CXMT IPO: China’s Memory Breakthrough Enters the AI Cycle

China’s DRAM champion is turning import substitution into production capacity, technology iteration, and supply-chain power.

The significance of CXMT lies in the fact that China has, for the first time, built an industrial platform in DRAM, a globally oligopolistic, capital-intensive, and fast-iterating strategic industry, that can sustain mass production, capacity expansion, technological iteration, and the upgrading of the domestic supply chain.

This essay is part of China Hard Tech Frontier Series.

Executive Summary

CXMT should be understood as a system-level industrial breakthrough, not just a semiconductor IPO. It represents China’s entry into one of the most capital-intensive and oligopolistic sectors of the global chip industry.

DRAM is one of the hardest semiconductor industries for latecomers. It requires simultaneous progress in process technology, yield learning, customer qualification, capacity scale, cost reduction, and cycle endurance.

CXMT has moved from China’s “zero-to-one” DRAM breakthrough into a global fourth-place position. Its 2019 8Gb DDR4 product marked the first real domestic DRAM breakthrough in mainland China, while its current portfolio now covers DDR4, LPDDR4X, DDR5, and LPDDR5/5X.

The AI memory cycle is changing CXMT’s strategic position. Strong AI and server demand has created structural DRAM undersupply, pushing prices higher and improving the earnings profile of memory manufacturers.

CXMT’s larger meaning lies in supply-chain training. Its expansion gives Chinese equipment, materials, testing, packaging, module, and downstream manufacturers a real mass-production verification environment.

DDR5 is the visible milestone; HBM is the next strategic test. DDR5 shows CXMT’s ability to enter mainstream server, PC, and terminal memory cycles, while HBM will determine how far it can move into the higher-value AI memory stack.

1. DRAM Is an Industry Where Latecomers Have Almost No Room to Survive

There are many difficult sectors in the semiconductor industry, but DRAM is among the least forgiving. It leaves very little breathing room for latecomers. Even if a company can make a product, it still has to continuously face yield, cost, capital expenditure, customer qualification, inventory cycles, product-generation migration, and the pricing discipline of global oligopolies. There is no light-asset story here, and there is no natural victory after a single technological breakthrough. DRAM is an industry that compresses technological capability, manufacturing capability, capital endurance, and cycle-management capability into the same company.

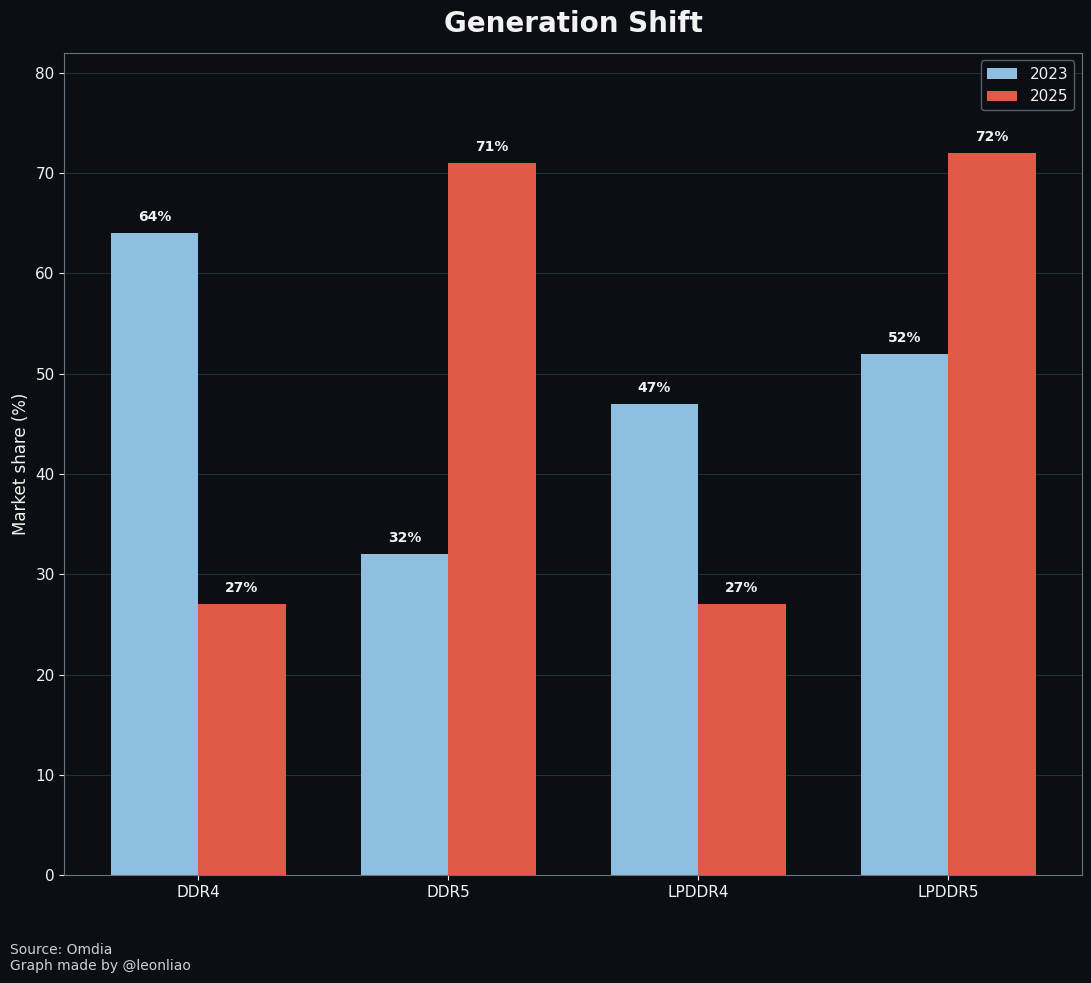

Over the past two decades, the global DRAM market has long been dominated by Samsung Electronics, SK hynix, and Micron Technology. The three companies have built extremely high barriers in technology roadmaps, capacity scale, customer relationships, capital expenditure, and cycle management. Once a latecomer enters, it must absorb losses during downcycles, expand capacity quickly during upcycles, continue investing during technology migration, and iterate repeatedly during customer qualification. More brutally, DRAM products never wait for the pursuer. CXMT’s prospectus shows that from 2023 to 2025, DDR products shifted rapidly from DDR4 to DDR5: DDR4’s market share fell from 64% to 27%, while DDR5 rose from 32% to 71%. LPDDR products also migrated from LPDDR4 to LPDDR5: LPDDR4 fell from 47% to 27%, while LPDDR5 rose from 52% to 72%.

This is the brutality of DRAM competition. Latecomers can hardly survive for long by relying on previous-generation products. Every mainstream product-generation shift re-tests process capability, design capability, validation capability, and customer-introduction capability. DDR4 has barely stabilized before the market moves to DDR5. LPDDR4X has barely formed a mass-production base before mobile terminals and high-end devices begin moving into LPDDR5/5X. For a new entrant, this means the chase always happens against a moving target.

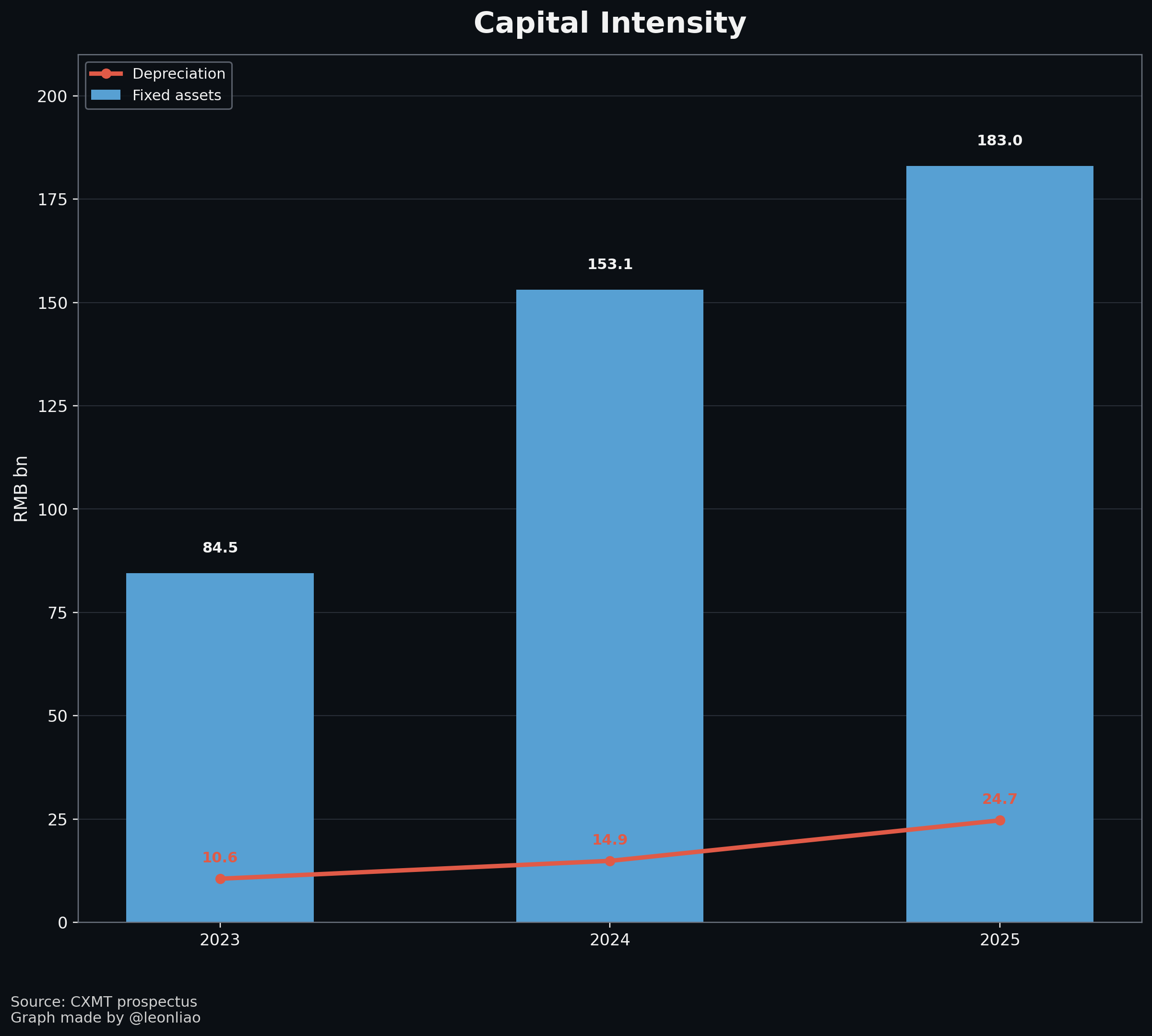

DRAM is also a typical heavy-capital industry. CXMT’s prospectus shows that from 2023 to 2025, the company’s fixed assets had book values of RMB 84.452 billion, RMB 153.132 billion, and RMB 183.024 billion, respectively, accounting for more than 40% and even more than 50% of total assets for a sustained period. Over the same period, fixed-asset depreciation reached RMB 10.555 billion, RMB 14.875 billion, and RMB 24.680 billion. These figures rarely appear in ordinary technology companies, but in DRAM they are part of the basic cost of entry. Once a production line is built, depreciation occurs every day. Once equipment is installed, the process must keep climbing the yield curve. Once capacity is released, the market pricing cycle again determines profit levels.

CXMT entered exactly this kind of industry. Its competitors are not regional players or single-product companies, but global memory giants such as Samsung, SK hynix, and Micron. The market it wants to enter is not a low-end replacement market, but the mainstream storage market jointly driven by servers, mobile devices, personal computers, smart vehicles, data centers, and AI infrastructure. The brutality of the DRAM industry forms the first layer of background for understanding CXMT: in this industry, survival itself is capability, and achieving scale means a higher level of industrial organization capability.

2. CXMT Has Moved from “Zero to One” into “One to Global Fourth”

CXMT was founded in 2016, and the moment that truly changed the position of mainland China’s DRAM industry came in 2019. That year, the company launched its independently designed and manufactured 8Gb DDR4 product, achieving a “zero-to-one” breakthrough for mainland China’s DRAM industry. The significance of this breakthrough was that mainland China formed, for the first time, a closed loop of independent R&D, design, manufacturing, and commercial mass production for a mainstream DRAM product.

In the semiconductor industry, there is a huge distance between “making it” and “mass-producing it.” There is an even longer distance between “mass-producing it” and “entering the customer system.” Between “entering the customer system” and “forming global market share,” there are still capacity, yield, cost, supply stability, and product-generation upgrade capability. The real importance of CXMT’s progress over the past few years lies in the fact that it has crossed several of these key thresholds.

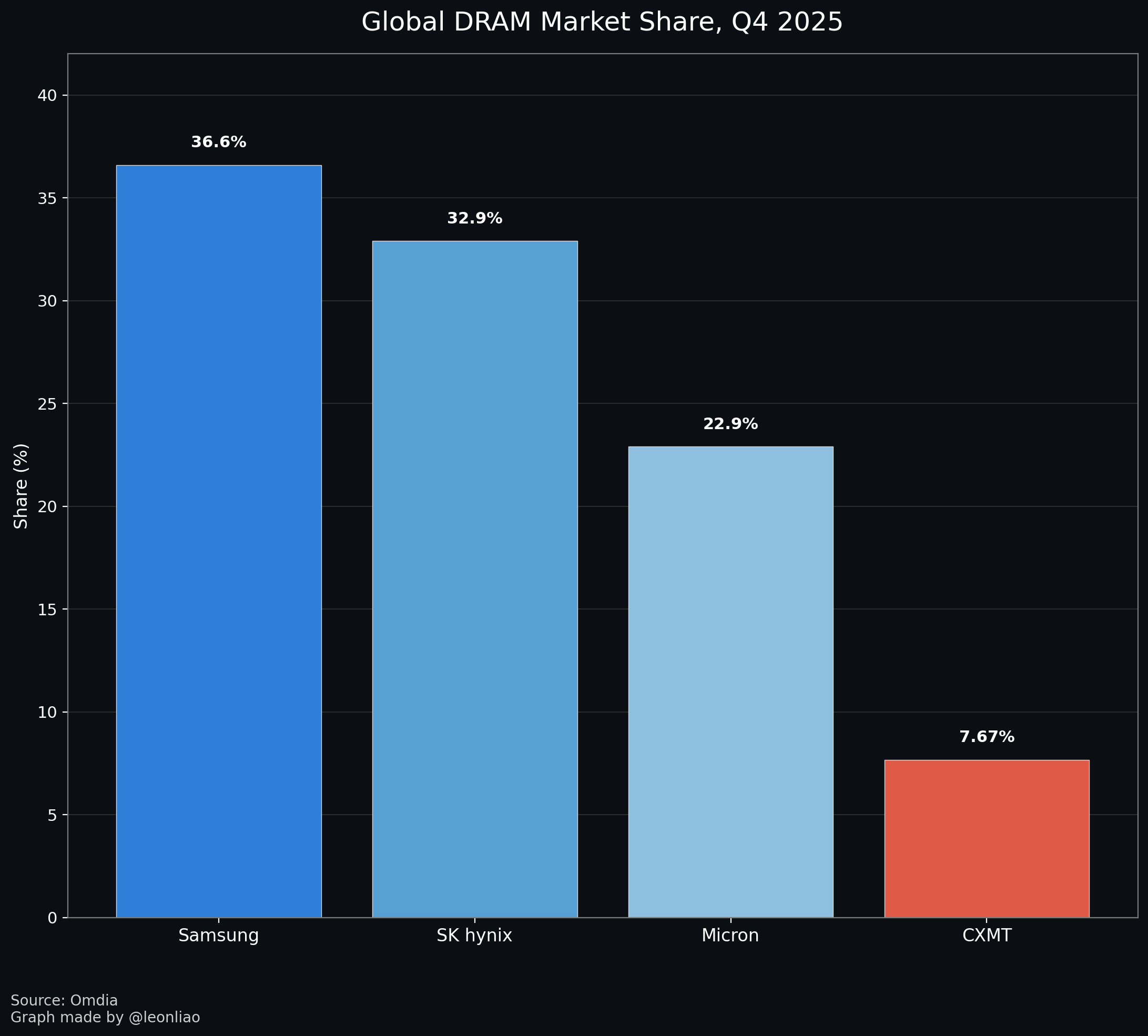

CXMT’s prospectus states that the company has become China’s largest, most technologically advanced, and most comprehensive DRAM R&D, design, and manufacturing integrated enterprise. The company has adopted a “generation-skipping R&D” strategy, completed mass production from its first-generation to fourth-generation process technology platforms, and achieved product coverage and iterative upgrades from DDR4 and LPDDR4X to DDR5 and LPDDR5/5X. It owns three 12-inch DRAM wafer fabs in Hefei and Beijing. According to Omdia statistics by capacity, shipments, and revenue, CXMT has become China’s No. 1 and the world’s No. 4 DRAM manufacturer, with a 7.67% market share in 4Q25.

This is an unusually rapid growth path. The 8Gb DDR4 product in 2019 proved that mainland China could make mainstream DRAM. The subsequent coverage of DDR5 and LPDDR5/5X shows that CXMT has begun entering mainstream product-generation migration. Its global fourth-place position means it has moved from the engineering-breakthrough stage into the industrial-share stage. “Zero to one” was a technological and engineering breakthrough; “one to global fourth” was a breakthrough jointly completed by manufacturing, capital, customers, and supply chains.

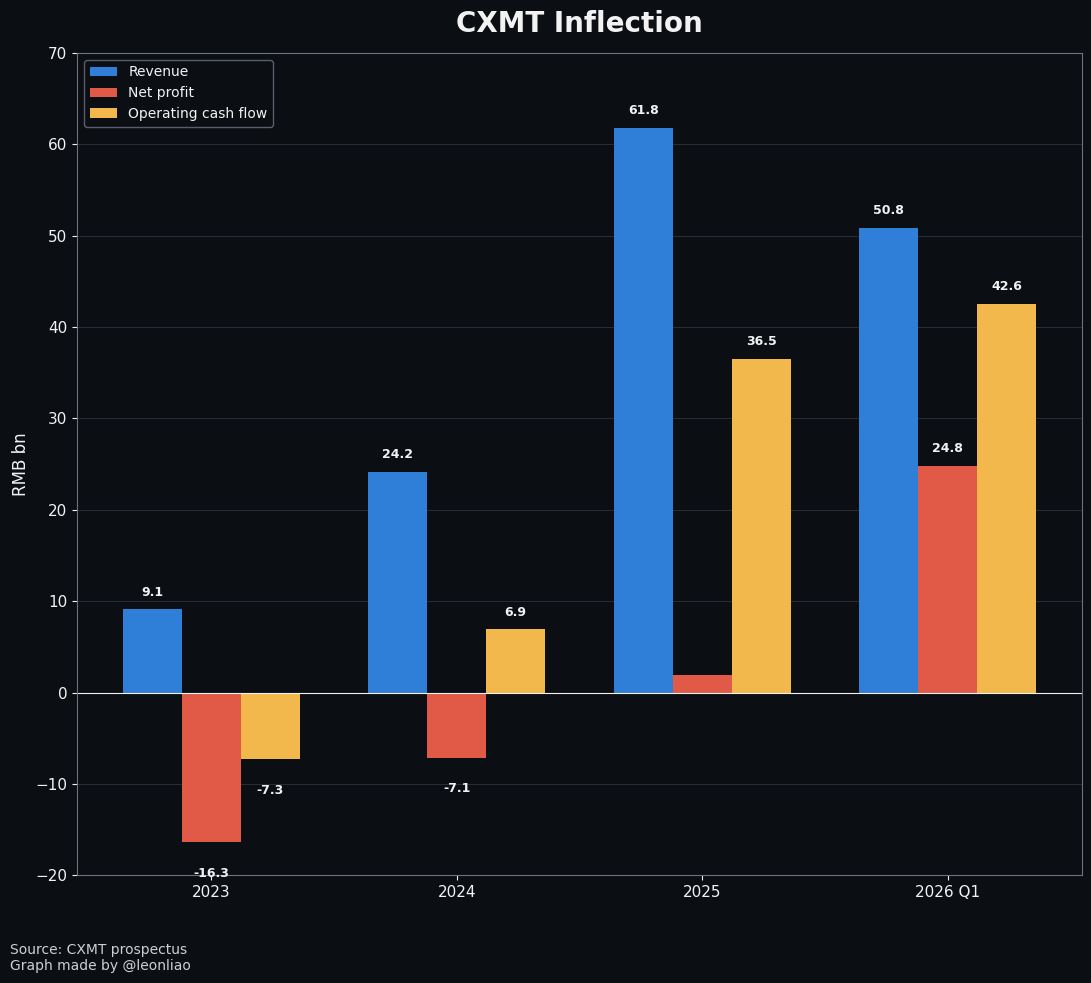

The financial data also shows this transition. In 2023, CXMT generated RMB 9.087 billion in revenue and recorded a net loss attributable to shareholders of RMB 16.340 billion. In 2024, revenue rose to RMB 24.178 billion, while the net loss narrowed to RMB 7.145 billion. In 2025, revenue reached RMB 61.799 billion, net profit attributable to shareholders turned positive at RMB 1.875 billion, adjusted net profit reached RMB 5.316 billion, and operating cash flow reached RMB 36.520 billion.

By the first quarter of 2026, cycle elasticity, capacity release, and price increases were amplified at the same time. CXMT’s updated prospectus shows that the company’s first-quarter 2026 revenue rose by more than 700% year on year to RMB 50.8 billion, with net profit of around RMB 25 billion. The company expects first-half 2026 revenue to reach RMB 110 billion to RMB 120 billion, with net profit attributable to shareholders potentially reaching RMB 57 billion.

This means CXMT has begun entering the most critical scale-effect stage of the DRAM industry. Early investment forms production lines. Production lines create supply. Supply enters the customer system. The customer system brings orders. Orders, in turn, improve yield, cost, and product mix. This is precisely the hardest part of the DRAM industry: without scale, costs are difficult to reduce; without cost reduction, profit is difficult to release; without profit release, the next round of technology and capacity investment is constrained. The financial changes that began appearing after 2025 show that this cycle is starting to turn.

3. The AI Memory Supercycle Is Changing CXMT’s Industrial Position

For many years, when the market discussed AI infrastructure, the first things that came to mind were GPUs, advanced process nodes, AI accelerators, data centers, and large models. Memory was often placed in a supporting role. Since the second half of 2025, however, the strategic position of memory inside AI infrastructure has become much clearer. AI servers, inference compute, cloud expansion, enterprise server upgrades, AI PCs, AI smartphones, and smart vehicles are all pulling DRAM demand upward again.

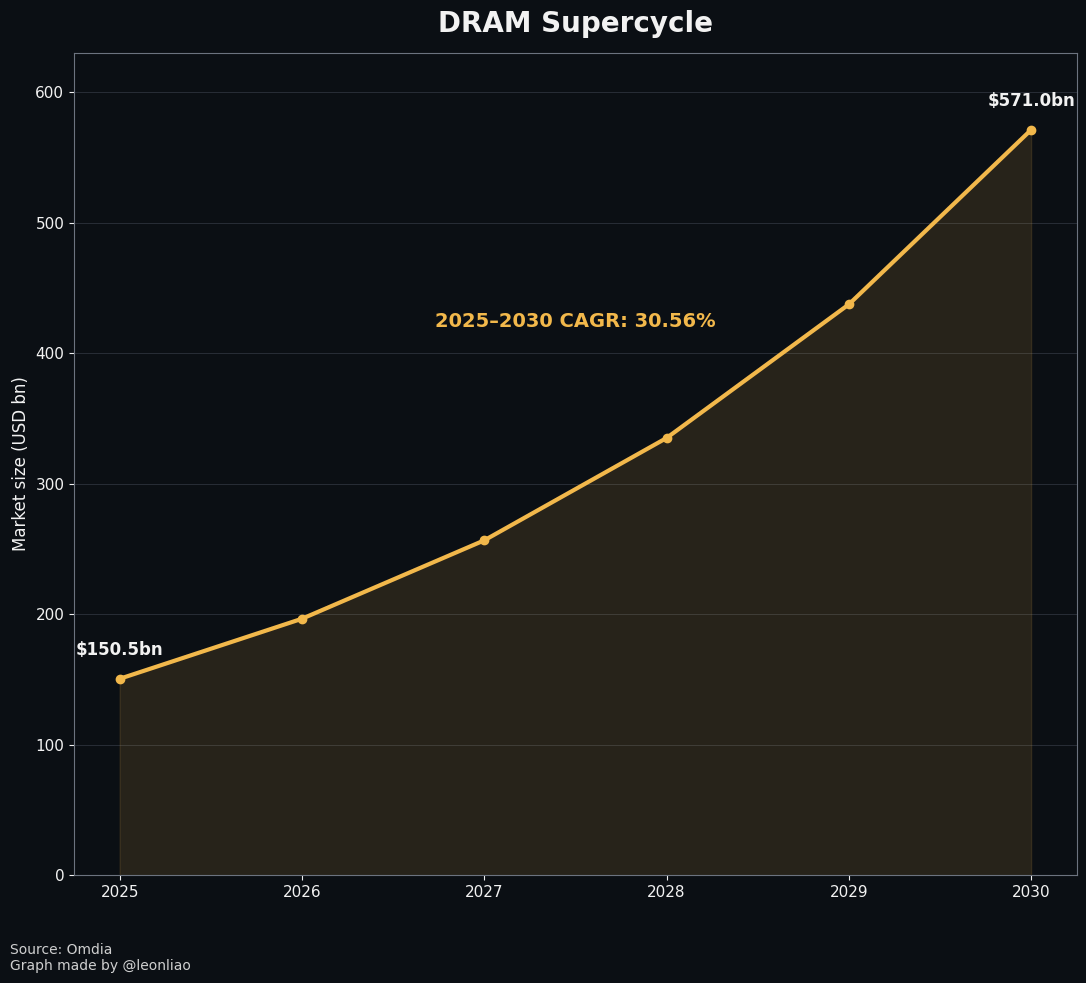

Omdia data shows that the global DRAM market is expected to grow from USD 150.5 billion in 2025 to USD 571.0 billion in 2030, representing a CAGR of 30.56%.

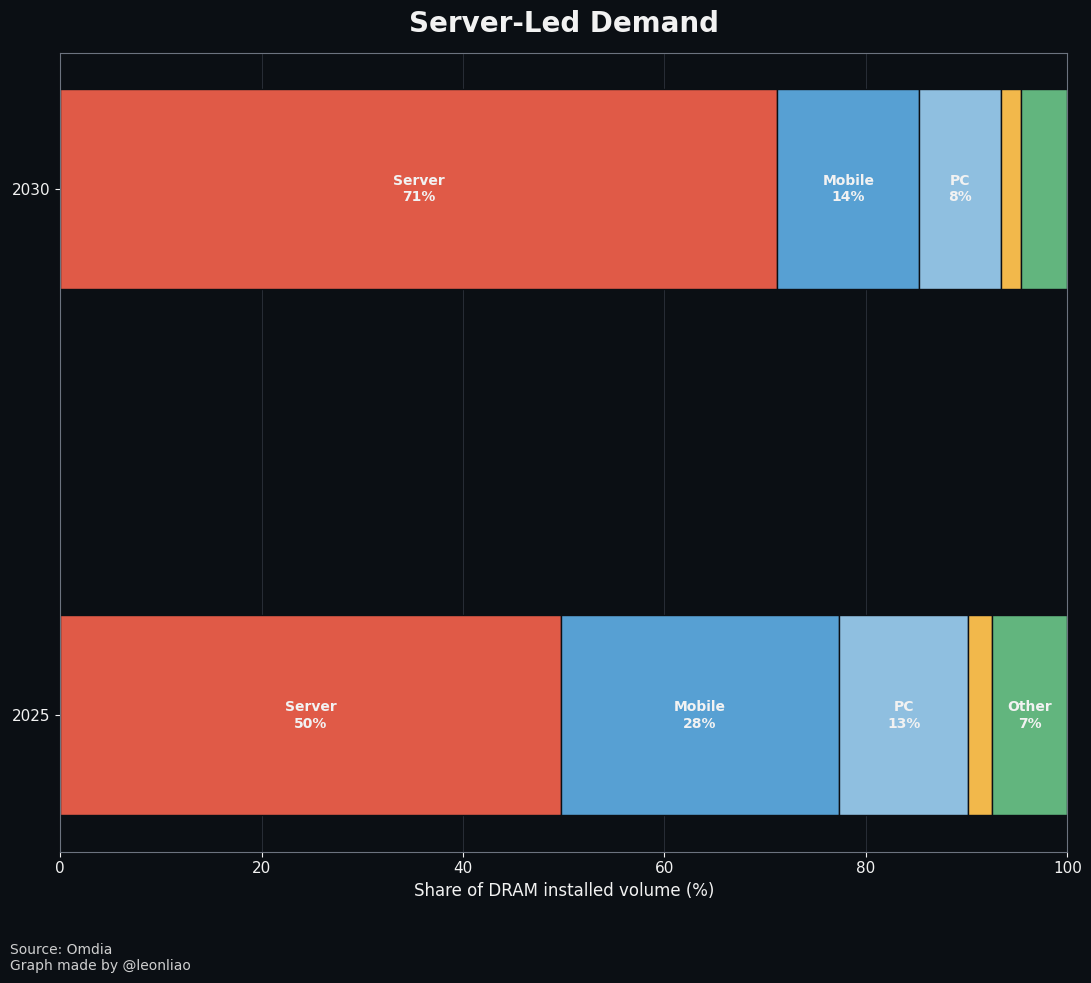

Server DRAM’s share is expected to rise from about 50% in 2025 to around 71% in 2030, while the relative share of mobile devices and PCs declines. TrendForce’s May 2026 DRAM market materials indicate that strong AI and server demand is creating structural DRAM undersupply, pushing both contract prices and spot prices higher. Supplier inventories have already bottomed, while cloud providers and PC manufacturers are actively locking in long-term contracts, and overall supply remains constrained. CXMT’s prospectus states that since the second half of 2025, continued growth in global compute demand and capacity adjustments by major chip manufacturers have caused DRAM demand to exceed supply, driving prices sharply higher.

This memory cycle is clearly different from previous PC or smartphone inventory cycles. In the past, DRAM price increases often came from consumer-electronics restocking, PC-cycle recovery, or smartphone shipment improvement. Now, AI data centers are pushing server memory, HBM, DDR5, RDIMM, MRDIMM, and other products into much greater importance. Large-model training requires high bandwidth and large-capacity memory. Inference expansion also requires more server deployment. Cloud providers, internet platforms, enterprise customers, and terminal-device manufacturers are all competing for more stable memory supply.

This provides CXMT with a special window. It did not enter the mainstream market during the calmest phase of the global DRAM market. It is entering an expansion cycle at a time when AI memory demand is being revalued, international giants are shifting capacity toward high-end servers and HBM, general-purpose DDR5 supply is tight, and demand for domestic substitution is rising. This window contains pricing-cycle factors, technology-upgrade factors, and supply-security factors at the same time.

China’s domestic market also provides a sufficiently large demand base. The prospectus clearly states that China is a major global DRAM consumption market, but the self-sufficiency rate of domestic-branded DRAM products remains low, leaving broad room for future development. This means CXMT does not need to depend entirely on overseas customer systems from the beginning. China’s servers, PCs, smartphones, smart vehicles, industrial control systems, consumer electronics, and data-center demand can themselves support a huge domestic-substitution market.

The AI memory supercycle has changed CXMT’s industrial position. It is no longer merely a DRAM company filling a gap in China’s semiconductor industry. It is also becoming a key variable in China’s memory foundation for the AI era. GPUs determine the upper limit of compute. Memory determines the efficiency of data movement. Server memory determines system throughput. HBM determines the performance boundary of high-end AI accelerators. If China wants to build its own AI infrastructure system, memory capability must be one of its foundational stones.

4. Technology-Generation Upgrading: From DDR4/LPDDR4X to DDR5/LPDDR5X

The real threshold in the DRAM industry lies in continuous iteration. Being able to launch DDR4 is the starting point. Being able to follow the market as it migrates to DDR5 and LPDDR5/5X means the company is beginning to approach the mainstream demand curve.

The “generation-skipping R&D” described in the prospectus deserves attention. The company has moved from its first-generation process technology platform to its fourth-generation process technology platform, and has completed product coverage from DDR4 and LPDDR4X to DDR5 and LPDDR5/5X. This means CXMT has not stayed on a single generation of products, but is compressing the catching-up cycle. For a later entrant, following the conventional rhythm of slowly catching up generation by generation can easily lead to a situation in which the market has already moved to the next generation by the time one generation is completed. The meaning of generation-skipping R&D is to shorten the time gap with international mainstream products through higher-intensity R&D organization and manufacturing iteration.

CXMT’s official website shows that its DDR5 die has a peak speed above 8000Mbps, with capacities covering 16Gb and 24Gb. Power consumption is 20% lower than DDR4, and the company has introduced multiple module forms covering enterprise servers, workstations, desktops, and laptops. For LPDDR5X, the company offers 12Gb and 16Gb single-die capacities, with peak speeds reaching 10667Mbps, 66% higher than the previous-generation LPDDR5, while reducing power consumption by 30%.

DDR5 represents the mainstream upgrade direction for servers, PCs, workstations, and data-center memory. LPDDR5/5X is tied to smartphones, tablets, lightweight laptops, wearables, and mobile AI terminals. CXMT’s entry into these product generations means Chinese DRAM is beginning to enter growing mainstream markets, rather than only satisfying mature previous-generation demand.

Recent SCMP reporting indicates that Chinese memory-module manufacturers are accelerating the launch of consumer-grade and enterprise-grade products based on CXMT DDR5 chips. For example, Powev’s Sinker DDR5 server memory has entered mass production and delivery, and its 64GB DDR5-5600 RDIMM products have passed testing by several major customers. Other Chinese companies have also introduced industrial-grade and enterprise-grade DDR5 products based on CXMT die.

More notably, Tom’s Hardware recently reported that CXMT DRAM has appeared in Corsair Vengeance DDR5 16GB memory modules sold in the Chinese market, with DDR5-6000 CL36 specifications and support for Intel XMP and AMD EXPO. Corsair has traditionally sourced DRAM from Samsung, SK hynix, and Micron. This change shows that CXMT DDR5 has begun touching a more mainstream branded hardware product chain.

These developments show that CXMT’s DDR5 has entered the validation process among module makers, branded hardware companies, and terminal markets. For DRAM, this is a crucial step. Only when chips enter modules, modules enter customers, customers pass testing, and products form stable delivery can industrial capability truly be accumulated.

5. CXMT’s Real Significance Is That It Gives China’s Memory Supply Chain Its First Large-Scale Verification Window

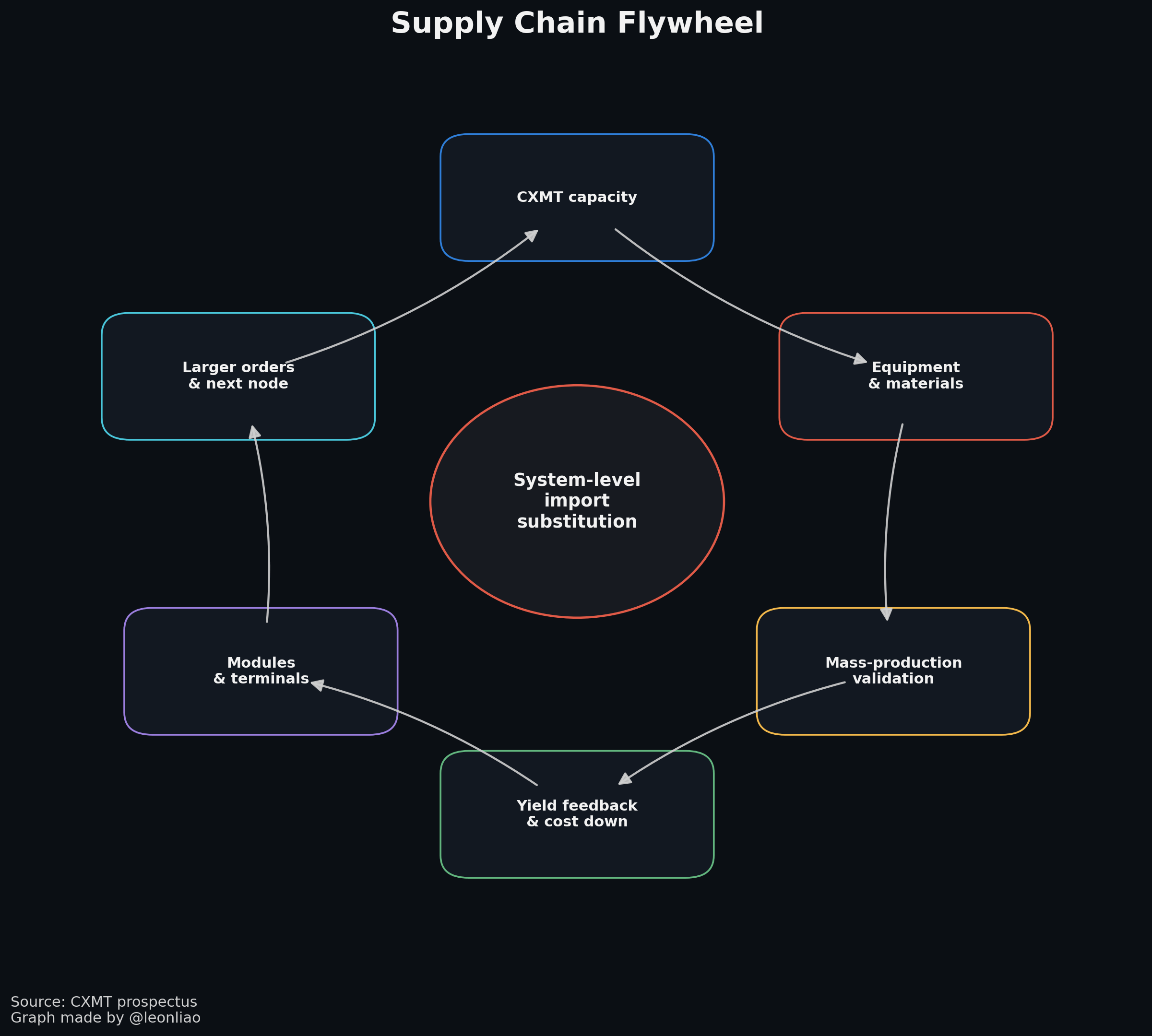

The deepest significance of CXMT lies in the supply chain. Over the years, China’s semiconductor industry has accumulated many equipment, materials, components, packaging, testing, EDA, and module companies. But these companies have long faced a common constraint: they lacked a sufficiently stable, sufficiently high-specification, and sufficiently large-scale domestic mainstream production line for validation. The capability of semiconductor equipment and materials cannot be proven only in the laboratory. They must enter mass-production lines and be tested in real process environments for yield, stability, lifetime, contamination control, batch consistency, and cost.

In the section explaining its listing purpose, CXMT’s prospectus explicitly states that the company’s development can drive coordinated development across core parts of the industry chain, including “memory chip design companies, EDA vendors, semiconductor material suppliers, semiconductor equipment and component suppliers, module manufacturers, and downstream terminal application manufacturers,” thereby improving the overall strength of China’s integrated-circuit industry chain.

A DRAM production line is a training ground for the semiconductor supply chain. Etching equipment, thin-film deposition equipment, CMP equipment, cleaning equipment, metrology and inspection equipment, photoresist, electronic specialty gases, targets, wafers, precursors, polishing slurry, packaging materials, and testing equipment all need to be validated in mass-production environments. Without a mainstream production line, domestic suppliers can only remain in the stages of samples, trials, and partial replacement. With an expansion platform like CXMT, the supply chain has the opportunity to form a stable feedback loop.

Recent reporting from Economic Observer also placed this issue inside the supply-chain validation context. The report argued that the key constraint on the development of domestic equipment and materials lies in the lack of large-scale mass-production validation scenarios. CXMT and YMTC, with standardized manufacturing platforms and stable expansion rhythms, have built domestic validation loops. Because memory-chip process platforms are highly standardized, once equipment or materials are validated and introduced on one generation of a platform, subsequent capacity replication can be rapidly rolled out, and the commercialization cycle can be shortened.

This is exactly the most important capability-formation mechanism in China’s industrial system. Industrial capability does not naturally emerge from papers, policy documents, or one-off projects. It is trained inside production lines, forced out under order pressure, polished through customer validation, and solidified through cost reduction and yield improvement. Industry is the greatest university. CXMT’s expansion will bring upstream equipment and materials companies into a more intense real-world classroom.

This supply-chain training has already begun to appear in specific segments. In CXMT’s DRAM production-line capital expenditure, etching and thin-film deposition equipment together account for roughly 50%, while metrology and inspection equipment accounts for around 12% to 15%. The penetration rate of domestic equipment in domestic memory production lines is rising. CMP and cleaning equipment have relatively high domestic substitution levels. Etching and thin-film deposition are in a phase of rapid penetration. Metrology and inspection, coating and development, and related segments remain weaker points. Chinese semiconductor equipment companies such as Naura, AMEC, Piotech, Hwatsing Technology, and Jingce Electronic are gaining more industrialization opportunities in etching, thin-film deposition, CMP, testing, and related areas.

A similar shift is occurring on the materials side. CXMT’s 2025 raw-material procurement table shows that the company’s total raw-material purchases reached about RMB 11.47 billion, of which chemicals accounted for 37.29%, photoresist 12.16%, wafers 8.55%, and electronic specialty gases 5.10%. At the same time, Chinese domestic companies including Yoke Technology, Anji Microelectronics, Huate Gas, Jinhong Gas, Guangzhou Gas, and GigaDevice-adjacent materials and service suppliers are accelerating introduction across different material segments.

This shows that CXMT’s industrial significance has already moved beyond the company itself. It provides China’s memory supply chain with a large-scale verification window. Domestic equipment companies need it. Domestic materials companies need it. Domestic module companies need it. Terminal manufacturers need it as well. Without this kind of mainstream manufacturing platform, domestic substitution can only be scattered, partial, and project-based. With continuous expansion and generational upgrading, domestic substitution begins to enter the stage of system training.

6. DDR5 Is the Visible Progress; HBM Is the Next Strategic Test

The clearest visible progress for CXMT today is DDR5. It already has products, specifications, modules, downstream manufacturers, and market feedback. DDR5 is directly tied to demand from servers, PCs, workstations, and data centers, and it is also tied to China’s supply security in general-purpose server memory and enterprise memory. The DDR5 breakthrough brings CXMT into the growing mainstream memory curve.

HBM is the next strategic test. AI accelerators require higher memory bandwidth and more advanced packaging integration. HBM has already become a critical component for Nvidia, AMD, Google TPUs, various AI ASICs, and high-end training and inference systems. The global HBM market is currently dominated by SK hynix, Samsung, and Micron, and the entry threshold is higher than for ordinary DDR5. It involves not only DRAM die capability, but also stacking, TSV, advanced packaging, thermal management, testing, yield, and deep coordination with AI accelerator customers.

CXMT plans to raise about RMB 29.5 billion through a Shanghai listing to upgrade production facilities, support advanced DRAM technology R&D, and expand product lines, including HBM for AI processors and related applications.

It is important to keep the boundary of judgment clear. DDR5 has already entered a relatively clear product and market validation stage. HBM remains in a much more difficult stage of technological assault. CXMT’s current foundation remains DDR, LPDDR, and other general-purpose DRAM products. These products support the company’s scale, revenue, cash flow, and supply-chain diffusion. HBM is the strategic direction and the next key test of whether China’s memory industry can move further into the higher-value segment of the AI compute chain.

From an industrial-structure perspective, DDR5 and HBM represent two different levels. DDR5 determines whether China can form mainstream supply capability in servers, PCs, workstations, terminals, and enterprise memory. HBM determines whether China can form a deeper memory capability inside AI accelerators and high-end compute systems. The former is closer to large-scale domestic substitution. The latter is closer to a high-end position in the AI compute chain.

If CXMT can continue expanding its share in DDR5, enter more terminal scenarios with LPDDR5/5X, and gradually complete R&D, packaging, validation, and customer introduction in HBM, China’s memory industry will continue moving up the hierarchy. This upward movement will not happen overnight, but the direction is clear: from general-purpose DRAM to server memory, from server memory to high-bandwidth memory, from single chips to memory systems, and from domestic die to a domestic supply-chain loop.

7. CXMT Reflects China’s Industrial Organization Form of State Capacity

CXMT’s development path is difficult to explain as a simple market-startup story, and it is equally difficult to summarize as a simple policy-support story. It reflects a Chinese-style strategic industrial organization model: local governments provide long-term industrial carrying capacity, state capital provides strategic patient capital, industrial capital and downstream ecosystems provide demand connections, engineering teams complete technology roadmaps and production-line ramp-up, and the domestic supply chain is trained in real mass production.

The shareholder structure in the prospectus already reflects this pattern. The National Integrated Circuit Industry Investment Fund Phase II, Anhui Investment Group, Hefei industrial capital, Xiaomi’s Yangtze River Industry Fund, Alibaba Network, Midea Investment, the China State-Owned Enterprise Structural Adjustment Fund, and financial-asset investment institutions all appear among CXMT’s related shareholders. These capital sources are not the same. Behind them are different functions: national strategic capital, local industrial capital, market-based financial capital, downstream ecosystem capital, and supply-chain coordination capital.

This kind of organization is especially important in an industry like DRAM. Ordinary venture capital can hardly bear a ten-year investment cycle and large-scale loss pressure on its own. A single local government can hardly complete technology roadmaps, international talent recruitment, production-line equipment, customer validation, and supply-chain construction by itself. Entrepreneurial spirit alone cannot solve DRAM’s capital intensity and technological catch-up problem. CXMT’s growth required a system capable of organizing capital, land, infrastructure, talent, equipment, materials, customers, and policy expectations around the same industrial objective.

This is the concrete form of China’s state capacity at the industrial level: the ability to maintain project continuity during long loss-making periods; the ability to provide infrastructure and capital-bearing capacity for high-capital-intensity industries; the ability to align national capital, local capital, and industrial capital around the same target; the ability to push domestic supply-chain introduction in real demand markets; and the ability to allow R&D, manufacturing, customers, and suppliers to iterate repeatedly around the same production line.

Hefei is a typical example of this capability. From display panels and new-energy vehicles to semiconductors, Hefei has long demonstrated an ability to organize industrial capital and strategic projects through local government. CXMT grew out of precisely this kind of local industrial organization environment. This is a form of sustained coordination among local government, industrial platforms, capital tools, engineering teams, and supply-chain ecosystems. It is a development path with distinctly Chinese characteristics.

Chinese-style industrial policy is often misunderstood from the outside as a list of subsidies. CXMT shows that what matters more is organizational capability. Subsidies can reduce early-stage costs, but they cannot replace yield ramp-up. Capital can provide time, but it cannot replace technological iteration. Policy can provide direction, but it cannot replace customer validation. Local governments can provide carrying capacity, but they cannot replace market competition. Only when these elements are organized around the same industrial goal and repeatedly tested in real markets can state capacity be transformed into company capability and supply-chain capability.

More importantly, CXMT has changed the level of China’s semiconductor import substitution. In the early stage, China’s semiconductor substitution was concentrated more in certain chip-design categories, low-end components, packaging and testing, mature processes, and parts of the equipment and materials chain. Later, domestic substitution began moving into EDA, semiconductor equipment, advanced packaging, memory, AI chips, and high-end materials. The DRAM segment where CXMT operates pushes domestic substitution into a more difficult level.

The difficulty of this level comes from several dimensions. First, DRAM is a global oligopoly, and latecomers face giants such as Samsung, SK hynix, and Micron with decades of accumulated strength. Second, DRAM is a strongly cyclical industry, where price movements amplify both profits and losses. Third, DRAM is a heavy-capital industry, with enormous capacity-building and depreciation pressure. Fourth, DRAM is a continuously iterating industry, where generational shifts from DDR4 and DDR5 to LPDDR5 and HBM keep forcing companies to invest. Fifth, DRAM is a supply-chain-intensive industry, where equipment, materials, packaging, testing, modules, and terminals must advance together.

CXMT’s emergence shows that China’s semiconductor import substitution is moving from point substitution to system substitution. Point substitution asks whether a single chip can be made. System substitution asks whether an industrial chain can sustain mass production, continuous validation, cost reduction, and technological upgrading. Point substitution can rely on a small number of engineering teams for breakthrough. System substitution requires capital, manufacturing, supply chains, customers, and state capacity to act together.

This is also what distinguishes CXMT from many ordinary semiconductor companies. Its significance lies not only in filling mainland China’s DRAM gap, but also in providing a platform for China’s memory supply chain to evolve collectively. Domestic equipment needs it for introduction. Domestic materials need it for validation. Domestic modules need it for supply. Domestic terminals need it for supply security. China’s capital market needs it to demonstrate the long-term value of hard-tech manufacturing enterprises. China’s AI infrastructure also needs it to complete the memory foundation.

From the 8Gb DDR4 product in 2019 to today’s DDR5, LPDDR5/5X, three 12-inch wafer fabs, China’s No. 1 position, and global No. 4 ranking, CXMT’s trajectory shows that China’s semiconductor industry has entered a deeper stage. This stage is more capital-intensive, more dependent on system organization, closer to the core of global industry, and more demanding of long-term patience.

DRAM was once an industry that left almost no space for latecomers. CXMT has squeezed into that space. What it must now prove is whether a Chinese company can continue expanding capacity, catching up technologically, introducing customers, training the supply chain, and occupying a higher position in the memory restructuring of the AI era.

The real sign that China’s semiconductor import substitution has entered deep water is the formation of a global-scale, heavy-capital manufacturing platform. CXMT’s value lies precisely here: it has brought Chinese DRAM from long-term absence into scaled manufacturing, pushed domestic substitution from the product level to the supply-chain level, and advanced state capacity from policy expression into the industrial reality formed by production lines, equipment, materials, customers, and cash flow.