Why China Delivers Large Transformers for AIDC Faster Than the U.S. ?

Global Energy System #3

Why Has the U.S. Transformer Supply Suddenly Become So Tight?

The United States is trying to enter an AI-driven supercycle in power infrastructure, but the first thing it has exposed is not a shortage of compute. It is that the heavy industrial equipment system required to actually deliver electricity to load centers is not ready. In the past, the market was more accustomed to talking about GPUs, data centers, natural gas generation, nuclear restarts, and renewable expansion, as if the power constraint of the AI era would naturally ease as long as generation capacity increased. But the reality is that electricity does not become usable automatically the moment it is “produced.” It has to go through voltage step-up, transmission, step-down, grid connection, protection, dispatch, and end-user access before it can truly become a stable system capability that data centers, factories, and households can reliably draw on. And along that chain, large power transformers are precisely one of the most critical, and most easily overlooked, components.

The upgrading of the U.S. grid, the expansion of AI data centers, and the reshoring of manufacturing are now running into the same deeply “old industrial” hard constraint at once: an insufficient supply of large power transformers, combined with a clear shortfall in America’s own manufacturing capacity. This is no longer a vague supply-chain concern. It is already visible in delivery times. NERC noted that in 2024, large transformer lead times were running at roughly 80 to 210 weeks, with average transformer lead times around 120 weeks. At the same time, more than 80% of U.S. large power transformers are still imported. Once transformer deliveries are delayed, everything from data center interconnection and renewable integration to transmission upgrades and the commissioning of new industrial loads can be constrained in reverse by this piece of equipment that does not look especially “glamorous.” The market thought it was facing a compute bottleneck. In reality, the first thing getting stuck is the most basic layer of heavy grid equipment.

The problem is not simply that there is a shortage. The deeper problem is that this is an industry that is extremely difficult to scale up quickly. Large power transformers are not ordinary electrical appliances, nor are they standard industrial products whose output can be doubled quickly through a more standardized assembly line. They are often highly customized, have long manufacturing cycles, and require large numbers of skilled workers, grain-oriented electrical steel, copper, insulation materials, bushings, tap changers, coil manufacturing, high-voltage testing, and heavy transport and lifting capabilities. What U.S. media and industry sources have repeatedly emphasized over the past two years is exactly this kind of “slow industry” constraint. The issue is not that capital is unwilling to invest, nor that there is a lack of orders. It is that from raw materials, skilled labor training, production cadence, and quality testing to customer certification, the entire chain cannot catch up quickly in the way semiconductors or software sometimes can through sheer spending. Even if companies announce capacity expansion today, the new capacity often will not be meaningfully available until 2027 or 2028.

That is also why many people fall into the illusion that, since the world already has major players like Siemens Energy, Hitachi Energy, and Eaton, the market should not be this tight. The problem is that having many large companies does not mean having many companies that can fill the most critical supply gap in the short term. Siemens Energy and Hitachi Energy are more directly positioned in the hardest-to-expand layer: large main transformers and ultra-high-voltage equipment. Their order books, production schedules, certification processes, and high-end project delivery pipelines are inherently easier to lock up. Eaton, while also an important electrical giant, is more strongly positioned in distribution equipment, power quality, switchgear, medium-voltage equipment, and the broader data-center power chain. That does not mean it can immediately substitute for the shortage of large main transformers. In other words, what the market sees on the surface is that “there are many global giants.” But the number of firms that can actually fill the short-term gap in extra-large, high-voltage, long-lead-time core equipment is much smaller than it appears.

At a deeper level, this is no longer just an industry problem. It is a problem of national industrial organization capacity. In the past, many people understood great-power competition mainly as a competition at the technological frontier: whose chips are more advanced, whose models are stronger, whose data centers are larger, as if that alone would determine the next round of industrial advantage. But the reality is that the capabilities that truly support the expansion of frontier technologies are often the basic industrial goods least likely to make headlines and least likely to become the focus of market excitement. Large transformers are a textbook example. Without them, more GPUs, more natural-gas turbines, and more solar and wind installations do not necessarily translate into stable and usable power-system capability. Whether AI can ultimately become a real industrial and commercial force depends not only on algorithms and chips, but also on whether a country can produce, install, and maintain these “old industrial” devices as part of a coherent system.

Why Is China Better Able to Build a Systematic Supply of Large Power Transformers?

If one starts only from the level of individual firms, it is easy to reduce the question to “Chinese companies are stronger” or “American companies are not strong enough.” But the real difference is not mainly about isolated firm-level capability. It is that China has turned this category of equipment into a system-level industrial capability that can be expanded repeatedly, whereas the United States still operates more on a logic of “a project arrives, then resources are coordinated.” That is why once orders surge, the U.S. system is much more likely to get stuck on delivery.

The first and most fundamental difference lies in how demand is organized. China’s grid investment and long-distance transmission buildout are not the result of scattered market demand colliding on their own. They are organized over long periods through national-level planning and large state-owned power groups. For large transformers, GIS, converter valves, and ultra-high-voltage supporting equipment, what matters most is not whether orders suddenly spike in a single year, but whether there is a demand curve that is sustained, predictable, and repeatable over ten or more years. China’s grid system has long had several clearly defined structural priorities: cross-regional transmission, distribution-network upgrades, renewable integration, and industrial load expansion. Because of this, upstream equipment manufacturers can see the direction of demand several years in advance, and are therefore more willing to keep expanding factories, training skilled workers, building testing platforms, and laying out materials and component supply around relatively certain future demand. In other words, China is not merely chasing capacity whenever a boom appears. It has treated this category of equipment as a national foundational capability for a long time.

The second difference is that China has connected grid equipment, project construction, and grid operation into a relatively complete closed loop. Over the past many years, China has repeatedly built ultra-high-voltage lines, cross-regional transmission systems, and extra-high-voltage substations. In essence, it has been repeatedly executing the same category of large engineering projects at high frequency. The more repetition there is, the more unified standards become, the more mature the supply chain becomes, and the lower the coordination costs become across design, manufacturing, testing, transport, installation, and maintenance. In a slow industry like this, the most valuable thing is not a single isolated technological breakthrough. It is the engineering experience and organizational experience that emerge from repeated large-scale delivery. The U.S. problem is almost the reverse. Its large grid projects are more dispersed. Coordination among utilities, state-level approvals, federal regulators, and regional transmission organizations is more complex. Projects are often discrete and fragmented, and equipment manufacturers therefore find it much harder to organize capacity around unified standards and long-cycle batch demand.

The third difference is that China looks more like cluster-based industrial supply, while the United States looks more like a small number of firms taking orders. Large transformers are not standalone products. Behind them is a full supporting system involving grain-oriented electrical steel, copper, insulation materials, bushings, tap changers, coils, testing equipment, heavy transport, and on-site installation. China’s advantage in many categories of heavy electrical equipment does not simply come from having more final assembly plants. It comes from the fact that surrounding component makers, material suppliers, engineering teams, construction systems, and local government support all sit within the same dense industrial network. The benefit is not just lower cost. More importantly, coordination is faster and supply response is more continuous. The United States, by contrast, has long depended on imported large power transformers, while domestic capacity remains limited and both upstream materials and skilled labor remain tight. Once demand surges in concentrated fashion, lead times stretch almost immediately. On the surface, both sides may be said to “make transformers.” In substance, one system can mobilize almost the entire chain together, while the other can only move some parts of the chain. The outcomes are naturally different.

The fourth difference is that China is better able to bundle demand into standardized capacity expansion, while the United States is more likely to be slowed by institutional friction. America’s problem is not that there is no money, nor that firms are unwilling to invest. It is that the process from grid interconnection and permitting to interstate coordination and large-load connection is much more fragmented. For firms, this means downstream project timing is not fully controllable, which makes it difficult to commit heavy capital in advance around relatively certain demand in the way Chinese firms can. China’s logic is the opposite. First come clear plans for major transmission corridors, regional dispatch, and investment priorities; then manufacturing expansion is pulled forward around that framework. That sequencing matters enormously. It means Chinese equipment manufacturers are expanding continuously along a direction that is already broadly known, while American firms are waiting for projects to clear in an environment that is much more uncertain and much slower in approvals and execution.

The fifth difference is that China places greater emphasis on engineering delivery capability, while the United States places greater emphasis on market response capability. In ordinary consumer goods, software, or parts of light industry, market responsiveness can indeed be more efficient. But in a slow industry such as large transformers, ultra-high-voltage equipment, and transmission engineering, what determines delivery efficiency is not the speed of price quotations. It is sustained investment, engineering reuse, skilled labor formation, supply-chain support, and organizational coordination. Hitachi Energy, Siemens, and Eaton are all investing further in the United States, but much of their additional capacity will not be meaningfully available until around 2027. That in itself shows that even with global leaders expanding, the U.S. domestic system still needs years to catch up. China’s relative ability to avoid the pattern of “many orders, slow delivery” does not come from having no bottlenecks. It comes from the fact that over the past decade and more, many of the key links have already been internalized in advance.

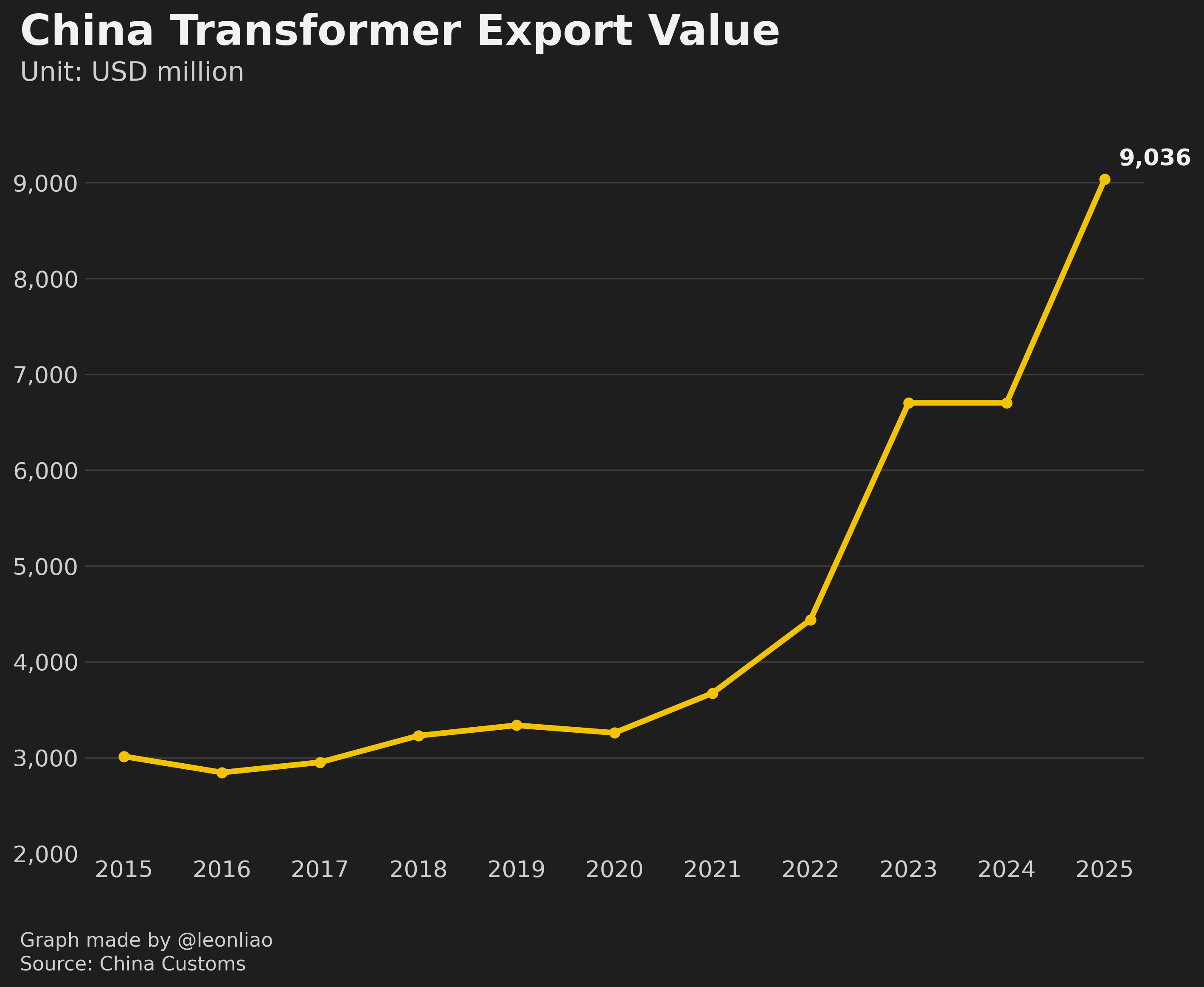

That is also why the visible acceleration in China’s transformer exports in recent years is not an accident. From 2015 to 2020, China’s transformer exports mostly fluctuated between roughly USD 2.8 billion and USD 3.3 billion, reflecting steady but not dramatic growth. But beginning in 2021, export value accelerated clearly, rising to USD 3.672 billion, USD 4.439 billion, USD 6.702 billion, USD 6.702 billion, and USD 9.036 billion. This is no longer a normal linear fluctuation. It is a more structural spillover outcome formed by the combined effects of global grid upgrades, renewable integration, data-center expansion, and insufficient domestic supply capacity in some countries. It shows that China is not only a major producer of transformers, but is increasingly acting as an external supplier of power equipment to the world. As long as the United States and Europe continue to face pressure in large transformers, distribution equipment, and delivery timelines, China’s export growth is likely to be not merely a cyclical phenomenon, but part of a broader structural uptrend.

If the United States is this short on supply, why doesn’t it just import large power transformers from China on a much larger scale?

On the surface, this looks like a very straightforward question. But the answer is more complicated than simply saying “geopolitics.” More precisely, the United States is not completely absent from importing transformers from China. The point is that in the more critical subcategories of large liquid dielectric main transformers, China is not America’s primary source.

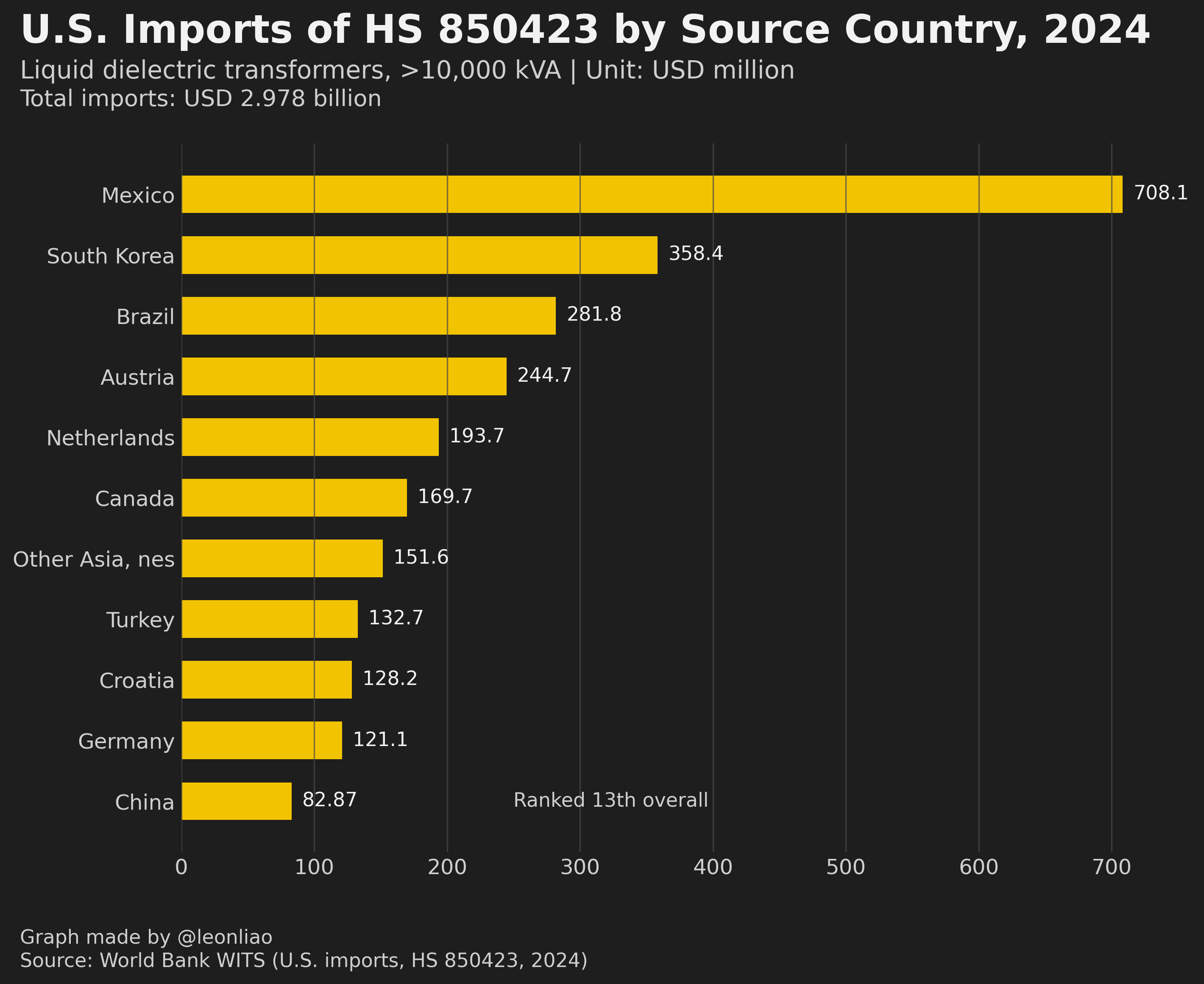

If we break the data down to the HS6 level, the two U.S. 2024 product codes closest to large liquid dielectric power transformers are 850423, which refers to liquid dielectric transformers with a capacity above 10,000 kVA, and 850422, which refers to liquid dielectric transformers with a capacity between 650 and 10,000 kVA. In the 850423 category, which is closer to large main transformers, U.S. imports in 2024 were close to USD 3 billion. The main source countries were Mexico, South Korea, Brazil, Austria, the Netherlands, Canada, Turkey, Croatia, and Germany, while China ranked much further down the list. This suggests that in the most critical category of large liquid dielectric main transformers, the United States relies more heavily on North American nearshoring, South Korea, and mature European manufacturing bases than on China.

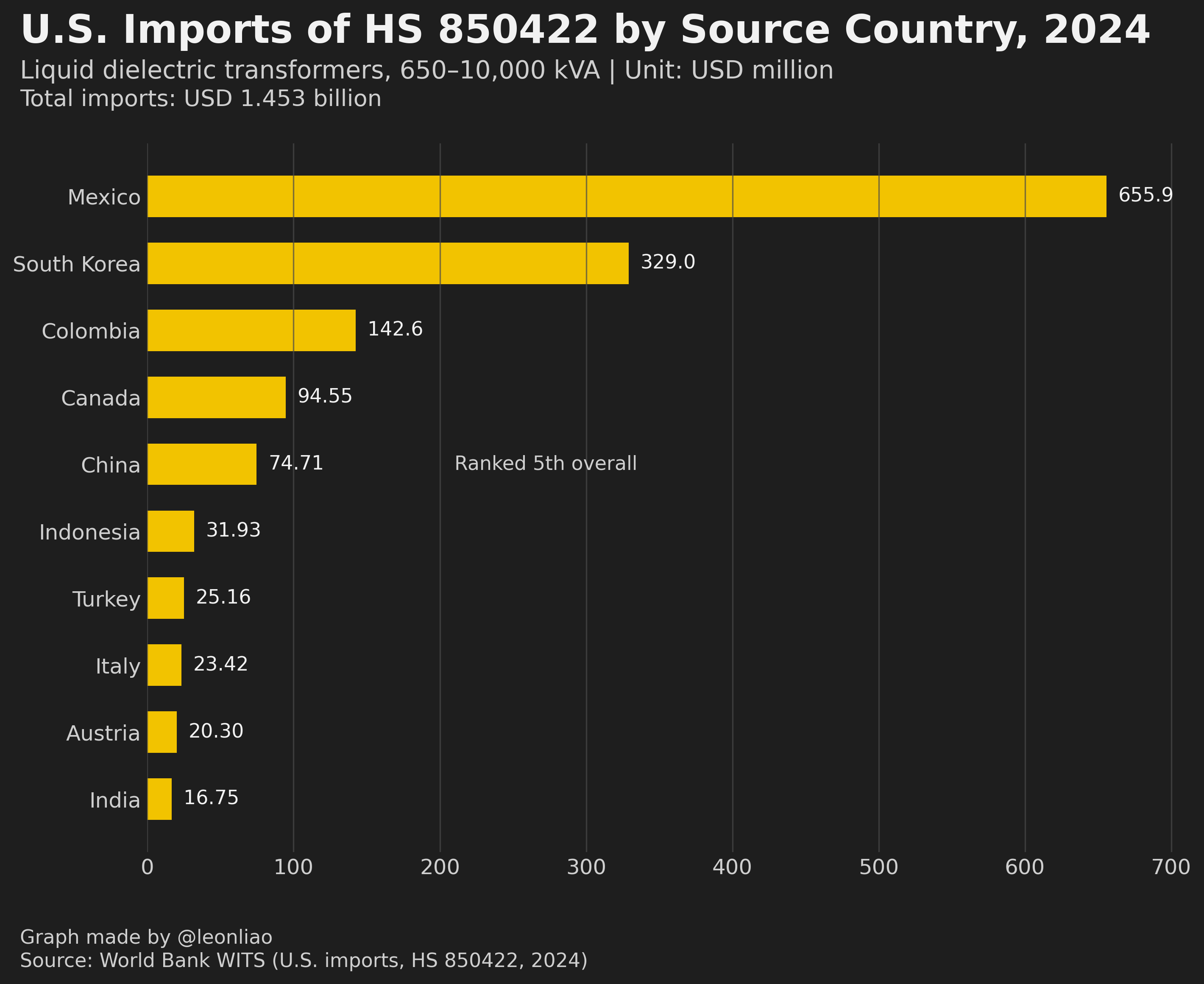

But in the 850422 subcategory, which covers medium-to-large liquid dielectric transformers, China’s importance has already started to rise. In U.S. imports of this category in 2024, Mexico and South Korea remained the main suppliers, but China had already entered the top five. That means China is not absent from the U.S. market. Rather, the closer one gets to the layer of larger, higher-voltage, more certification-intensive, and more project-complex main transformers, the more the U.S. procurement system tends to rely on existing North American and allied supply chains.

Why is that? First, because the United States in recent years has broadly emphasized nearshoring, localized assembly, North American certification, transport accessibility, and supply-chain security. Large transformers are not small or lightweight electronic products. They are extremely difficult to transport, and their delivery and installation are deeply tied to local engineering systems. That gives countries like Mexico and Canada natural advantages. Second, the utility and grid-equipment market is itself highly conservative. Customer certification, long-term relationships, project experience, and after-sales service all matter enormously. Countries such as South Korea, Austria, Germany, and Turkey, which already have deep industrial capabilities in high-voltage and large-transformer manufacturing, therefore find it easier to win U.S. orders. Third, the United States is not willing to deepen dependence on China at large scale in the most critical category of core grid equipment. In other words, it is not that China lacks capability. It is that within this U.S. supply chain, capability does not automatically translate into market share.

If one compares the U.S. import-source structure with the broader global export structure, this contradiction becomes even clearer. On the one hand, China is already a major supplier in the global export market for products such as 850423 and 850422, which shows that China is indeed strong on the global supply side. On the other hand, the actual U.S. import structure has not followed global supply shares mechanically. Instead, it is clearly shaped by the combined influence of North American nearshoring, existing certification systems, transport logic, and geopolitical preferences. In other words, the United States does not allocate large-transformer imports simply by looking for the cheapest or most abundant global supplier. It embeds industrial, geographic, institutional, and political factors into its procurement system at the same time. The result is that even in a state of shortage, it does not necessarily pivot sharply toward the direction with the greatest global supply potential.

Conclusion

Taken as a whole, the tightness in U.S. transformer supply is not merely a question of equipment shortage. It is an early stress test of national industrial capacity exposed by the AI-driven power supercycle. America’s problem is not that it is completely unable to manufacture these products, nor that it is completely unable to buy them. The problem is that it cannot manufacture them quickly enough, cheaply enough, or in a sufficiently systematized way, while procurement is simultaneously constrained by nearshoring preferences, certification systems, transport radius, and geopolitics. The result is that orders are arriving, projects are queuing, data centers are expanding, and grids are being upgraded, but the most critical layers of heavy industrial equipment are unable to keep pace.

China’s greater ability to form a systematic supply is also not because one particular company is somehow magically stronger. It is because behind China stands a unified long-term buyer, a large-engineering system built on repeatable project execution, a relatively complete domestic supply chain, and lower institutional coordination friction. The United States is more likely to fall into the pattern of “many orders, slow delivery” because in this category of heavy industrial infrastructure, long-term demand has been less continuous, supply-chain localization is weaker, and project approval and grid interconnection are more fragmented. As a result, the supply system lacks the kind of organized, formation-level expansion capacity that China has built. And when this is combined with the fact that the United States is unwilling to significantly deepen dependence on China in the most critical category of large grid equipment, the supply tightness is amplified even further.

Of course, this does not mean China faces no constraints across all power equipment categories, nor does it mean the United States can never catch up. America is expanding capacity, and global electrical giants are investing more heavily in the U.S. China, too, would face localized bottlenecks if its own demand were to accelerate much further. But at the current stage, the biggest difference between the two is real: China has already treated this category of equipment as a national foundational capability, while the United States is only now being forced by AI, grid aging, and manufacturing reshoring to relearn how to turn these seemingly “old industrial” products into a system that can expand on a sustained basis.