Inside Sungrow’s New Energy Infrastructure Bet

China’s inverter champion is turning storage, global factories, and AI power systems into one integrated platform.

Sungrow’s story is no longer only about selling solar equipment. It is about how China’s clean-energy companies are learning to export infrastructure systems.

This essay is part of China Industry Signals.

Executive Summary

Sungrow is one of China’s most important clean-energy equipment companies and a global leader in photovoltaic inverters and energy-storage systems. Founded in Hefei in 1997, the company built its position through power electronics, solar inverters, storage systems, and large-scale renewable-energy project solutions, and is now becoming a global energy-infrastructure platform.

Chinese industry media are focusing on a major shift inside Sungrow: storage has overtaken solar inverters as its largest business. In 2025, Sungrow’s energy-storage systems generated RMB 37.287 billion in revenue, accounting for 41.81% of total revenue, while overseas revenue reached RMB 53.992 billion, or 60.54% of total revenue.

Sungrow’s recent 7.5GWh Middle East storage order shows that Chinese clean-energy companies are moving from product exports to national-scale energy-system delivery. The Masdar RTC project in the UAE requires storage, inverters, grid adaptation, thermal management, long-duration operation, and local delivery capability.

The company’s second Hong Kong listing attempt reveals the capital intensity of China’s next stage of clean-energy globalization. Sungrow already has substantial cash, but overseas manufacturing in Poland and Egypt, large-scale project execution, inventory, receivables, and localization requirements are making the business heavier.

Sungrow’s move into AIDC power systems connects China’s renewable-energy industry with the AI infrastructure cycle. AI data centers require stable, high-voltage, high-density, low-loss power systems, and Sungrow’s power-electronics, storage-converter, HVDC, and solid-state transformer capabilities give it a credible entry point.

The deeper signal is that China’s clean-energy competition is shifting from low-cost manufacturing to system integration. The next battlefield is not only cheaper solar modules or batteries, but storage systems, grid-forming capability, overseas engineering, local factories, AI power infrastructure, and the ability to deliver complex energy projects under demanding conditions.

1.Chinese Solar-Storage Companies Are Entering the Stage of System-Based Global Expansion

On May 21, Sungrow announced that it had signed an agreement with UAE renewable-energy company Masdar to supply 7.5GWh of PowerTitan 3.0 liquid-cooled energy-storage systems and 2.6GW of photovoltaic inverters for the UAE RTC, or Round-The-Clock, 1 Plant North project. The Paper and several energy-industry media outlets noted that this is another gigawatt-hour-scale order Sungrow has secured in the Middle East, following its 7.8GWh energy-storage project in Saudi Arabia. The project is expected to be connected to the grid in 2027 and, once completed, is expected to reduce carbon emissions by about 5.7 million tons per year.

This kind of order can no longer be understood simply as a Chinese company selling a batch of storage cabinets or inverters. Solar-storage projects in the Middle East face a full set of requirements: high temperatures, sand and dust, weak grids, long-duration operation, grid-forming capability, project delivery, and local service. In its coverage of the project, Tansuo Storage emphasized that PowerTitan 3.0 needs to operate at full power in a 55°C environment, while adapting to the Middle East’s complex grid conditions through liquid cooling, silicon-carbide PCS, thermal management, and grid-forming capability. The report also noted that the project uses 684Ah stacked cells, and that a 1GWh power station occupies 22% less land than the previous-generation system.

This is the most important thing to watch about Sungrow recently: it is no longer merely a photovoltaic inverter company. It is becoming a global energy-infrastructure system supplier. Many overseas analysts have understood Chinese solar mainly through modules, silicon wafers, solar cells, and price competition. But Sungrow represents another line within China’s new-energy industry: power electronics, energy-storage systems, solar-storage integration, grid adaptation, overseas project delivery, and large-scale energy-engineering system integration.

Founded in 1997 and headquartered in Hefei, Anhui, Sungrow began with photovoltaic inverters. A solar inverter converts the direct current generated by solar modules into alternating current that can be connected to the grid and used. This link may sound less intuitive than silicon wafers, solar cells, or modules, but it is one of the core control nodes in a photovoltaic power-generation system. Sungrow later extended its technical capabilities into wind-power converters, energy-storage systems, electric-vehicle control systems, charging equipment, hydrogen-energy equipment, and smart-energy operation and maintenance. The company’s official website defines it as an enterprise focused on the research, development, production, sales, and service of new-energy power equipment for solar, wind, energy storage, electric vehicles, and related fields.

Sungrow is essentially a representative of China’s power-electronics capability inside the clean-energy industry. It does not produce upstream polysilicon, nor is it a typical solar-module manufacturer. Its position is closer to the conversion, control, storage, and grid-connection layer of the new-energy power system. As the share of renewable energy rises, this layer is becoming increasingly important.

2.Storage Has Overtaken Inverters, and Sungrow’s Business Center of Gravity Has Changed

Energy storage is moving from a supporting technology to the central infrastructure layer of the renewable-energy system.

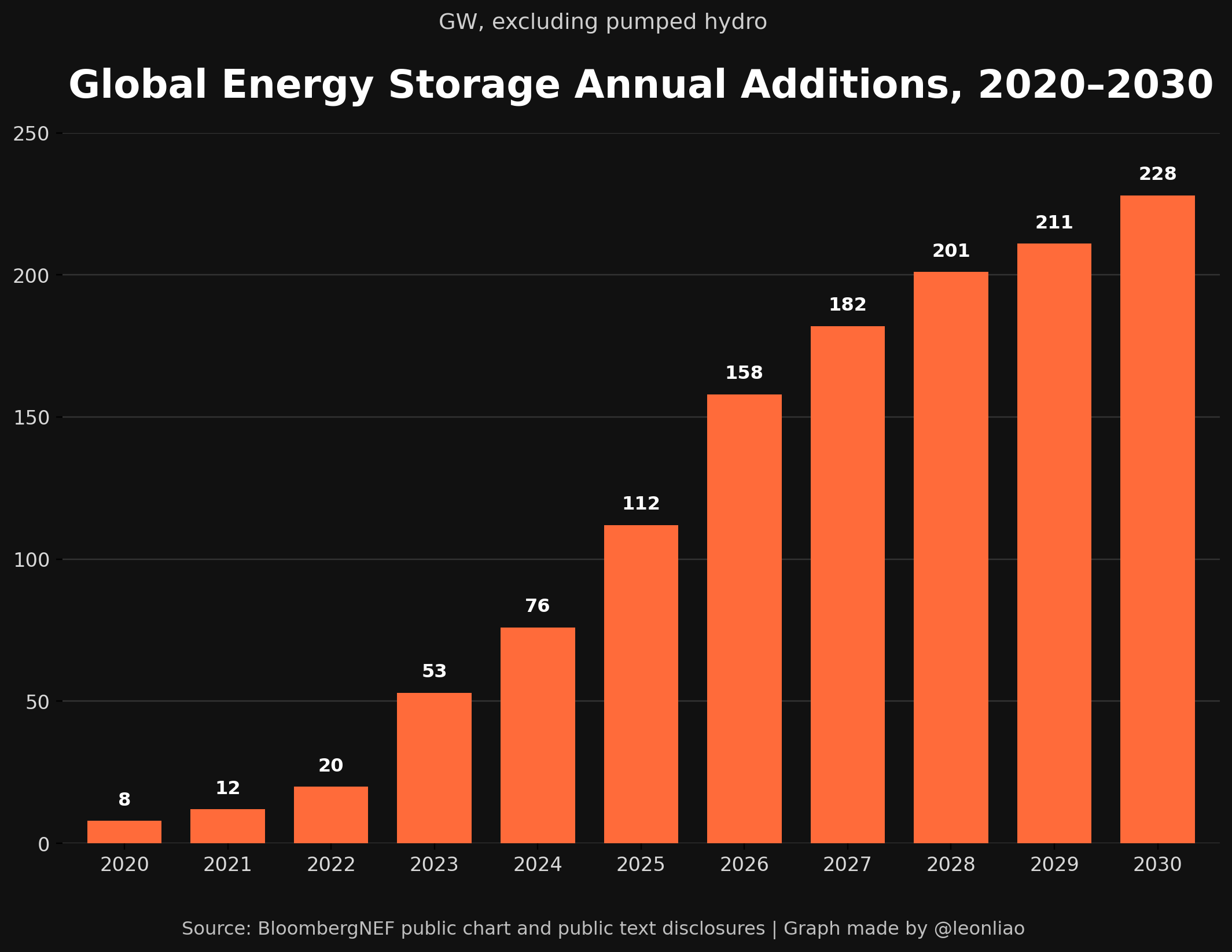

Global annual energy storage additions rose from roughly 8GW in 2020 to 112GW in 2025, and the market is moving toward more than 200GW a year by 2030. This is not ordinary industrial growth. It is the moment when solar and wind deployment begins to require a second system: batteries, grid-forming storage, power electronics, dispatch software, and system integration that can turn intermittent generation into usable electricity.

This is why Sungrow matters. It is no longer just a photovoltaic inverter company.

Recent Chinese media coverage of Sungrow has one common focus: energy-storage systems have overtaken photovoltaic inverters to become Sungrow’s largest source of revenue.

According to its 2025 annual report, Sungrow generated about RMB 89.184 billion in revenue, up 14.55% year on year, and about RMB 13.461 billion in net profit attributable to shareholders, up 21.97% year on year. Its global energy-storage system shipments reached 43GWh, generating RMB 37.287 billion in revenue, up 49.39% year on year. Storage accounted for 41.81% of total revenue, up from 32.06% in 2024. Revenue from photovoltaic inverters and other power-electronics conversion equipment was RMB 31.136 billion, accounting for 34.91% of total revenue.

This change is highly significant. Sungrow was long viewed by capital markets and the industry as a photovoltaic inverter leader, and its valuation logic was mainly built around solar installations, inverter shipments, overseas markets, and utility-scale power-station demand. Now that storage has become its largest business, the company’s revenue structure, customer structure, project cycle, working-capital profile, technical requirements, and risk exposure are all changing.

Storage and inverters both appear to be new-energy equipment businesses, but their business models are different. Inverters are closer to standardized power-electronics equipment. Although they also require large-project delivery and overseas certification, they are generally more productized. Energy-storage systems are more complex. They involve cells, PCS, BMS, EMS, thermal management, fire safety, grid-connection control, project-return calculations, local power-market rules, and long-term operation and maintenance. Customers are not buying just a piece of equipment. They are buying a system that can continue operating and generating value in complex grid and commercial environments.

According to an interview by Industry Depth with Xu Qingqing, president of Sungrow’s energy-storage business unit, energy-storage competition is shifting from static product performance to dynamic scenario capability. The core issue is no longer just cell capacity, cycle life, or equipment parameters, but whether a system can create long-term value under different electricity markets, grid conditions, and revenue models. The report summarized Sungrow’s storage approach as “three-electric integration,” grid-forming capability, software algorithms, grid understanding, and multi-scenario solutions.

This is important for understanding China’s energy-storage industry. External narratives have often reduced China’s new-energy advantage to low-cost manufacturing and government subsidies. But in energy storage, low cost explains only part of the competitiveness. Large-scale storage projects truly test system integration, engineering iteration, project delivery, fault response, software control, grid-connection capability, and cross-regional service networks. If Chinese storage companies can only make hardware cheaper, it will be difficult for them to establish a durable position in large projects in the Middle East, Europe, Australia, Latin America, and Africa.

The rapid rise of Sungrow’s storage business shows that Chinese new-energy companies have entered a more complex stage of competition. They are no longer simply exporting manufacturing capability to the world. They are packaging and exporting engineering capability, system capability, and project-delivery capability.

3.Behind the Middle East Orders Is a Chinese Solution for Global South Energy Transition

The Middle East has special significance for Sungrow. Saudi Arabia and the UAE are both promoting energy-structure transformation. On one hand, they continue to rely on oil and gas revenue; on the other, they are accelerating the construction of large-scale renewable-energy projects, storage projects, and green industrial systems. The Middle East does not lack capital. What it lacks are system suppliers that can build large-scale renewable-energy projects under extreme conditions, connect them to the grid, keep them running reliably, and create long-term economic value.

Last year, Sungrow signed a 7.8GWh energy-storage project agreement with Saudi Arabia’s ALGIHAZ. Reuters reported at the time that the project would be used to improve the stability and reliability of Saudi Arabia’s power grid and support Saudi Vision 2030. The UAE Masdar 7.5GWh project in May further places Sungrow at the center of clean-energy infrastructure construction in the Middle East.

Chinese companies are rapidly entering the Global South’s energy transition as system suppliers. In the Middle East, Africa, Latin America, and Southeast Asia, electricity demand is growing, renewable resources are abundant, grid infrastructure is relatively weak, and new electricity-use scenarios are expanding quickly. Simply selling solar modules can no longer meet the next-stage needs of these markets. They need a combined solution made up of solar, storage, inverters, grid-connection control, operation and maintenance, local construction, and financing arrangements.

This is also the difference between Sungrow and traditional module companies. Module companies face increasingly intense price competition, trade barriers, and capacity cycles. Inverter and storage-system companies face a different type of competition: products must be reliable, systems must be stable, service must keep up, software and control algorithms must adapt to different grids, overseas projects must be delivered, and customers must believe the supplier can continue providing service for the next ten years or longer.

According to Time Weekly’s reporting on China’s solar exports, in 2025, 70 A-share listed photovoltaic equipment companies generated RMB 341.255 billion in overseas revenue, down slightly by 2.12% year on year. But inverters, materials, and auxiliary equipment grew against the trend. Sungrow ranked first among listed photovoltaic companies in overseas revenue, with RMB 53.992 billion.

This shows that the structure of China’s solar globalization is changing. In the past, the most visible part was module exports. In the next stage, the more valuable export links are increasingly concentrated in inverters, energy-storage systems, power electronics, smart operation and maintenance, and solar-storage integrated solutions. The global competitiveness of China’s new-energy industry is upgrading from “selling cheap products” to “delivering complex systems.”

4.Sungrow Has Cash, Yet Still Wants a Hong Kong Listing. Globalization Is Becoming Heavier.

Recently, Sungrow submitted its application to the Hong Kong Stock Exchange again. On the surface, Sungrow does not appear to lack money. Startup Frontier and several financial media outlets have noted that the company has ample cash on its balance sheet, yet still plans to raise funds in Hong Kong and use the proceeds for overseas production bases, research and development, and global expansion.

Beijing Business Today, The Beijing News, and other media outlets have reported that Sungrow plans to use the proceeds from its Hong Kong IPO for two overseas bases in Poland and Egypt. The Polish base is planned to include production capacity for energy-storage systems and inverters, while the Egyptian base is planned for energy-storage system capacity. The Beijing News reported that the Polish base is expected to have about 22.5GWh of energy-storage system capacity and 20GW of inverter capacity, while the Egyptian base is expected to have 10GWh of energy-storage system capacity.

This is a capital-structure adjustment after Chinese new-energy companies have entered the second stage of globalization. In the past, Chinese manufacturing companies mainly relied on domestic production capacity, overseas sales networks, and trade channels to go global. Now, trade barriers, rules of origin, localization requirements, public-procurement policies, geopolitical risk, and customer supply-chain security requirements are all rising. To continue serving Europe, the Middle East, Africa, and other overseas markets, companies must build overseas production capacity, overseas service networks, local delivery capability, and more complex financing arrangements.

In April, STAR Market Daily also reported on the overseas factory-building wave among Chinese energy-storage companies. It noted that Chinese storage companies have accelerated the establishment of overseas manufacturing bases this year. Sungrow is investing in its first manufacturing plant in Europe, with planned annual capacity of 20GW of photovoltaic inverters and 12.5GWh of energy-storage systems. At the same time, Sungrow is also working with the Egyptian government and Norwegian renewable-energy company Scatec on related projects in the Suez Canal Economic Zone.

This is exactly the major change in China’s new-energy globalization model. Companies are no longer simply selling products made in Chinese factories to overseas markets. They are embedding part of their manufacturing, delivery, service, and supply-chain capabilities into overseas markets. For companies, this means higher capital expenditure, longer project cycles, more complex inventory and receivables management, and higher organizational requirements.

Energy Circle and Startup Frontier have both paid attention to the financial pressure behind Sungrow’s rapid expansion. Energy Circle noted that the company’s accounts receivable and inventory together exceed RMB 52 billion, and argued that the purpose of the Hong Kong listing looks more like providing support for overseas factories, international identity, and capital-market tools. Startup Frontier discussed the pressure behind Sungrow’s high-growth storage business from the perspectives of first-quarter revenue, profit decline, and storage gross-margin fluctuations.

This pressure does not mean the company’s strategy has failed. On the contrary, it shows that globalization has moved from a light-asset sales stage into a heavy-asset organizational stage. Overseas factories, local service, large-project delivery, and storage-system integration will make an equipment company increasingly resemble an infrastructure company. Revenue becomes larger, orders become larger, projects become more complex, and the balance sheet becomes heavier.

5.AIDC Power Brings Sungrow Into the AI Infrastructure Cycle

Another interesting signal in recent coverage of Sungrow is its AIDC power business. AIDC stands for AI Data Center. As demand for large-model training and inference rises, AI data centers impose higher requirements on power systems than traditional data centers. Power density is higher, electricity load is greater, continuity of supply is more critical, and power quality, voltage levels, conversion efficiency, cooling, and backup power systems all become more important.

In its report on the “three paths of computing-power storage,” Xinliu Think Tank compared Sungrow with Kstar, Shuangdeng, and other companies, discussing different routes for AIDC storage and power systems. The report argued that Sungrow entered the AIDC race relatively late, but has strong capital and technical reserves. Its experience with 1500V platforms, 800V direct-current adaptation, nearly ten years of preliminary research into 35kV solid-state transformers, and its capabilities in storage converters and solar-storage systems all provide entry points. The report also noted that Sungrow has been relatively cautious in how it describes the AIDC business, aiming to achieve product landing and small-scale delivery in 2026.

Today, global AI competition is increasingly constrained by power infrastructure. Data centers need stable electricity, low-loss power supply, backup power, energy-storage systems, thermal management, and grid dispatch. In regions where AI data centers are being built in clusters, compute growth quickly becomes a power-system problem.

Sungrow’s entry into AIDC is not a random attempt to chase a hot theme. Its underlying capability comes from power electronics. Inverters, storage converters, HVDC, solid-state transformers, grid-forming storage, and solar-storage integrated systems are all fundamentally about power conversion, control, and management. AI data-center power systems need exactly this kind of capability. The difference is that AIDC imposes higher requirements for reliability, response speed, power density, and system redundancy.

China’s AI competition is often understood externally as a competition over chips and models. But over a longer time horizon, AI infrastructure competition will increasingly resemble energy-system competition. Whoever can build cheaper, more stable, and more scalable power and data-center infrastructure will be able to support broader AI application diffusion. Sungrow’s entry into AIDC power shows that Chinese new-energy equipment companies are penetrating the AI infrastructure chain.

This is also why China Industry Signals should continue to track these developments. Chinese industry media often capture changes in corporate boundaries earlier than overseas media. External narratives see “solar companies,” “storage companies,” or “inverter companies.” Chinese industry media see that these companies are entering new growth curves along the technological common ground connecting power electronics, storage, grids, data centers, and new energy infrastructure.

6.China’s Solar Globalization Is Moving From the Module Era to the Energy-System Era

Over the past decade, overseas understanding of China’s solar industry has mainly centered on several words: capacity, price, subsidies, overcapacity, and trade frictions. These words are not entirely wrong, but they are no longer enough to explain today’s industrial changes.

The first thing that shocked global markets about China’s solar industry was the fall in module prices and the expansion of manufacturing scale. Polysilicon, wafers, cells, and module capacity expanded rapidly, dramatically lowering the global cost of solar power generation while also creating fierce price wars and trade disputes. Much of the discussion in Europe and the United States still remains at this level, interpreting China’s new-energy competitiveness as “low-price impact.”

Sungrow does not represent this layer. Its position is closer to the control layer, storage layer, and grid-connection layer of photovoltaic power-generation systems. As renewable energy’s share increases, global markets need more than cheap modules. They need system solutions that can address intermittency, volatility, grid stability, and project economics. Storage, inverters, PCS, EMS, grid-forming control, and long-term operation and maintenance are becoming more important.

This is why Sungrow’s story has broader significance for the global competitive landscape. It shows that Chinese new-energy companies are moving from manufacturing-scale advantage to complex-system delivery advantage. In the module era, the core competition was scale, cost, efficiency, and supply chains. In the energy-system era, the core competition also includes grid understanding, scenario adaptation, software control, safety management, overseas localization, and lifecycle service.

This change is consistent with the broader direction of China’s manufacturing upgrade. Many Chinese companies are moving from selling individual products to selling systems, from exporting products to exporting solutions, and from being low-cost suppliers to becoming global engineering and infrastructure partners. Energy storage, electric vehicles, power batteries, smart grids, charging networks, industrial robots, drones, and construction machinery are all going through similar changes.

7.The Risks Are Also Clear: High Growth in Storage Comes at a Cost

Chinese media reports over the past month have also discussed the risks behind the rapid expansion of the energy-storage industry.

First, competition in the storage industry is intensifying. Startup Frontier noted that Sungrow’s revenue and net profit attributable to shareholders declined year on year in the first quarter of 2026, and discussed the downward pressure on storage gross margins. Although storage systems are growing quickly, more battery companies, PCS companies, system integrators, and cross-sector entrants are entering the market. Price competition and project competition will continue to intensify.

Second, low-price competition in China’s domestic storage market is severe. Sungrow said in an investor survey that domestic storage shipments declined because the company strategically gave up some projects. Its domestic business gross margin was only in the single digits and was loss-making. This shows that the company is not enjoying smooth growth in every market. High growth in overseas markets is important for Sungrow, but it also means the company’s dependence on overseas demand, exchange rates, trade policy, and major customer orders is rising.

Third, overseas factory construction and localization will raise organizational complexity. If the Poland and Egypt bases are put into operation on schedule, they will strengthen Sungrow’s global supply capability. But overseas manufacturing is not a simple replication of Chinese factories. Local labor, supply chains, policy approvals, logistics, quality control, management culture, taxation, and geopolitical risks may all affect project progress and returns.

Fourth, accounts receivable and inventory pressure need continued monitoring. Large-scale storage projects involve high contract values, long delivery cycles, and relatively concentrated customers, which can easily create working-capital pressure. Energy Circle’s report asking why Sungrow is rushing to list despite making money approached the issue exactly from the angles of cash, receivables, inventory, and overseas expansion pressure.

Fifth, AIDC power is still in the validation stage. The market potential for AI data-center power is large, but technical routes, customer certification, delivery pace, and competitive structure remain unclear. Sungrow has technological commonality with this field, but that does not mean it can quickly replicate the success of its storage business. AIDC customers have very high requirements for reliability, certification cycles, and system responsibility, and leading international customers already have mature supply-chain systems.

These risks do not weaken Sungrow’s value as an industrial signal. On the contrary, they make the company more worth watching. Truly important industrial changes are usually not linear expansions. They come with higher capital intensity, more complex organization, higher technical thresholds, and greater risk exposure.

8.Sungrow Reveals the Next Stage of China’s New-Energy Globalization

Overall, Sungrow represents a structural upgrade in China’s new-energy globalization.

In the first stage, Chinese new-energy companies mainly exported low-cost products to the world. Modules, batteries, inverters, electric vehicles, power batteries, and engineering equipment all went through this stage. The core capabilities in this stage were manufacturing scale, supply-chain efficiency, cost control, and rapid iteration.

In the second stage, Chinese companies began exporting systems. Solar is no longer just modules. Storage is no longer just battery cabinets. Electric vehicles are no longer just cars. AI is no longer just models and chips. Energy is no longer just power-generation equipment. Companies need to integrate hardware, software, engineering, operation and maintenance, financing, local delivery, and policy adaptation.

Sungrow is at the frontier of this second stage. It has moved from photovoltaic inverters into energy-storage systems, from the Chinese market into the Middle East, Europe, and the Global South, from equipment sales into large-scale energy-project delivery, and from clean energy into AI data-center power systems. Its expansion demonstrates an important capability of China’s industrial system: the ability to combine long-accumulated manufacturing capability, power-electronics capability, engineering capability, and global project experience into new infrastructure solutions.

Overseas media often place Chinese new-energy companies into two narratives: “overcapacity” and “low-price dumping.” Both narratives capture part of the facts, but they miss the more important industrial evolution. Chinese companies do have scale, and competition is indeed intense. But scale and competition are forcing leading companies to upgrade toward more complex, higher-value, and more systemized directions.

Sungrow’s case shows that Chinese clean-energy companies are moving from the manufacturing end of global supply chains toward the organizational end of global energy infrastructure. They are changing not only product prices, but also project-delivery methods, energy-system structures, and the infrastructure-development pathways of the Global South.

This is the most important industrial signal from Sungrow: a photovoltaic inverter company that grew out of Hefei is now entering the intersection of energy storage, overseas manufacturing, Middle East energy engineering, and AI data-center power systems. This intersection is one of the most important front lines of the next stage of global energy competition and industrial competition.

Source Note: This essay is based on recent Chinese media reporting and public corporate information, including reports from The Paper and financial-media reposts on the Masdar 7.5GWh project; Startup Frontier and TMTPost reports on Sungrow’s Hong Kong fundraising plan, energy-storage business, and AIDC power layout; The Beijing News reports on Sungrow’s Hong Kong IPO and overseas base planning; Anhui Daily reports on Sungrow’s second Hong Kong Stock Exchange filing and Anhui’s solar-storage industrial cluster; STAR Market Daily reports on the overseas factory-building wave among Chinese energy-storage companies; and Sungrow’s official website and 2025 annual-report disclosures.