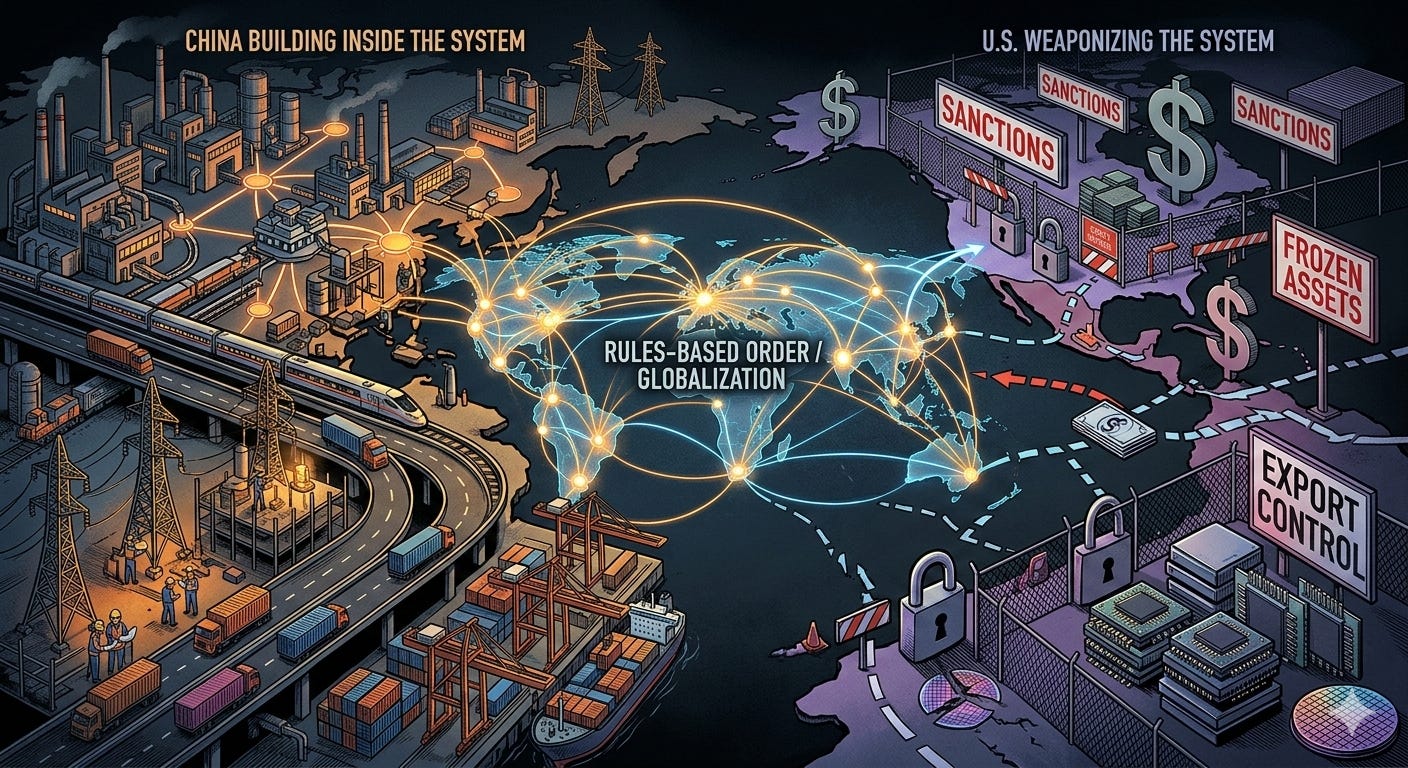

The Rules-Based Order Was Not Captured by China. It Was Weaponized by the United States

Rethinking the China Debate #4: China did not hijack the system. It outperformed within it.

For years, one of the most comforting myths in Western discourse has been that the so-called rules-based order was not weakened by its own contradictions, and not discredited by the conduct of the powers that claimed to defend it, but quietly captured from within by China. Amanda van Dyke’s post The Rules-Based Order Did Not Fail. It Was Captured., is one of the clearest recent expressions of this argument.

In this telling, Beijing entered the system, benefited from its openness, accumulated industrial and financial power, and then gradually bent the system against its original architects.

This story is politically convenient. It is also analytically wrong.

China did not capture the rules-based order. China succeeded inside it. What truly damaged the order was not China’s rise, but the steady American transformation of trade rules, payment systems, reserve assets, technology access, and supply chains from broadly usable infrastructure into instruments of pressure, exclusion, and control. The real rupture came when the core operating systems of globalization stopped being experienced as neutral channels and started being experienced as geopolitical leverage.

That distinction matters because once it is confronted, the comforting myth collapses. If China’s rise was mainly the result of superior performance inside the system, then the central Western failure was not victimhood but complacency. And if the deeper reason the order is losing legitimacy is that the United States increasingly weaponized the very infrastructure on which globalization depended, then the crisis of the order is not primarily about Chinese manipulation. It is about the West discrediting its own system by making access to it conditional, selective, and openly coercive.

I. Success Inside a System Is Not the Same as Capturing It

The first failure of the “capture” thesis is conceptual: extraordinary success inside a system is not evidence of control over that system. It is evidence of competitiveness.

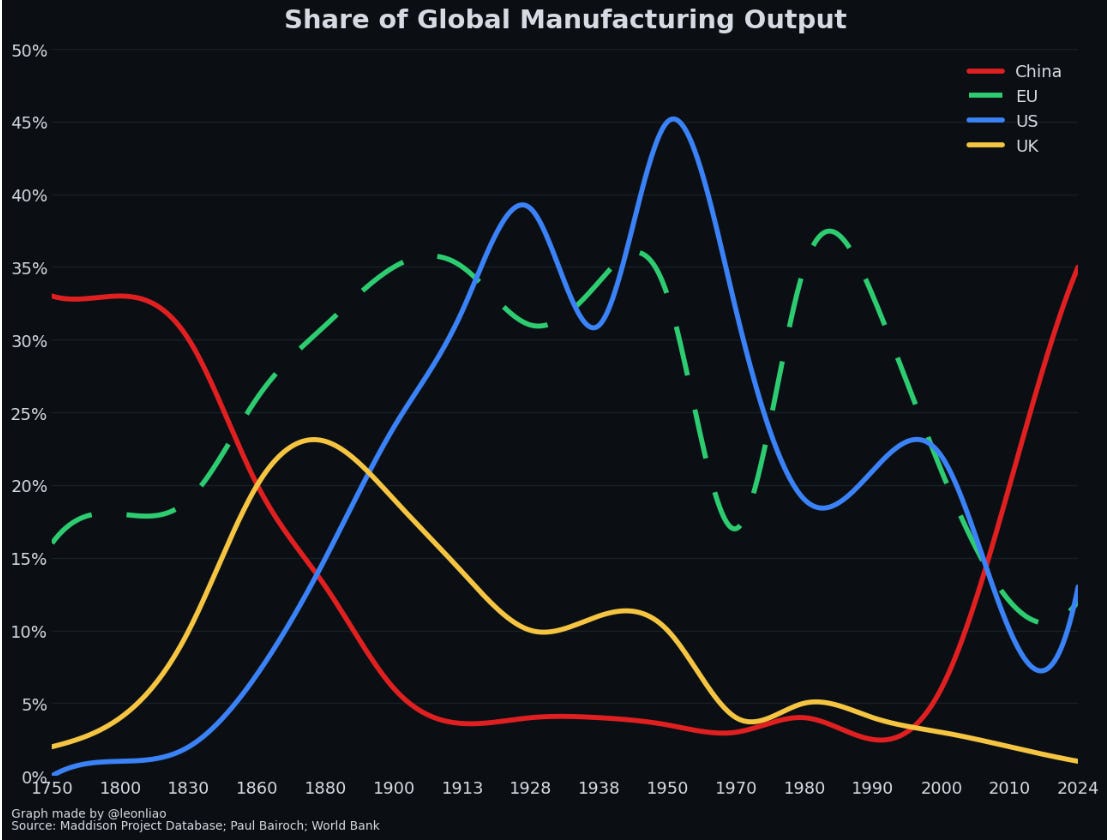

China was unquestionably one of the greatest beneficiaries of globalization over the past two decades. Its share of global manufacturing output is now around 35%, a level not seen for roughly 200 years. That is an extraordinary fact. But extraordinary success inside a system is not the same thing as institutional capture of that system. It means that China became exceptionally good at operating under the incentives that system actually created.

An open global economic order naturally pushes capital, manufacturing capacity, supply-chain nodes, and technological diffusion toward locations that offer higher efficiency, lower costs, larger scale, stronger organizational capacity, and denser industrial ecosystems. If China performed better than most countries under these rules, the logical conclusion is not that China “captured” the system. The logical conclusion is that China became more competitive within it.

This is precisely where much Western commentary still refuses to be honest. It often blurs two very different claims: first, that the United States designed much of the modern globalization framework; and second, that the United States should therefore remain its permanent primary beneficiary. But international economic systems have never distributed rewards according to moral authorship. They distribute industrial positions according to competitiveness. The globalization framework built largely under U.S. leadership encouraged cross-border capital mobility, production specialization, supply-chain expansion, cost optimization, and large-scale industrial organization. As long as those mechanisms remained active, manufacturing was always going to gravitate toward regions able to sustain lower coordination costs and denser industrial ecosystems.

From this perspective, China’s rise does not represent an abnormal “hijacking” of the rules. It represents the outcome produced when those rules operated according to their own internal logic. The real issue is not that China secretly rewrote the system. It is that the architects of globalization badly underestimated how effectively another large state could organize industry, infrastructure, and national capacity within that system.

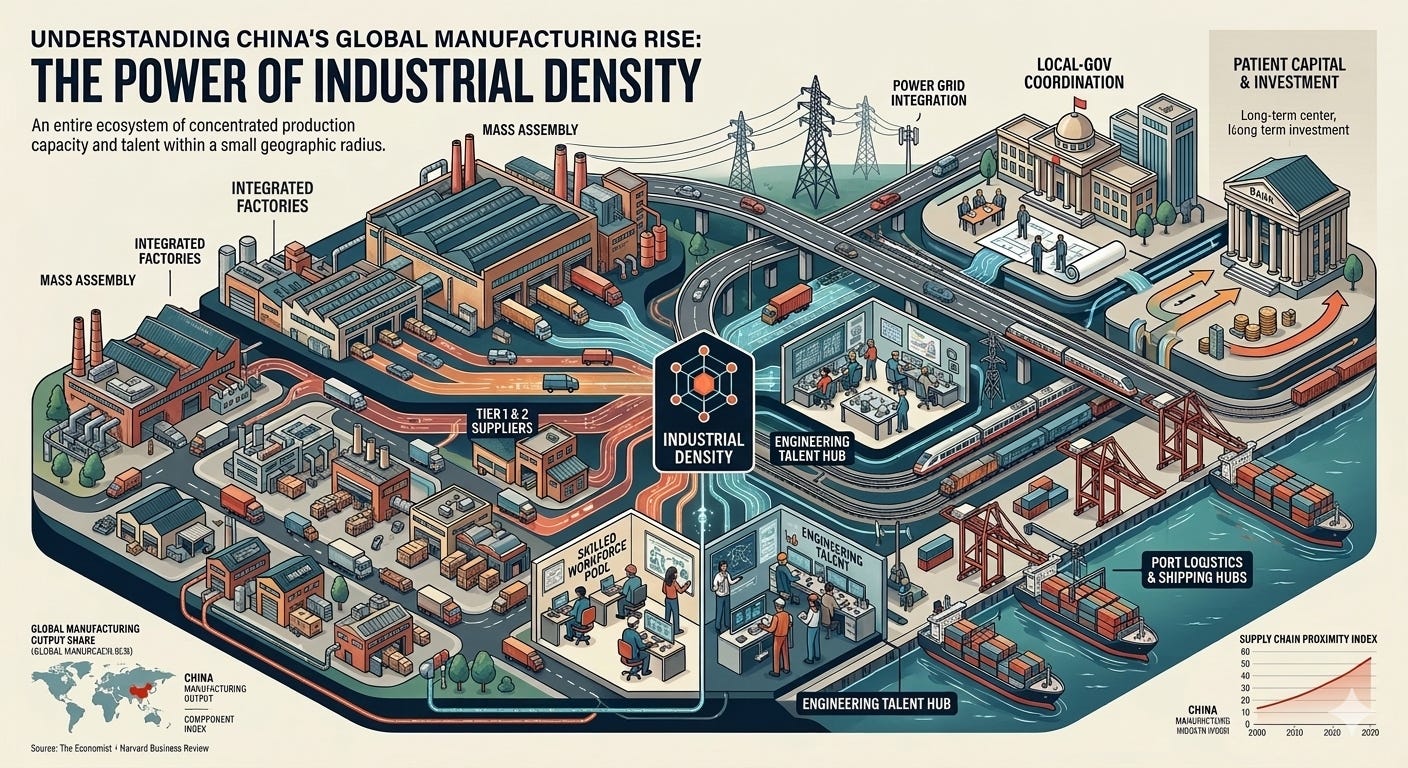

II. China’s Rise Was Built on Industrial Density, Not Institutional Hijacking

If one wants to understand why China rose, the key lies not in conspiracy narratives, but in industrial reality.

China’s advantage in global manufacturing begins, above all, with industrial density. This is not an abstract phrase. It refers to an entire ecosystem of highly concentrated production capacity, component suppliers, skilled workers, engineering talent, infrastructure, port logistics, local-government coordination, and patient capital, all compressed within an extremely small geographic radius. This is the part that much Western commentary keeps moralizing around because the alternative is too uncomfortable: China did not rise because it captured institutions. It rose because it built an industrial ecosystem that was denser, faster, and harder to replicate than almost anyone else’s.

What truly supported China’s rise was a city-cluster-level manufacturing network: a system in which a single factory can be surrounded by hundreds or even thousands of supporting firms; in which raw materials, molds, machine processing, electronic components, final assembly, and testing can be iterated in very short timeframes; and in which alternative suppliers can be found in days rather than months when disruptions occur. It is also the composite result of highways, deep-water ports, rail freight, grid stability, vocational education systems, local investment-promotion capacity, and coordinated industrial policy. This is why, under the same WTO rules and facing the same global capital flows, many countries obtained only partial assembly functions, while China expanded into entire industrial chains.

In other words, China’s rise was primarily the victory of industrial organization, not the product of institutional hijacking. And there is a major analytical problem with reducing this outcome to “institutional hijacking”: it allows the West to avoid confronting the real reasons for its own industrial hollowing-out. Manufacturing capacity is not preserved simply by writing a few trade rules, and supply-chain density cannot be recreated through declarations of values. China developed advantages in steel, chemicals, solar, batteries, consumer electronics, machinery, and a growing range of mid- to high-end manufacturing above all because it treated industrial capacity as a core variable of national competitiveness over a long period of time. Much of the Western world, by contrast, assumed for too long that financial superiority, technological superiority, and institutional superiority could substitute for manufacturing density.

Only now is it becoming obvious how dangerous that assumption was. Once industrial networks are thinned out, many capabilities cannot be rebuilt with a few years of subsidies, a flagship factory announcement, or a reindustrialization speech. To describe this outcome as “China capturing the system” is to bury the real industrial lesson under a moralized narrative.

III. Transactional Networks Are Not a Coherent Alternative Order

The second major failure of the “capture” thesis is that it takes a set of transactional relationships and inflates them into a coherent alternative world order that does not yet exist.

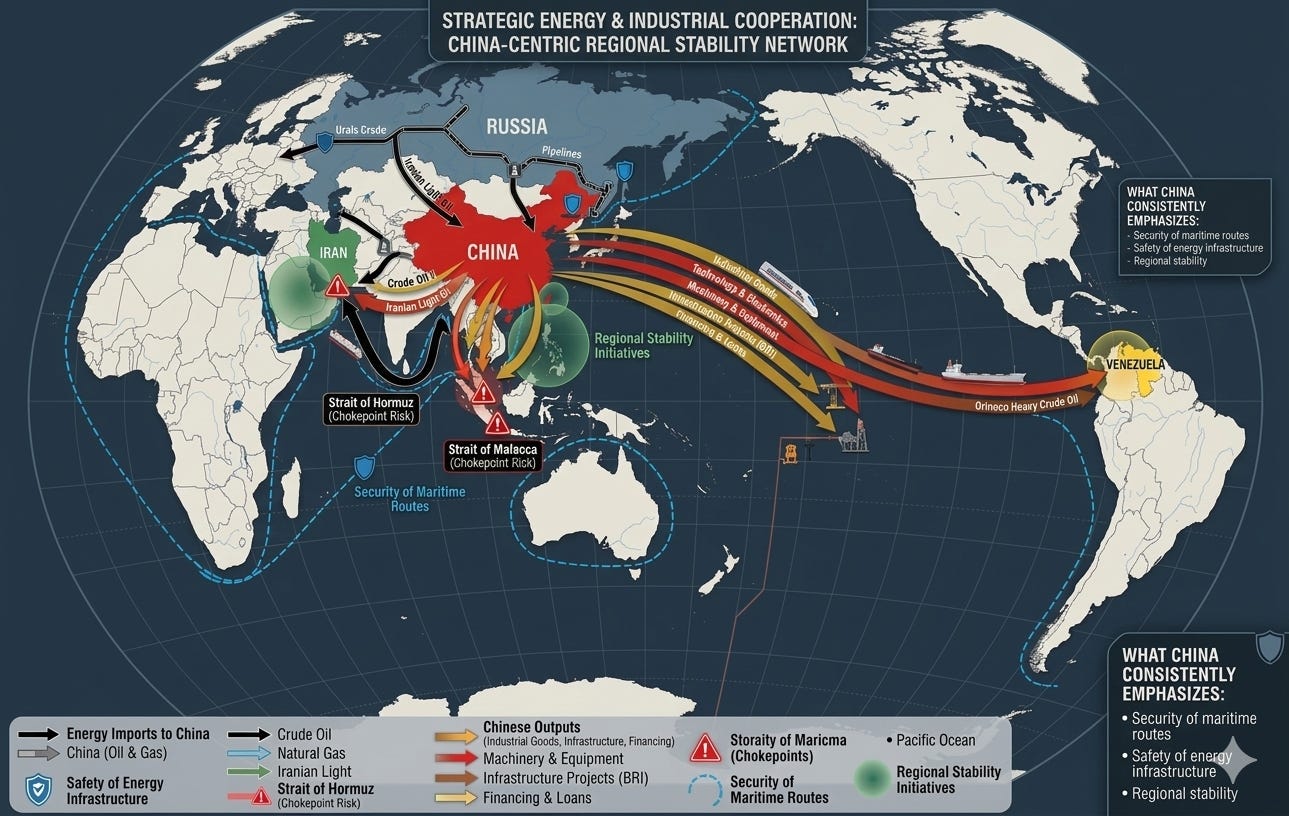

Articles arguing that the system has been “captured by China” often make a second logical leap: they portray cooperation among China, Russia, Iran, and Venezuela as though it were a highly coordinated alliance constructing a new global order. The claim sounds dramatic. Its evidentiary chain is thin. China certainly has multi-layered relationships with these countries in energy, trade, settlement mechanisms, and diplomatic support. But these relationships are mostly transactional, hedging-oriented, and situation-specific, rather than components of an integrated alliance built around a shared institutional blueprint, common governance architecture, and collective strategic discipline.

When China purchases energy from Russia and Iran, the most basic logic is security of supply and price advantage. Russia and Iran need export markets; China needs resource inflows. Their deeper trade ties under sanctions show, first and foremost, that markets and sanctions together have reshaped commercial flows. They do not demonstrate that China is actively constructing a unified alternative order. China’s relationship with Venezuela is even more clearly a complex transaction involving resources, debt, political risk, and geopolitical presence, not some endlessly scalable alliance model. What China has consistently emphasized in the Middle East is the security of maritime routes, the safety of energy infrastructure, and regional stability, because for one of the world’s largest energy importers, disorder in the Middle East means higher costs, inflation, and supply risk, not some effortless geopolitical windfall.

More importantly, any system that could truly replace the existing international order would require a clear institutional center, a stable financial anchor, a scalable legal framework, widely accepted payment infrastructure, and large-scale transnational trust networks. China, Russia, Iran, and Venezuela quite obviously do not meet these conditions today. What they possess are connected commercial channels and diplomatic coordination forums, not a fully formed global institutional architecture. To portray opportunistic cooperation as a replacement order may generate alarm. It does not improve analysis.

IV. The Real Turning Point Was the Weaponization of the System

If the rules-based order has genuinely entered crisis, the turning point did not come when China became stronger. It came when the system’s underlying infrastructure ceased to be broadly experienced as neutral.

Before 2008, globalization was defined by expansion. The share of global merchandise exports in world GDP rose from roughly 7–8% in the late 1940s to about 25% by 2008. That enormous increase reflected decades of trade liberalization, supply-chain fragmentation, containerized shipping, and the integration of large manufacturing economies such as China into the global system. After 2008, globalization entered a different phase. The financial crisis marked a structural turning point: trade intensity stopped rising steadily and began fluctuating under growing geopolitical and policy pressures. Although the ratio briefly surged again to around 26% in 2021 during the post-pandemic trade rebound, the broader trend since 2008 has been one of slower expansion, greater volatility, and increasing political intervention in global supply chains. Globalization did not disappear. It became more selective, more defensive, and more openly shaped by geopolitical risk.

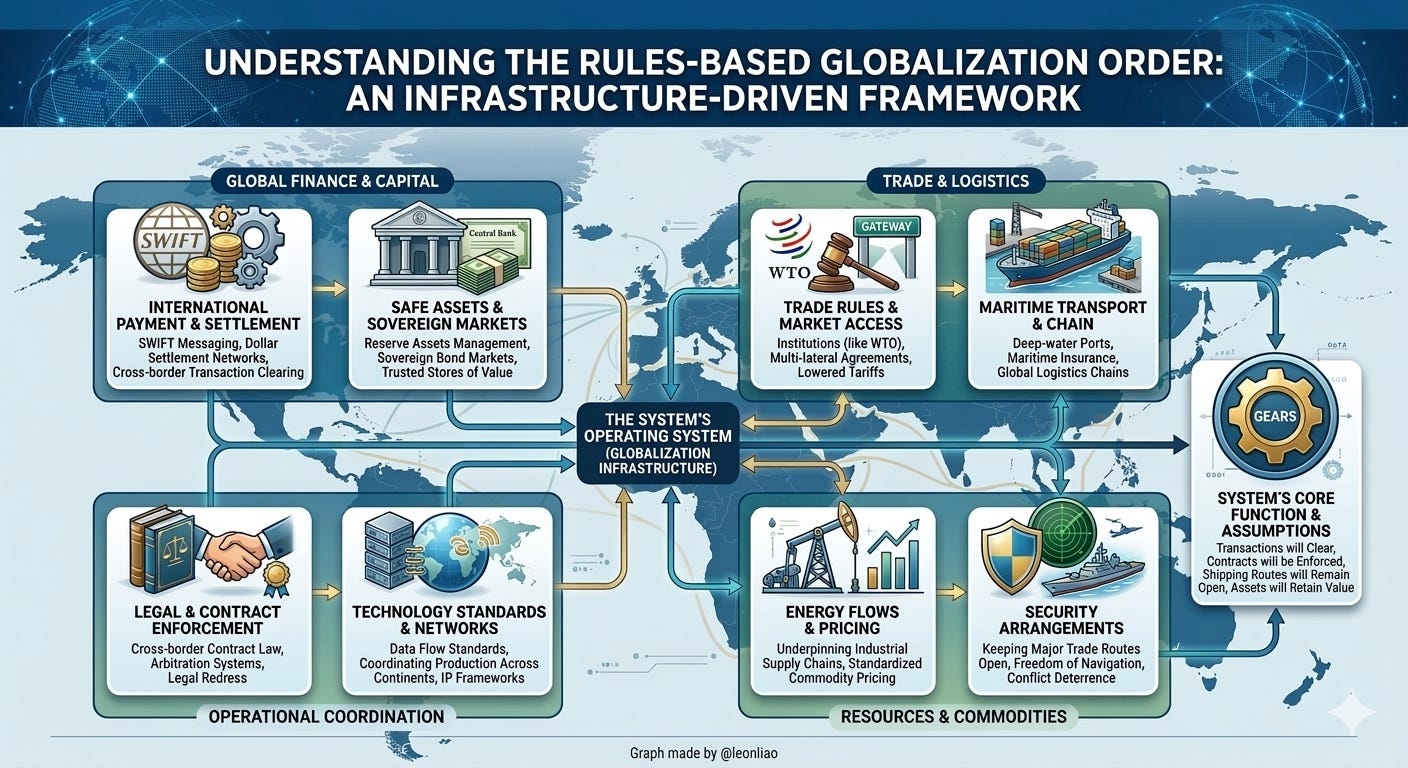

To understand why the weaponization of the system matters, one must first recall what the rules-based globalization order actually consisted of. It was never just diplomatic norms or multilateral declarations. It rested on a dense and highly practical infrastructure that allowed global trade and finance to function at scale. This infrastructure included international payment and clearing systems such as SWIFT and dollar settlement networks; reserve assets and sovereign bond markets that provided safe stores of value; trade rules and market-access frameworks built around institutions like the WTO; container shipping routes, deep-water ports, maritime insurance, and global logistics chains; legal systems capable of enforcing cross-border contracts and arbitration; technology standards and data networks that allowed firms to coordinate production across continents; energy flows and commodity pricing systems that underpinned industrial supply chains; and, in the background, security arrangements that kept major trade routes open. Together these elements formed the operating system of globalization. They made it possible for companies, banks, and governments across the world to assume that transactions would clear, contracts would be enforceable, shipping routes would remain open, and assets would retain value.

That system was never morally neutral. But for a long time it was operationally usable. And usability, not moral rhetoric, is what keeps an order standing. International order is not sustained because all countries believe in abstract principle. It is sustained because most countries assume that payments, reserves, settlement mechanisms, trade access, and technological exchange, although led by great powers, remain broadly predictable most of the time. As long as application remains generally stable, smaller and middle powers are willing to accept asymmetry within the system because they can still pursue growth and security inside it.

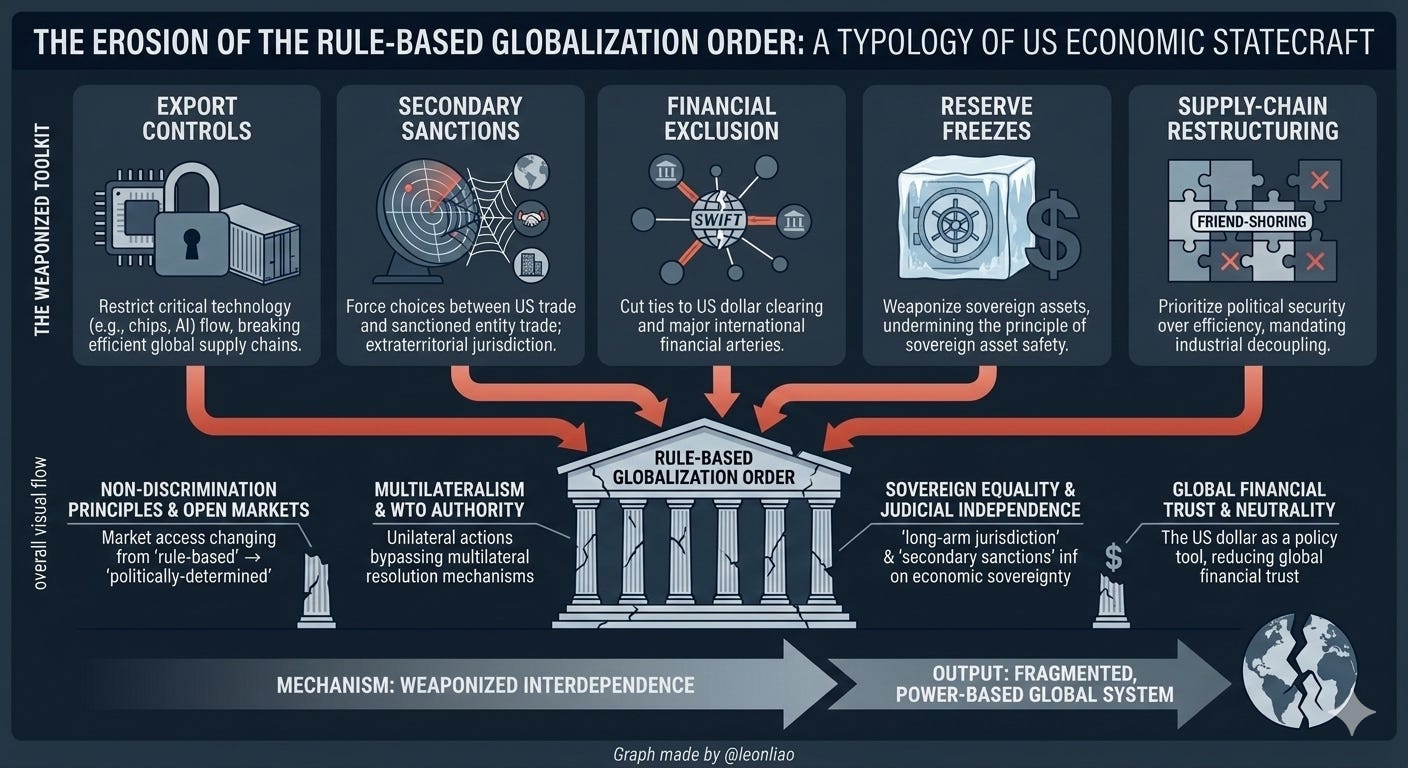

What changed this was the increasingly systematic way in which the United States transformed that infrastructure into an instrument of power over the past decade. When dollar clearing no longer functions merely as a channel for global trade, but as leverage that can be activated at any time; when sanctions cease to be exceptional tools and instead become a normal and frequently used policy instrument; when export controls, secondary sanctions, financial exclusion, reserve freezes, and supply-chain restructuring begin to appear together, then the nature of the international order itself changes. It ceases to be simply an open platform clothed in rules and increasingly begins to resemble a hierarchical structure led by the United States, with access conditions adjustable in line with American strategic objectives.

This is the real analytical entry point for understanding today’s crisis of order. Countries were not suddenly persuaded by China to resist a Western-led system. What changed their risk calculations was the gradual realization that the global economic infrastructure that once appeared neutral was not fully neutral at all. Once key nodes in the system can be politically instrumentalized, any country deeply embedded in that system will begin to think about precautionary measures. Once that neutrality disappeared, the system did not collapse overnight. But it began to behave very differently.

V. Dollar Power, Sanctions, and the End of Neutral Infrastructure

Over the past decade, the United States has not merely imposed sanctions or tightened export controls in isolated cases. It has progressively politicized the core infrastructure of globalization itself.

The damage has unfolded layer by layer. First, through the erosion of predictable trade rules, as tariffs, national-security exceptions, and unilateral restrictions increasingly displaced multilateral discipline. Second, through the narrowing of technology diffusion and industrial upgrading, as export controls, entity lists, and licensing regimes turned open commercial networks into stratified systems of access. Third, through the restriction of capital allocation, as outbound investment, industrial cooperation, and cross-border production decisions became subject to national-security logic. Fourth, through the loss of neutrality in payment and clearing systems, as dollar channels, sanctions, and compliance rules were used as instruments of pressure. Fifth, through the politicization of reserve and safe assets, as freezes and financial exclusion weakened confidence in their neutrality. And finally, through the restructuring of global supply chains themselves, as efficiency gave way to friend-shoring, de-risking, and politically defined trust boundaries.

Taken together, these shifts amount to something much larger than a series of tactical measures. They represent a structural redefinition of the global system’s most important operating channels — trade rules, technology flows, capital allocation, payment networks, reserve assets, and supply-chain organization — from relatively neutral infrastructure into instruments increasingly conditioned by strategic and political approval. The deeper damage, therefore, is not limited to any single targeted country. It falls on the neutrality, universality, and predictability of the rules-based globalization order itself.

The central role of the U.S. dollar was once one of America’s most important forms of global public power because it simultaneously provided liquidity, safe assets, pricing benchmarks, and payment convenience. Precisely because the dollar system was deep, broad, and stable, global trade and reserve holdings were willing to organize around it. But when a monetary system becomes increasingly tied to geopolitical punishment, it gradually transforms from public infrastructure into a strategic weapon. What dollar weaponization changes is not merely the position of sanctioned states. It changes the psychological expectations of all observing countries toward the system as a whole.

The consequences of sanctions overuse are similar. Sanctions have always existed. But when their scope expands continuously, when the spillover effects of secondary sanctions grow stronger, and when multinational firms and third-country financial institutions are compelled to reconfigure their behavior around U.S. policy, sanctions cease to be merely a diplomatic tool. They become an institutional force for restructuring global commercial networks. Reserve freezes further break an even deeper assumption: that high-grade foreign reserve assets held by sovereign states are, in most circumstances, relatively secure and politically neutral. Once that belief is broken, countries across the Global South, along with many middle powers, will naturally begin to reassess their own reserve structures, payment arrangements, and trade-finance dependencies.

The politicization of technology and supply-chain rules has accelerated this process even further. One of globalization’s basic promises was that, to a significant degree, commercial efficiency could override geopolitical disagreement. Today, more and more companies and states are discovering that access to technology, equipment purchases, chip supply, financial services, and even maritime insurance can be directly affected by great-power rivalry. When the “pipes” of globalization increasingly resemble strategic choke points, the credibility of the order begins to decline. The rules have not disappeared on paper, but in practice they rest on an increasingly fragile foundation of neutrality.

VI. Why the Rest of the World Started Building Alternatives

What much of the West describes as anti-system conspiracy is, in reality, a broad and rational wave of risk management.

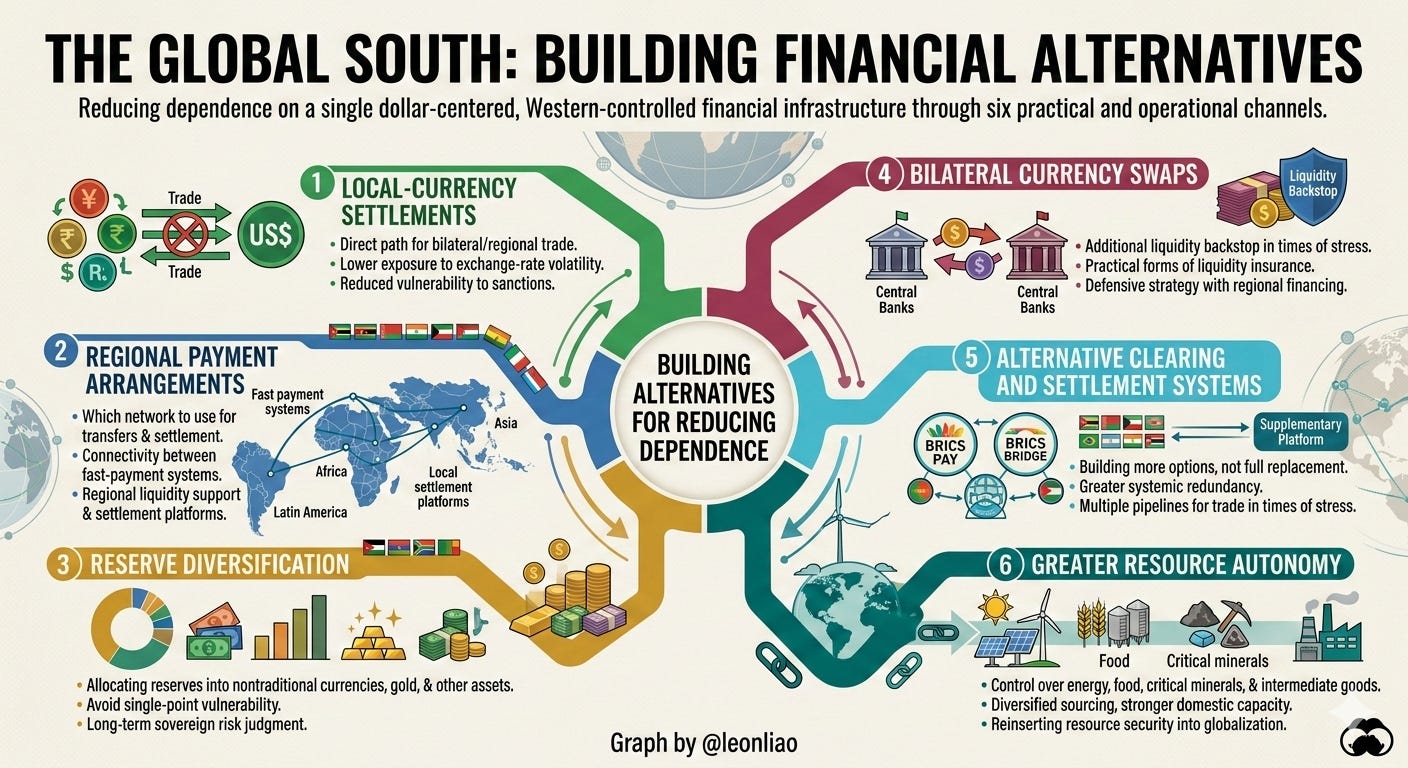

Against this backdrop, it is entirely natural that many countries have begun promoting local-currency settlements, regional payment arrangements, reserve diversification, bilateral currency swaps, alternative clearing systems, and greater resource autonomy. The Global South did not begin “building a new system” overnight. Rather, as the existing order became increasingly politicized, many countries started reducing dependence on a single dollar-centered, Western-controlled financial infrastructure through several practical and operational channels. Broadly speaking, these channels fall into six categories.

The first is local-currency settlement. This is the most direct and lowest-threshold path. The point is not to overthrow the dollar overnight, but to allow part of bilateral or regional trade to move, as much as possible, outside dollar pricing, dollar financing, and dollar clearing. The benefits are straightforward: lower exposure to exchange-rate volatility, less dependence on dollar liquidity, and reduced vulnerability to sanctions or payment disruptions. In recent years, more emerging economies have expanded the use of local currencies in trade involving energy, raw materials, and selected manufactured goods. At its core, this is transactional hedging, not ideological declaration.

The second is regional payment arrangements. If local-currency settlement answers the question of which currency to use, regional payment arrangements answer the question of which network to use. Many countries are not satisfied with merely switching currencies on paper, because if the underlying payment rails, correspondent banking networks, and clearing channels remain heavily dependent on Western infrastructure, the underlying risk has not really disappeared. As a result, more countries are pushing for regional payment connectivity, interoperability between fast-payment systems, regional liquidity-support mechanisms, and local settlement platforms. The logic is simple: reducing currency dependence is not enough if the transaction still has to travel through the same vulnerable pipes.

The third is reserve diversification. This step is especially important because it reflects longer-term sovereign risk judgments even more clearly than trade settlement does. Many countries are not “de-dollarizing” in the sense of abandoning the dollar altogether. But they are increasingly allocating new reserves into a broader mix of nontraditional reserve currencies, gold, and other liquid assets. The core logic is not replacement. It is avoidance of single-point vulnerability.

The fourth is bilateral currency swaps. Their significance lies in the fact that they provide countries with an additional liquidity backstop in times of stress, while also making local-currency trade and financing more realistic. Especially when dollar funding tightens, capital flows reverse, or external volatility rises, swap lines can reduce dependence on a single external source of liquidity. In this sense, bilateral swaps are not symbolic gestures. They are practical forms of liquidity insurance. Increasingly, emerging economies are using swap lines together with regional financing arrangements and reserve management as part of a layered defensive strategy.

The fifth is alternative clearing and settlement systems. This is the area most often exaggerated as proof that a full “parallel order” has already emerged. A more accurate interpretation is that many countries are trying to build more options, not immediately replicate a complete alternative to the SWIFT-dollar system. Arrangements such as BRICS Pay or BRICS Bridge are better understood as supplementary platforms for local-currency trade and cross-border settlement. They may not yet be capable of replacing the existing global financial network, but their real value lies elsewhere: they give countries more than one pipeline to rely on in moments of political or financial stress. The core purpose of alternative clearing systems is therefore not immediate replacement, but greater bargaining power and greater systemic redundancy.

The sixth is greater resource autonomy. This may not look like a payment issue at first glance, but in reality it is deeply connected to payment, settlement, and reserves. For many Global South countries, if energy, food, critical minerals, and intermediate goods remain heavily dependent on external systems, then strategic vulnerability persists even if financial alternatives are put in place. That is why many countries in recent years have pursued not only monetary and payment de-risking, but also more diversified energy sourcing, greater control over critical minerals, stronger domestic processing capacity, more regional supply-chain construction, and less reliance on a single transport or financing corridor. This is less an attempt to reverse globalization than an effort to reinsert resource security into globalization’s underlying design.

These initiatives do not necessarily arise from a shared ideology, nor do they imply that a fully developed alternative to the dollar system will emerge in the near term. But they reflect a rational effort to reduce vulnerability to a single financial architecture. In other words, de-dollarization and alternative payment mechanisms are first and foremost instruments of risk management, not declarations of revolution.

This point is especially important because many Western commentaries misinterpret developments precisely at this stage. Defensive adjustments are often framed as a coordinated anti-Western conspiracy, as though the world were collectively organizing under Chinese leadership to dismantle the existing order. A more realistic interpretation is far simpler: as the current system becomes increasingly selective and punitive, more countries are beginning to build contingency paths for worst-case scenarios. They may not believe that alternative systems are fully mature. But they are increasingly unwilling to anchor their entire economic future to a structure that can be weaponized at any time.

What are often described today as “parallel systems” are therefore better understood as responses to the erosion of credibility in the original system. They are symptoms and consequences, not the root cause. Without the weaponization of the dollar, the proliferation of sanctions, the politicization of financial infrastructure, and the strategic use of technological rules, these alternative arrangements would not possess the same momentum or appeal.

Conclusion: the order was not captured. It was discredited

China did not destroy the rules-based order. It operated successfully within it.

That may have been strategically uncomfortable for the West. It may have accelerated relative decline. It may have exposed Western complacency and industrial erosion. But none of that amounts to capture.

What truly damaged the order was something deeper and more consequential: the erosion of neutrality at its core. Once trade becomes selective, finance becomes conditional, reserves become political, technology access becomes restrictive, and supply chains become instruments of alignment, the system changes character.

It stops functioning as infrastructure. It starts functioning as leverage.

That is the real rupture.

An international order can survive asymmetry. It can survive hierarchy. It can even survive resentment. What it cannot easily survive is the widespread belief that its most important infrastructure no longer behaves like infrastructure, but like a weapon.

That is why the right conclusion is not that China captured the order. It is that the order discredited itself when the United States increasingly weaponized the very channels on which globalization depended.

When rules become weapons, the structure of order may remain standing for a while. But the trust that makes it durable has already begun to leave.