivery cycles, intense price pressure, and demanding customers. Automobiles, 3C electronics, photovoltaics, lithium batteries, semiconductors, home appliances, warehousing and logistics, e-commerce fulfillment, construction machinery, and metal processing together form a vast automation-demand field.

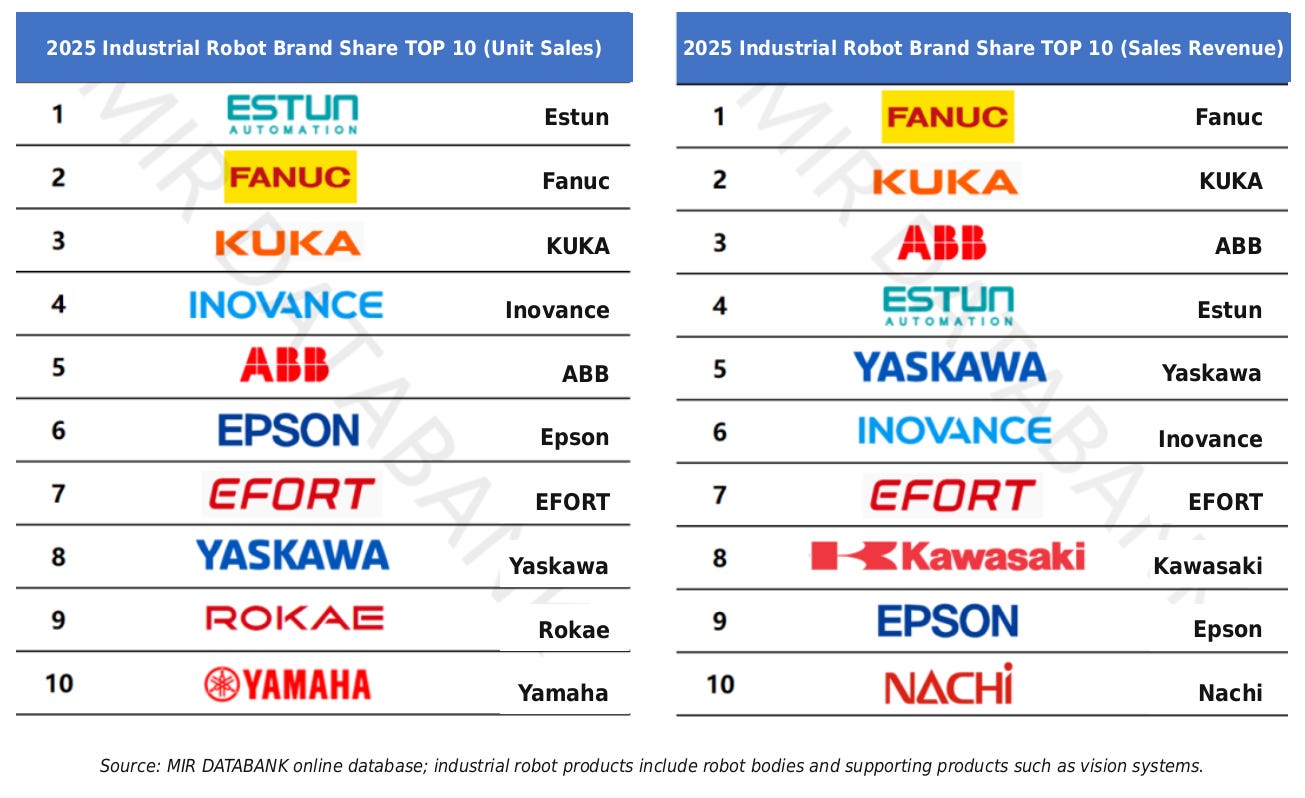

MIR DATABANK’s 2025 China industrial robot market data further illustrates this point. In 2025, China’s industrial robot sales exceeded 300,000 units for the full year, up more than 13% year on year. Fourth-quarter sales exceeded 91,000 units, up more than 16% quarter on quarter. Downstream demand came from electronics, automobiles, lithium batteries, semiconductors, and other sectors. Collaborative robots grew by more than 30%, while domestic substitution and embodied intelligence became core industry themes. MIR data also showed that China’s industrial robot exports grew 48.7% in 2025 and exceeded imports for the first time, making China a net exporter of industrial robots.

This path matters. Chinese industrial robot companies first endured price competition, scenario competition, and delivery competition at home, and only then acquired the capability to go overseas. The intensity of domestic competition compressed gross margins, but it also lowered the adoption threshold for automation. Many small and medium-sized manufacturers that previously could not afford expensive imported robotic systems can now purchase cheaper, easier-to-deploy, and more locally adaptable domestic solutions. This demand structure forced Chinese robotics companies to improve quickly in three directions: lower hardware costs, faster engineering deployment, and stronger after-sales responsiveness.

The industrial robot sector resembles China’s new-energy vehicles, photovoltaics, batteries, and construction machinery in one important respect. The domestic market is not simply an end market for sales. It is a continuous training ground for industrial capability. Companies face real customers, real production lines, real failures, real price pressure, and real delivery deadlines in the local market. Capability does not form in the laboratory alone. It forms through repeated engineering applications.

The underlying logic of China’s industrial robot exports lies here. China is not simply selling a machine overseas. It is carrying outward the cost control, flexible application capability, engineering modification experience, system integration, and fast delivery capability formed on Chinese manufacturing floors. For emerging markets in Southeast Asia, the Middle East, Latin America, and Eastern Europe that are absorbing manufacturing relocation, this capability is highly attractive. What many local companies need is often not the most expensive top-tier global robot, but an automation system that can rapidly improve efficiency, reduce labor dependence, adapt to multi-product production, and remain affordable.

This is also why China’s relatively low average export price for industrial robots still has strategic significance. A low unit price reflects product structure, and it also reflects the market-entry path. Chinese robotics companies first enter markets that are price-sensitive, deployment-sensitive, and scenario-adaptation-sensitive, then raise product complexity through local service and customer relationships. This process will not reshape the high-end global robotics landscape overnight. But it will gradually change the cost curve of global manufacturing automation.

3. Mobile Robots Are Going Global First: The Chinese Capability Incubated by E-Commerce, Warehousing, and Logistics

Among this wave of industrial robot exports, mobile robots are the segment most worth watching. Recent CCTV Finance coverage pointed out that the share of export orders for Chinese mobile robots rose rapidly from 25.87% in 2022 to 37.12% in 2024, and had already exceeded 40% in 2025. The report also noted that, by export destination, mature e-commerce, retail, and third-party logistics sectors in Europe, the United States, and Asia-Pacific have urgent demand for warehouse automation and stronger willingness to pay for technology. Demand for automation infrastructure in emerging markets such as Southeast Asia and the Middle East is also creating opportunities for Chinese mobile robots.

There is a clear industrial logic behind mobile robots going global first. They are more decentralized in application, have a wider range of scenarios, and are relatively more standardized. Their dependence on single-process precision is lower than that of some complex industrial robots. Warehousing, handling, sorting, factory logistics, production-line delivery, cross-floor transfer, and flexible warehouse management are all scenarios closely connected to the rapid development of China’s e-commerce, express delivery, third-party logistics, and smart warehousing systems over the past decade. Chinese companies did not first go overseas to search for mobile-robot scenarios. They had already completed long-term application training inside China’s ultra-large-scale e-commerce and logistics systems.

Chinese mobile robot companies have faced highly complex real-world conditions: vast warehouse space, enormous SKU counts, sharp order peaks and troughs, extreme pressure during promotional cycles, changing labor-cost structures, and customers with high requirements for system stability and turnover efficiency. Large numbers of mobile robot products have been repeatedly adjusted in these environments. Algorithms, path planning, dispatch systems, battery management, charging solutions, operations and maintenance systems, and software platforms have all iterated under real business pressure. This density of scenarios is the core asset of Chinese mobile robot companies.

CCTV Finance noted that Chinese mobile robots are moving from single-product exports toward comprehensive exports of “technology + solutions + services.” This shift is important. In the early stage of industrial robot exports, price and product functionality can open the market. But long-term revenue depends on system solutions, software adaptation, on-site debugging, equipment maintenance, spare-parts supply, customer training, and process redesign. Once robot products enter a customer’s production and logistics systems, they become part of a continuous service relationship rather than a one-off equipment sale.

This is also why mobile robots and traditional industrial robots have different overseas expansion rhythms. Traditional six-axis industrial robots entering automotive welding, final assembly, heavy-load handling, precision assembly, and other scenarios need higher customer-certification thresholds, longer validation cycles, deeper process understanding, and stronger brand trust. Mobile robots entering warehouse logistics and in-factory logistics are often evaluated more on investment payback period, system stability, deployment cycle, and scalability. Chinese companies have relatively strong advantages in these dimensions.

Data from Qichacha also shows that the industry has developed meaningful depth. As of May 25, 2026, China had 3,882 existing mobile-robot-related companies. Companies established more than 10 years ago accounted for the largest share, at 51.31%. Companies with registered capital of RMB 50 million or more accounted for 43.26%. This suggests that mobile robots are not a short-term fad. They have already formed a group of companies with long operating histories, heavy capital investment, and deep links with manufacturing and logistics systems.

From the perspective of China Industry Signals, the globalization of mobile robots is especially worth watching because it shows a typical diffusion mechanism of China’s industrial system. China first trains companies through vast domestic application scenarios, then sends mature products, engineering solutions, and service networks into overseas markets. What overseas customers are buying is not isolated hardware. It is a set of automation experience repeatedly validated in Chinese logistics, e-commerce, and factory settings.

4. From Following Supply Chains to Building Local Networks: The Overseas Path of Chinese Robotics Companies Is Deepening

The overseas expansion of Chinese industrial robot companies often began by following Chinese customers and global manufacturing supply-chain relocation. Jiemian News’ reporting on STEP provides a clear example. Sun Kun, STEP’s sales director, said the company plans to push aggressively overseas in 2026, identifying Southeast Asia as a strategic priority and Vietnam as the breakthrough market. STEP’s industrial robot products had already accumulated overseas application experience in 3C electronics manufacturing. Sun described this model as “borrowing a boat to go overseas”: products follow 3C and new-energy supply chains outward.

This shows that Chinese robotics companies did not initially face unfamiliar overseas customers independently. They entered overseas production lines by following familiar Chinese manufacturing customers and supply-chain partners. STEP’s SCARA robots and desktop six-axis robots followed customers such as Foxconn, Biel Crystal, and BYD, forming scaled applications in regional markets. Annual sales of related products have already exceeded 1,200 units. This case shows that China’s robot exports are deeply tied to the global migration of Chinese manufacturing. As Chinese companies build overseas factories and Chinese supply chains extend abroad, Chinese automation equipment naturally gains its first application scenarios.

This path has appeared repeatedly across many Chinese manufacturing sectors. The overseas expansion of photovoltaics, batteries, new-energy vehicles, consumer electronics, home appliances, construction machinery, energy storage, and power equipment all pulls equipment, automation, components, and service companies outward with it. Industrial robots are a critical part of that process. When Chinese manufacturers expand overseas, they need to replicate part of their domestic production efficiency and quality-control systems. Robotics companies following customers overseas can reduce customer-acquisition costs and build reference projects in real overseas settings.

Following customers is only the first stage. The more important part of Jiemian News’ reporting is that STEP is advancing localized registration and operating systems in Vietnam, moving from simple market entry toward local deepening. This shift means Chinese robotics companies are beginning to move from equipment suppliers to localized industrial-service providers. When overseas customers buy robots, their biggest concern is often not the specifications of a single machine. It is whether the system can run steadily, whether failures can be handled quickly, whether spare parts can arrive on time, and whether engineers can understand local factory needs.

Estun’s case shows a deeper path of globalization. A Securities Times interview with Estun president Wu Kan showed that the company has already built a four-brand matrix of “Estun,” “Cloos,” “Trio,” and “M.A.i,” covering different markets. Through internal development and strategic acquisitions, the company has filled product and technology gaps, including the acquisition of Trio in the UK, M.A.i in Germany, and German welding robot company Cloos. As of September 30, 2025, Estun had established 75 service outlets globally, employed 1,090 overseas staff, and covered manufacturing and economically developed regions across Europe, the Americas, and Asia.

These data points show that leading Chinese robotics companies already understand overseas expansion as a long-term organizational-capability project. Competition in overseas markets is not simply equipment quotation competition. It is comprehensive competition across product portfolios, channel networks, industry solutions, local engineering teams, certification capability, after-sales service, and brand trust. Estun’s revenue grew from RMB 487 million in 2015 to more than RMB 4 billion in 2024, with a compound annual growth rate of more than 25%. Its overseas revenue share rose from about 5% to more than 30%, while overseas gross margin has remained above 30%. This case shows that once Chinese robotics companies establish overseas service networks and brand matrices, overseas expansion can also become an important driver of profitability improvement.

The deepening of China’s industrial robot exports reflects three simultaneous shifts. First, Chinese manufacturing customers are expanding overseas, providing initial application scenarios for robotics companies. Second, overseas manufacturing itself faces automation demand, especially in e-commerce, logistics, auto parts, new energy, and electronics manufacturing. Third, Chinese robotics companies have built cost, iteration, and engineering-response capabilities through domestic competition, and are now adding localized service networks and international brand trust.

5. After Export Volume Breaks Out, China’s Robotics Industry Enters a More Difficult Upgrading Stage

The export breakthrough of Chinese industrial robots does not mean that the global high-end robotics landscape has already been rewritten. The gap between April export unit prices and import unit prices clearly indicates the industry’s boundary. Chinese companies are progressing rapidly in high-cost-performance products, mobile robots, SCARA robots, small six-axis robots, collaborative robots, warehouse logistics, and some new-energy and electronics manufacturing scenarios. They still need to accumulate capability in large-payload, high-precision, high-reliability, complex-process, automotive mainline, high-end welding, precision assembly, core control systems, reducers, servo systems, and global brand trust.

This does not weaken the long-term significance of China’s robotics exports. It shows that China’s robotics industry is in a typical upgrading stage: low-price volume growth is the first step, and real competition will gradually move toward product complexity, process understanding, system integration, software platforms, service networks, and industry ecosystems. Chinese companies once relied on the domestic market to form scale advantages. They now need to build long-term service capability in overseas markets. Without service networks, robots remain equipment. With service networks, robots can become part of a customer’s production system.

Industrial robots share one common feature with consumer electronics, new-energy vehicles, and photovoltaic modules: global customers ultimately buy reliability, efficiency, and payback periods. Price can open the market. Stability determines repeat purchases. Service capability determines long-term relationships. Industry solutions determine gross margins. For Chinese industrial robot companies to move from “selling products” to “selling systems,” they need to turn domestic manufacturing-floor experience into replicable overseas engineering capability.

This wave of overseas expansion will also reshape China’s robotics industry in reverse. Overseas customers’ safety certifications, compliance requirements, brand reviews, data interfaces, system compatibility, factory-management methods, and local labor structures all differ from those in China. Once Chinese companies enter markets in Europe, the United States, Japan, South Korea, Southeast Asia, the Middle East, and Latin America, they will face more complex industry standards and customer processes. This external pressure will push Chinese companies to improve documentation systems, quality systems, certification capabilities, remote operations and maintenance, and multilingual engineering services.

From the perspective of global manufacturing, China’s industrial robot exports carry a larger meaning. Over the past few decades, China has been the world’s largest manufacturing site. In the coming years, China is beginning to export the automation capabilities formed within that manufacturing site. Factories in Southeast Asia, logistics centers in the Middle East, warehouse systems in Europe, industrial parks in Latin America, and auto-parts plants in Mexico may all become new application scenarios for Chinese robotics companies. The outward diffusion of Chinese manufacturing includes not only factory relocation, but also the diffusion of equipment, processes, engineers, supply chains, and automation systems.

This is the early signal that China Industry Signals needs to capture. The April export figure of 25,375 units is only the surface-level number. The deeper change is that China’s robotics industry is moving from domestic substitution into global supply, from single-machine exports into solution exports, and from following customers into localized operations. The still-low average export price reminds us to keep the boundary of industrial judgment clear. The rapid growth in export volume shows that Chinese robotics companies have already gained an important entry point into the global diffusion of manufacturing automation.

The next stage of competition in Chinese industrial robots will no longer be determined only by who can make equipment cheaper. The decisive variable will be who can organize robots, software, processes, on-site service, supply chains, and customer production flows into a stable system. Chinese companies already possess experience trained in the world’s largest manufacturing environment. They now need to translate that experience into an industrial capability that global markets can accept, maintain, and continuously upgrade.

This is the real meaning of the April export data: Chinese industrial robots have begun to move out of Chinese factories, but what they carry with them is the system capability formed inside those factories over many years.

Source note: This essay is based on recent Chinese and international industry coverage and data from the National Bureau of Statistics of China, China Customs / GG Robot, CCTV Finance, Securities Times, Jiemian News, MIR DATABANK, IFR, and company investor-relations materials on China’s industrial robot production, exports, mobile robots, and overseas expansion.

Saw an interesting comment on Weibo regarding the coal mine disaster in China last week. “I wish the fancy dancing robots in Shenzhen could be programmed to work in our mines!”