Inside China’s Shipbuilding Boom

Global Shipowners Are Sending the Orders of the Green Shipping Era to Chinese Yards

China’s shipbuilding order boom reveals a deeper industrial fact: the global transition toward green shipping is increasingly relying on China’s ability to organize steel, engines, shipyards, workers, engineers, finance, ports, software, and supply chains into one complete industrial system.

This essay is part of China Industry Signals.

Executive Summary

China has become the central production base for global shipbuilding demand. In Q1 2026, China accounted for 84.9% of global new shipbuilding orders by deadweight tonnage, 57.3% of completions, and 69.8% of the global orderbook.

The boom is export-driven. Export vessels accounted for 96.1% of China’s completed shipbuilding volume in Q1 2026, showing that Chinese yards are primarily serving global fleet renewal.

Green vessels are the core of the new cycle. China’s share of global new green-vessel orders reached 80.2% in Q1 2026, covering LNG, LPG, methanol, ethane dual-fuel vessels, and electric ships.

China’s advantage is shifting from scale to system capability. Large yards, dense supplier clusters, modular production, digital scheduling, financial support, and after-sales response are making Chinese shipyards attractive to global shipowners.

South Korea remains the key high-end competitor. HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean still hold strong positions in LNG carriers, FPSO, naval vessels, and high-value eco-friendly ships.

Japan shows the limits of traditional industrial strength without scalable capacity. Imabari Shipbuilding and Japan Marine United still matter, but Japan’s shipbuilding sector faces capacity constraints, aging labor, and a shrinking global share.

The Qianlong Emperor’s Southern Inspection Tour, Scroll Six: Entering Suzhou along the Grand Canal (乾隆南巡图,第六卷:大运河至苏州)

By Xu Yang, Qing Dynasty

Its canals, boats, bridges, roads, officials, merchants, and urban networks echo the central theme of this essay: China’s shipbuilding boom as an organized maritime-industrial system rather than a simple export cycle.

At a modern shipyard, the scale of industrial power is visible in the silence before a giant hull moves, in the slow swing of a gantry crane, in the rows of steel blocks waiting to be assembled, in the workers walking beneath structures that dwarf human bodies, and in the long production schedules pinned years into the future. A shipyard is one of the few industrial spaces where a country’s manufacturing capacity can still be seen almost physically. Steel, engines, cables, valves, software, welding, logistics, finance, and labor discipline all have to meet in one place. Nothing can be faked for long.

In recent years, this scene has increasingly been found in China’s coastal shipbuilding bases — Shanghai’s Changxing Island, Dalian, Nantong, Guangzhou, Qingdao, Zhoushan, Yangzhou, and other industrial waterfronts where massive hulls are being built, fitted out, tested, and delivered to global shipowners. Some of these ships will carry liquefied natural gas across oceans. Some will move electric vehicles from Chinese ports to Europe, Latin America, Southeast Asia, and the Middle East. Some will transport crude oil, grain, minerals, or containers. Some are designed around methanol, LNG, electric propulsion, or other low-carbon fuel systems. They are commercial vessels, but they also reveal something strategic: global trade and green shipping are being rebuilt through physical industrial capacity.

The shipyard is a useful corrective to the way many people now talk about technology and competition. It is easy to focus on software, chips, AI models, or financial markets because they move faster and generate cleaner narratives. Shipbuilding is slower, heavier, and more stubborn. It requires land, docks, cranes, engineers, welders, skilled technicians, suppliers, power systems, marine equipment, port infrastructure, ship finance, and a long chain of industrial trust. A ship cannot be improvised through capital alone. It has to be organized through a production system.

That is why China’s latest shipbuilding data matter. The numbers are not just another export statistic. They show where global shipowners believe future delivery capacity resides. When a shipowner signs a contract for an LNG carrier, a methanol dual-fuel container ship, a car carrier, or a very large crude carrier, the decision is not only about price. It is a judgment about whether a yard can deliver on time, coordinate thousands or millions of components, meet emissions requirements, secure supply chains, provide financing support, and service the vessel over its operating life. In shipbuilding, orders are long-term votes of confidence in an industrial system.

This is the real meaning of China’s current shipbuilding boom. It is a cycle of global fleet renewal, but it is also a visible expression of China’s accumulated manufacturing power. The same country that built deep supply chains in steel, machinery, port equipment, power systems, new-energy vehicles, batteries, wind power, and electrical equipment is now turning those capabilities into maritime industrial strength. The result is not only more ships. It is a broader shift in the geography of global industrial capacity.

1. Global Orders Are Flowing Into Chinese Shipyards

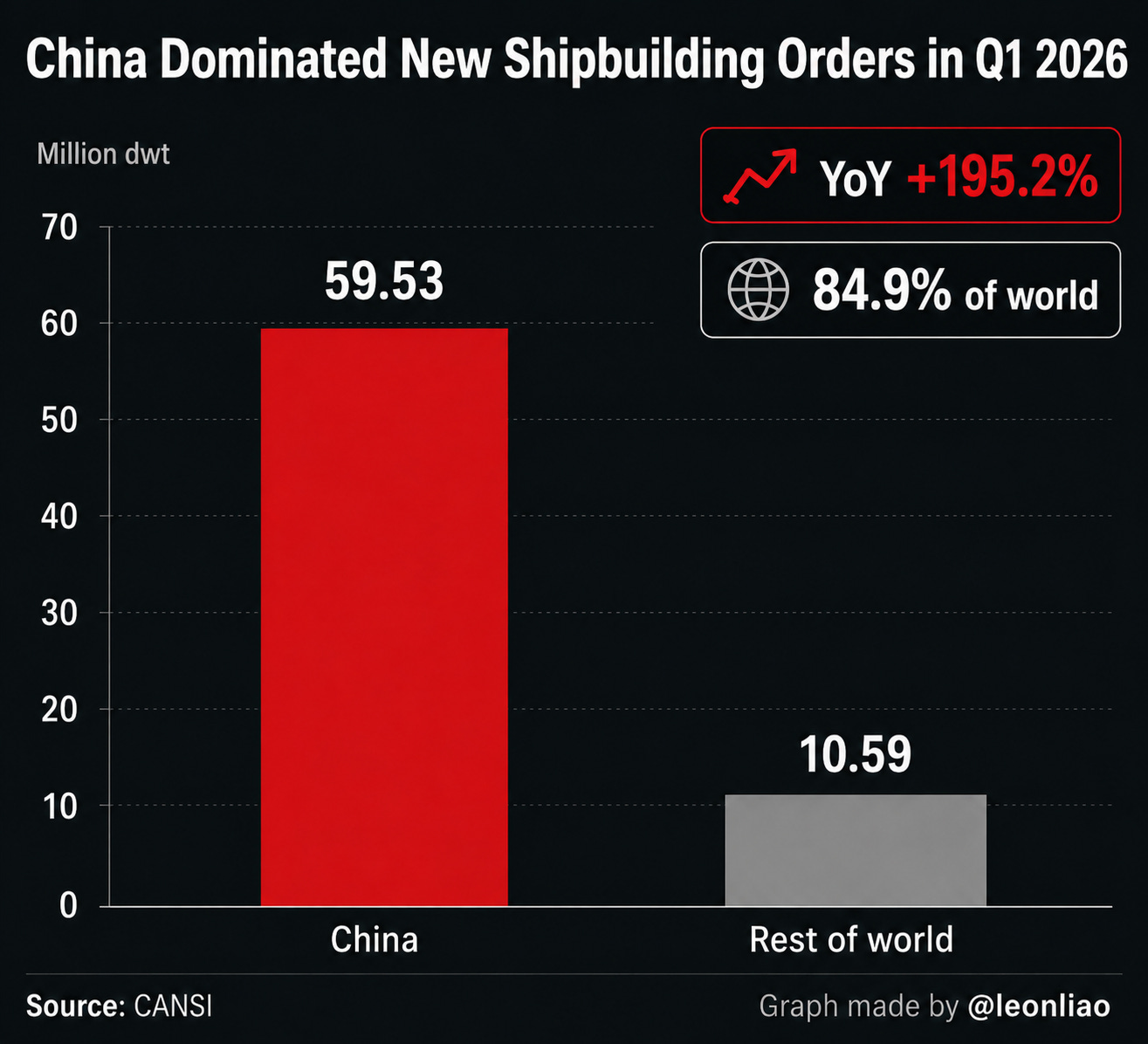

China’s shipbuilding industry continued to grow strongly in Q1 2026. China completed 15.68 million DWT of shipbuilding, up 46.0% year on year, accounting for 57.3% of the world total.

New orders reached 59.53 million DWT, up 195.2% year on year, accounting for 84.9% of the world total.

As of the end of March, China’s orderbook stood at 322.30 million DWT, up 43.6% year on year, accounting for 69.8% of the global total.

Even more important, export vessels accounted for 96.1% of China’s completed shipbuilding volume in the quarter. This shows that the high prosperity of Chinese shipyards is not simply being driven by domestic demand. Global shipowners are handing the next round of fleet renewal, energy transition, and capacity deployment orders to China.

The full-year 2025 data had already laid the foundation for this upward cycle. China completed 53.69 million DWT of shipbuilding, received 107.82 million DWT of new orders, and held 274.42 million DWT of orders on hand. China’s ship exports reached $55.08 billion, up 26.7% year on year. By export structure, bulk carriers, oil tankers, and container ships together accounted for $30.46 billion, or 55.3% of total ship-product exports. This means China’s shipbuilding exports are not a scattered short-term increase across a few vessel categories. They represent a systematic expansion from traditional mainstream vessel types into higher-value vessel segments.

The most important signal in recent Chinese media coverage is that global shipowners’ choices are shifting from cost comparison to delivery certainty comparison. People’s Daily Overseas Edition and Xinhua, in their report “Global Shipowners Look to China,” noted that international shipowners returned noticeably to the Chinese market in 2025, with nearly nine out of every ten vessels built in China serving global shipping markets. The report cited orders placed with Chinese shipyards by Singapore’s EPS, Greece’s Dynacom, Arcadia and Danaos, and Germany’s Asiatic Lloyd. These cases show that global shipowners are entering Chinese yards from multiple market segments. This is not limited to Asian shipowners. It also includes traditional European shipping capital.

Shipowners choose China first because of delivery capability. Shipbuilding is a classic long-cycle, heavy-asset, engineering-intensive industry. The construction of a large vessel involves design, procurement, steel processing, block construction, assembly, launching, outfitting, sea trials, and final delivery. It requires coordination across a large number of processes. What shipowners buy is not the isolated capability of one yard. They are buying an entire on-time delivery system. Over the past few years, global shipping has experienced high volatility in container freight rates, restructuring in energy transportation, rising demand for car carriers, and a shift toward green-fuel vessel types. For shipowners, the ability to secure shipyard slots, deliver on schedule, and guarantee follow-up maintenance services has become as important as price.

CCTV’s report on Hudong-Zhonghua offers a vivid on-site example. Yang Chunhua, director of the development institute at CSSC Hudong-Zhonghua, said the company delivered 11 LNG carriers in 2025, setting an industry record. It currently holds more than 80 vessels in its orderbook, with production schedules extending to 2030, and 80% of these orders come from global green-vessel demand. This detail matters. LNG carriers have long been regarded as one of the “crown jewels” of shipbuilding. They involve cryogenic materials, cargo-containment systems, dual-fuel propulsion, automatic control, system integration, and extremely high reliability requirements. If a Chinese yard’s LNG carrier orders are already scheduled into 2030, China’s role in the global high-end vessel market has materially changed.

Another important set of data comes from global vessel-type distribution. In Q1 2026, among the world’s 18 major vessel types, China ranked first globally in new orders for 15 vessel types. Its international market share exceeded 90% for very large crude carriers, large car carriers, bulk carriers, and container ships above 10,000 TEU. This data is more meaningful than the total order share alone. It shows that China’s shipbuilding industry is not relying only on bulk carriers, lower-end ships, or a single mainstream category to gain scale advantage. It is winning overwhelming shares across multiple large vessel segments at the same time.

This is also where shipbuilding differs most from many consumer-goods export industries. A ship is a mobile industrial complex. Behind a large LNG carrier, car carrier, container ship, or offshore engineering vessel are steel, engines, cryogenic materials, coatings, valves, navigation systems, control software, deck machinery, power systems, port services, financial insurance, and long-term operations and maintenance. China’s share of new shipbuilding orders reflects a comprehensive vote by global shipowners on China’s industrial system.

2. China, South Korea, and Japan: The Triangle of Global Shipbuilding

To understand the high prosperity of China’s shipbuilding industry, South Korea and Japan must be placed in the same coordinate system. China has already taken the global lead in order scale, vessel-type coverage, supply-chain completeness, and delivery capability. South Korea remains the core competitor in high-value vessel types. Japan, once a dominant shipbuilding power, is facing pressure from capacity constraints, labor shortages, and industry restructuring.

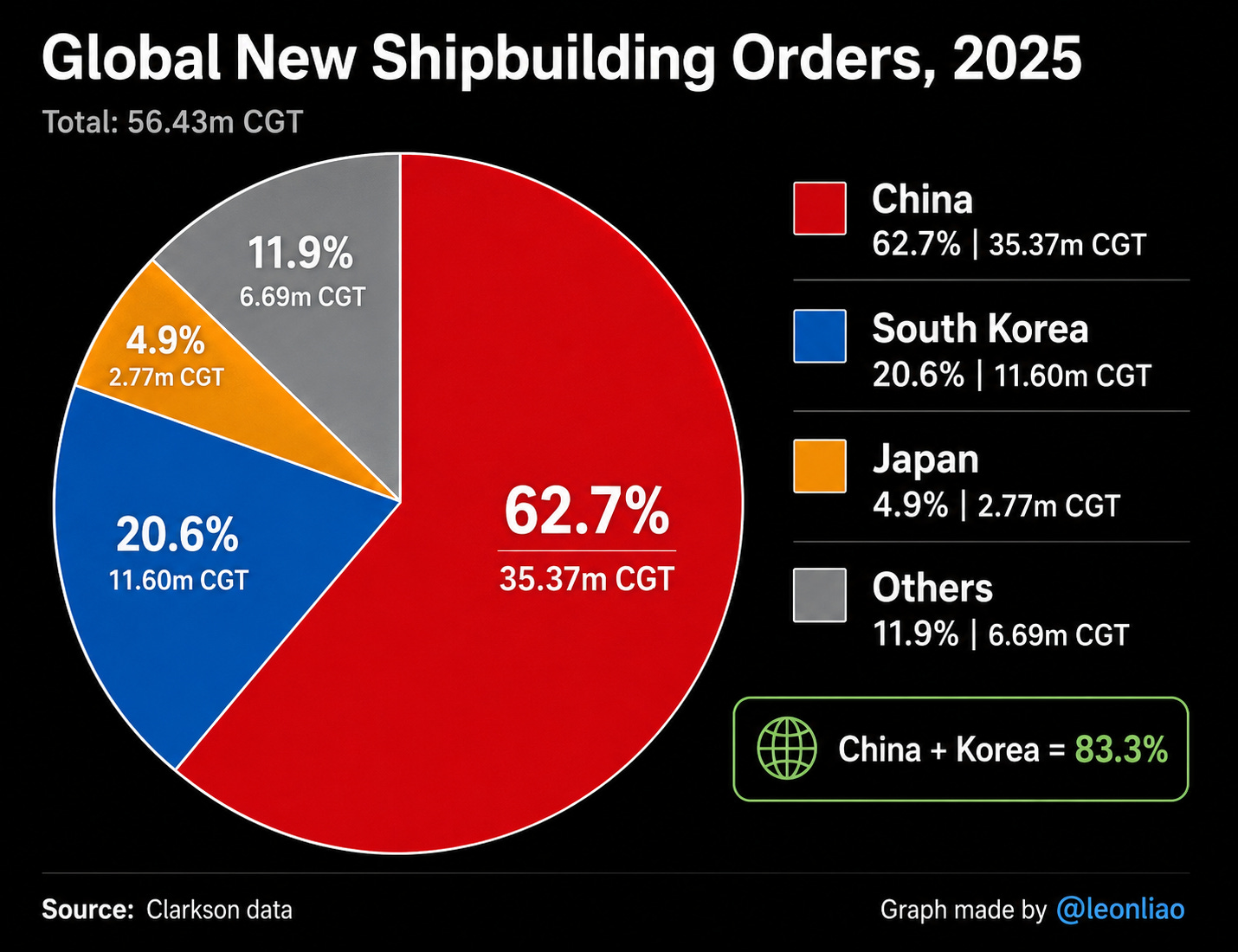

According to Clarkson’s CGT measure, global new shipbuilding orders in 2025 totaled roughly 56.43 million compensated gross tons. Chinese yards received about 35.37 million CGT, or roughly 63% of the global total. Korean yards received about 11.60 million CGT, or roughly 21%. This measure is more reflective of vessel complexity and construction value than deadweight tonnage, because CGT adjusts for the technical complexity of different vessel types. Even when measured by CGT rather than DWT, China already holds a clear lead in global new shipbuilding orders.

South Korea’s position remains very important. The OECD’s 2026 peer review of the Korean shipbuilding industry noted that South Korea remains the world’s second-largest shipbuilding country and has focused strategically on high-value-added and eco-friendly vessels. After the downturn of the mid-2010s, South Korea’s shipbuilding sector consolidated further around three major groups: HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean. These three companies form the core of Korean shipbuilding. They still possess strong technical brands and customer bases in LNG carriers, ultra-large container ships, FPSO, offshore engineering equipment, naval vessels, and eco-friendly fuel ships.

HD Hyundai is one of the most important representatives of Korean shipbuilding. HD Hyundai Heavy Industries has long been in the global first tier for large vessels, with strong positions in large tankers, container ships, LNG carriers, and naval vessels. Samsung Heavy Industries has deep experience in LNG carriers, FLNG, FPSO, and complex offshore engineering equipment. Hanwha Ocean, formerly Daewoo Shipbuilding & Marine Engineering, has strengthened its focus on naval vessels, LNG carriers, and Korea-U.S. shipbuilding cooperation under the Hanwha Group. After Hanwha acquired Philly Shipyard in the United States, it became not only a Korean shipbuilder but also an important allied enterprise in America’s attempt to restore shipbuilding capacity.

South Korea therefore still holds part of the high-end, complex-vessel market and retains trust from global shipowners. Competition between China and South Korea has entered a new stage. In the past, the question was who could build more ships. Now the question is who can simultaneously organize large-scale delivery, complex engineering, green-fuel systems, shipowner financing, and global service networks.

Japan offers another point of comparison. Japan was once an absolute global shipbuilding power. Companies such as Imabari Shipbuilding, Japan Marine United, Oshima Shipbuilding, and Tsuneishi Shipbuilding still have extensive engineering experience and customer relationships. But Japan’s global shipbuilding share has fallen significantly. In recent years, Japan has pushed industry consolidation, such as Imabari Shipbuilding’s acquisition of a controlling stake in Japan Marine United, in an attempt to create a larger group capable of competing with China and South Korea. This consolidation itself shows that Japan’s shipbuilding industry understands a hard reality: traditional engineering experience cannot fully offset pressure from capacity scale, cost structure, labor supply, and supply-chain density.

Reuters’ reporting on NYK Line’s management provides a valuable reality check. Takaya Soga, NYK’s chief executive, has said that Japanese shipbuilding capacity is almost fully booked through 2028, making it difficult to expand capacity quickly in the short term. Korean yards and U.S. yards also face financial constraints. This judgment is important because the United States is trying to shift shipowner orders away from China and toward its allied system. But shipbuilding capacity cannot be replicated through political slogans. Shipyard slots, skilled workers, steel supply, engines, design systems, supplier networks, and financial support all require long-term accumulation.

China, South Korea, and Japan therefore form a clear global shipbuilding structure. China has the strongest combination of scale, vessel-type coverage, and supply-chain organization. South Korea remains an important competitor in high-end and complex vessels. Japan represents the pressure facing traditional industrial powers in a new era of system-level industrial competition. This structure means that, in the short term, global shipowners will find it very difficult to identify a true large-scale substitute for Chinese yards.

3. Green Vessels Have Become the Core of New Orders

The most important change in this cycle of high prosperity in Chinese shipbuilding is the deep shift in order structure. In Q1 2026, China’s share of global new green-vessel orders reached 80.2%. New orders covered LNG, LPG, methanol, ethane dual-fuel vessels, and electric ships. Methanol-powered, LNG-powered, pure-electric, and other new-energy vessels are being delivered intensively and launched in batches. This shows that Chinese yards have entered the stage of green-vessel competition.

Several cases in recent CCTV and Xinhua reports illustrate this shift well. China’s self-developed “Kun” series 15,000-TEU methanol dual-fuel container ship was delivered successfully, with estimated annual carbon dioxide emissions reductions of about 120,000 tons. The Tianshan, a 174,000-cubic-meter large LNG carrier, was delivered using a latest-generation dual-fuel system. The Innovation 19, China’s first single-methanol-fuel river-sea direct bulk carrier, reduces carbon dioxide emissions by 90% and almost eliminates sulfur oxide emissions. These vessel types point to a common trend: green vessels have moved from demonstration projects into batch-order production.

Global shipping is facing IMO decarbonization targets, EU carbon-market pressure, fuel switching, an aging fleet structure, and uncertainty over new technology pathways. When shipowners place orders, they must consider not only ship prices but also which vessel types will be better able to meet emissions standards over the next ten or twenty years. LNG, methanol, ammonia, hydrogen, electrification, wind-assist systems, and energy-efficiency management systems are all entering ship design and fleet-renewal decisions. This stage imposes higher requirements on shipyards. Yards cannot only weld steel plates. They must understand fuel systems, tank safety, cryogenic engineering, propulsion systems, control software, port refueling infrastructure, and full lifecycle operations and maintenance.

Chinese yards’ advantages in green vessels come from several layers.

First, vessel-type coverage is broad. China has already built a complete product spectrum across bulk carriers, oil tankers, container ships, car carriers, LNG carriers, and offshore engineering equipment.

Second, the manufacturing base is deep. A green vessel is not a standalone technology product. It is an integrated system of materials, equipment, electronics, propulsion, and process engineering.

Third, delivery scale is large. Only with sufficient order scale can green vessel types move quickly from first-of-class ships to series production, reducing costs, shortening construction cycles, and improving quality stability.

Fourth, supply-chain support is strong. Shipowners are not only buying ships. They are also buying follow-up services, spare-parts supply, and engineering response.

Hudong-Zhonghua’s LNG carrier case is especially illustrative. Science and Technology Daily has reported that the construction difficulty of LNG carriers is comparable to that of aircraft carriers. The containment system alone contains more than 3 million components and involves fluid mechanics, cryogenic materials, automatic control, and multiple other fields of expertise. Xinhua has also reported that Hudong-Zhonghua has reduced the production time for a large LNG carrier from more than 30 months in the past to 17 months. It is expected to deliver 11 large LNG carriers in 2025. The transition from being able to build LNG carriers to delivering them in batches is ultimately the combined result of engineering experience, supply-chain maturity, process discipline, and project-management capability.

This also explains why South Korea remains China’s most important competitive coordinate. Korean yards have long held advantages in LNG carriers, FLNG, FPSO, and other complex high-end vessel types. When new LNG carrier orders recovered at the end of 2025, Samsung Heavy Industries, Hanwha Ocean, and HD Hyundai Samho remained important recipients of global orders. China is catching up rapidly in LNG carriers, but China-Korea competition will continue for a long time. The key question going forward is not only single-vessel technology. It is who can turn complex vessel types into stable delivery capacity and expand green vessels from a small group of high-end customers to a broader base of global shipowners.

Car carriers are another important observation point. China’s rapid growth in new-energy vehicle exports has driven rising demand for roll-on/roll-off car carriers. Chinese shipbuilders’ high share of large car-carrier orders is itself a supporting result of China’s automobile exports. When a country’s automobile industry, port logistics, shipbuilding, and shipping finance reinforce each other, the entire export system extends from producing goods to organizing transportation systems. Shipbuilding is therefore not only a foreign-trade industry. It is the maritime infrastructure of China’s global supply-chain capability.

4. Shipbuilding Reveals China’s Industrial System Capability

Shipbuilding is one of the best tests of a country’s industrial system capability because it compresses a large number of industrial sectors into one vessel. Behind a large ocean-going ship are steel, engines, generators, shafting, propellers, cryogenic equipment, valves, pumps, piping, coatings, welding materials, cables, navigation, communications, control systems, deck machinery, fire-safety systems, life-saving systems, cabin engineering, docks, logistics, and finance. This industry is very difficult to win through a single technological breakthrough.

The People’s Daily Overseas Edition and Xinhua reports on Changxing Island show clearly why shipbuilding is such a powerful test of industrial-system capability. On Shanghai’s Changxing Island, central state-owned enterprise leaders such as Hudong-Zhonghua and Jiangnan Shipyard have pulled together more than 7,000 supporting enterprises, forming an ecosystem of “final assembly + supporting suppliers.” From marine steel plates to engines, from navigation systems to deck machinery, China has built a relatively complete shipbuilding supply-chain system. The reports also note that shipowners in different regions have different product requirements: Southeast Asian markets focus more on cost efficiency and adaptability; EU markets place high importance on compliance and sustainability; American markets have higher requirements for automation integration and smart systems. This shows that Chinese yards are serving highly differentiated global demand rather than a single low-price export market.

Changxing Island is a classic window into China’s shipbuilding system capability. People’s Daily reported in May 2026 that the localization rate of supporting equipment for Jiangnan Shipyard and Hudong-Zhonghua on the island has risen from less than 30% more than a decade ago to around 80% today. In 2025, the island’s shipbuilding and offshore engineering equipment output value exceeded RMB 90 billion. Shanghai has proposed that Changxing Island’s industrial scale should exceed RMB 120 billion by 2027. This change shows that the rise of China’s shipbuilding capability is not only about the expansion of a few leading companies. It is the joint evolution of industrial clusters, supplier capability, R&D organization, engineering talent, and local industrial foundations.

The manufacturing process of shipbuilding is also becoming more digitalized. In the past, shipbuilding production planning relied heavily on the experience of senior technicians. Blocks, assembly, equipment installation, pipe laying, dock resources, and worker scheduling all required complex coordination. Recent industry reports have mentioned that AI-based autonomous production planning can raise workshop capacity by 25%. This detail matters because the efficiency bottleneck in shipbuilding often does not lie in one piece of equipment. It lies in multi-process coordination. If digital scheduling can reduce waiting time, rework, and resource conflicts, it directly improves shipyard delivery capacity.

China’s competitiveness in shipbuilding is also reflected in the full experience of “available to buy, affordable to use, and fast to repair.” Xinhua has reported that, compared with foreign-brand components that have long supply cycles and high maintenance costs, Chinese shipbuilders have advantages in service and response. Their after-sales response time is shorter, and engineering support is more flexible. For global shipowners, a vessel is not a one-time consumer product. It is a heavy asset that operates for more than ten or even twenty years. Spare-parts supply, maintenance response, software upgrades, troubleshooting, and refit support all affect fleet operating costs. The rapid-response capability China has developed in other manufacturing industries is now entering a heavy industrial-equipment field like shipbuilding.

Offshore engineering equipment should also be placed in this framework. Data from the China Association of the National Shipbuilding Industry show that in 2024, China received new orders for 108 units of offshore engineering equipment, worth about $18.6 billion, accounting for 69.4% of the global total. China has ranked first globally for seven consecutive years. Offshore engineering equipment connects oil and gas development, offshore wind power, deep-sea operations, marine engineering services, and energy infrastructure. China’s share in offshore engineering equipment shows that its maritime industrial capability is no longer limited to traditional merchant ships. It is extending into offshore energy and complex engineering platforms.

This is also the deeper connection between China’s shipbuilding industry and China’s other advanced manufacturing industries. New-energy vehicles, power batteries, solar, wind power, electrical equipment, port machinery, construction machinery, steel, and shipbuilding appear to be different industries. In reality, they share many underlying capabilities: large-scale manufacturing, supply-chain density, engineering talent, continuous cost reduction, local industrial clusters, export service systems, and policy support. Chinese yards can quickly absorb green-vessel orders because they stand on top of a vast industrial ecosystem.

5. Why the United States Has Begun to Treat Shipbuilding as a National Security Issue

China’s global shipbuilding expansion has moved from commercial competition into geoeconomic industrial competition.

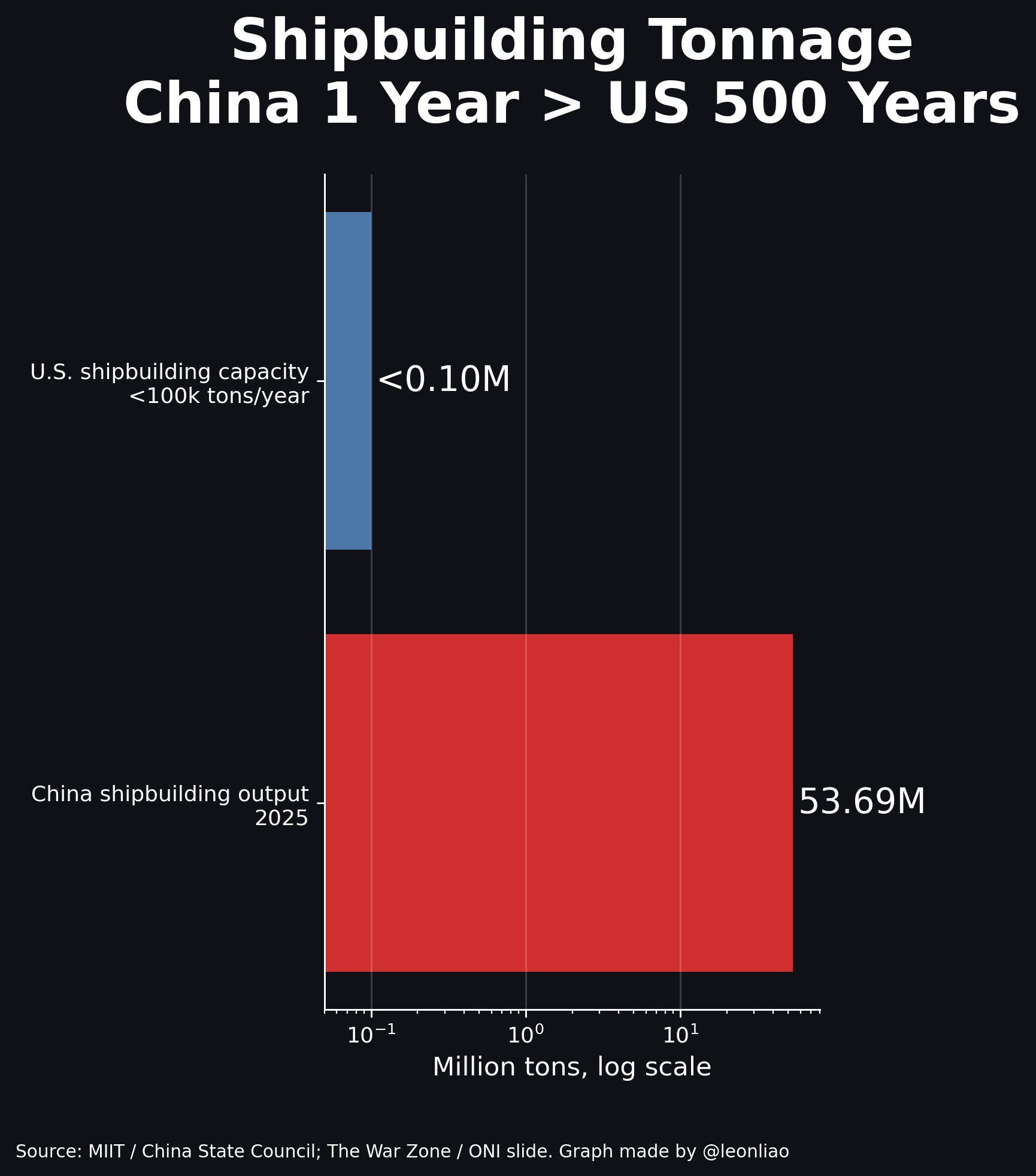

China’s 2025 shipbuilding output was larger than more than 500 years of current U.S. shipbuilding capacity. China completed 53.69 million DWT of shipbuilding in 2025. The United States’ current annual shipbuilding capacity is often estimated at less than 100,000 tons.

This is not just a shipbuilding gap. It is an industrial-capacity gap in steel, ports, suppliers, skilled labor, engineering organization, and wartime production potential.

In 2025, the Office of the United States Trade Representative initiated and advanced Section 301 action targeting China’s maritime, logistics, and shipbuilding sectors, explicitly focusing on “China’s dominance in the maritime, logistics, and shipbuilding sectors.” USTR argued that China’s related policies and practices harmed U.S. companies, workers, and economic interests, while creating supply-chain dependence and economic-security risks. The United States then proposed fees on Chinese vessel operators, China-built vessels, and certain foreign-built car carriers, while also trying to use policy tools to rebuild U.S. shipbuilding capacity.

The real meaning of this move is that the United States has redefined shipbuilding from an ordinary industrial sector into a national-security infrastructure sector. The reason is straightforward. A country without sufficient merchant-shipbuilding capacity must rely on foreign yards to renew its fleet. A country without enough port equipment and maritime-equipment capability becomes dependent on others inside logistics networks. A country without a complete shipbuilding industrial base will also see its naval construction, maintenance, and mobilization capability affected. Commercial shipbuilding and military shipbuilding share many foundations: shipyards, welding workers, hull design, propulsion systems, steel, electronics, suppliers, and project-management capability. American anxiety over Chinese shipbuilding reflects anxiety over maritime power after the erosion of industrial foundations.

America’s effort to use South Korea and Japan to restore its own shipbuilding capacity also shows that China’s shipbuilding advantage has reached a level the United States cannot easily handle alone. Reuters has reported that the Trump administration believed the United States needed allies such as Japan and South Korea to help revitalize its shipbuilding industry, especially given its lag behind China in naval construction. Hanwha Ocean acquired Philly Shipyard and announced additional investment. HD Hyundai Heavy Industries has also discussed cooperation with U.S. shipyards and defense shipbuilding companies. Korean shipbuilders are being incorporated into America’s policy framework for rebuilding maritime industrial capability.

But the judgment from NYK’s management in Japan points to a practical reality: replacing Chinese yards is difficult. Japanese shipbuilding capacity is already largely booked through 2028. Korean yards also face their own financial and capacity constraints. U.S. domestic shipbuilding faces long-term underinvestment, shortages of skilled workers, aging yard facilities, high costs, and insufficient commercial orders. Global shipowners can adjust some orders under political pressure, but the distribution of global shipbuilding capacity cannot be reshuffled within just a few years.

The friction between China and the United States over shipbuilding has also pushed Korean companies into a complicated position. Reuters reported in October 2025 that China imposed sanctions on five U.S.-related subsidiaries of Hanwha Ocean, saying those subsidiaries had assisted and supported U.S. government investigations and harmed China’s sovereignty, security, and development interests. Hanwha Ocean is, on one hand, a Korean high-end shipbuilder. On the other hand, through Philly Shipyard, it has entered America’s shipbuilding-revival plan, while still maintaining links to Chinese supply chains. This triangular relationship shows that shipbuilding has become an intersection of China-U.S. industrial competition, Korean corporate global strategy, and allied-system restructuring.

Japan faces a similar situation. Japan wants to rebuild shipbuilding scale through the integration of Imabari and JMU. The United States wants Japan to help restore maritime industrial capacity. But Japan itself faces capacity, labor, and cost constraints. Japan still has engineering tradition and shipowner resources, but it is already difficult for it to recover its former central position in the face of global incremental orders. Shipbuilding competition increasingly looks like a system-level contest. The technical accumulation of a single old industrial company is not enough to compete against a complete supply chain, a huge order pool, and continuous engineering iteration.

China’s high-prosperity shipbuilding cycle therefore carries broader global meaning. It shows that China’s manufacturing competitiveness is expanding from consumer goods, electronics, and mid-to-low-end machinery into large and complex system equipment. Ships are the underlying infrastructure of global trade. They are also the maritime carriers of energy, automobiles, grain, minerals, military logistics, and global supply-chain operations. When Chinese yards capture most of the world’s new orders, China gains more than export revenue. It gains deeper participation in global logistics, energy transition, and maritime industrial infrastructure.

Shipbuilding is also an important entry point for understanding China’s industrial capability. It is not as light as consumer internet, not as attention-grabbing as AI models, and not as close to ordinary consumers as new-energy vehicles. But it more clearly shows whether a country can organize heavy assets, long cycles, multiple disciplines, many suppliers, and regional service networks over the long term. China’s shipbuilding order boom today comes from decades of industrial accumulation, engineering learning, supply-chain construction, and global customer validation. When shipowners place orders, they evaluate delivery, cost, quality, emissions, finance, maintenance, and future fleet-operating risks. Chinese yards can answer these questions at the same time. That is the most important industrial signal of this cycle.

The global transition toward green shipping is creating a new fleet-renewal cycle, and China is becoming the most important manufacturing infrastructure of that cycle. South Korea will continue to remain strongly competitive in high-end vessel types. Japan will continue to possess traditional engineering experience. The United States will continue to use trade policy and allied cooperation to push for shipbuilding reshoring. But judging from current orders, capacity, vessel-type coverage, green-vessel share, and supply-chain organization, China’s shipbuilding industry now stands at the center of the global reorganization of maritime industry.

Source note: This essay is based on recent Chinese media reports and industry coverage from China Association of the National Shipbuilding Industry, China News Service / China Industrial News, CCTV, People’s Daily Overseas Edition / Xinhua, Science and Technology Daily, China Daily, OECD, Reuters, and USTR on China’s shipbuilding orders, ship exports, green vessels, shipyard production schedules, Korean and Japanese shipbuilders, and U.S. maritime industrial policy. All translations of short quoted phrases are my own.

Bonjour Leon

Votre site est très prolifique et très argumenté.

Je vous en remercie.

Vous serait-il possible de faire un article sur le domaine de l'aéronautique civile ?

Le développement de la société Comac et le C919 et ses programmes dérivés sur d'autres modèles d'avions:

* les contraintes liées aux restrictions techniques occidentales:

réacteurs ( Général Electric , Pratt et Witney , Snecma en France , ..) par exemple

* les systèmes embarqués d'avionique ( Thalès et autres , ....)

* les développements en cours sur l'autonomie des composants majeurs comme le CJ-1000A en substitution des réacteurs LEAP 1C de GE/Snecma

* les certifications aéronautiques internationales en cours et contraintes associées

* les programmes commerciaux en cours ( Raynair semble intéresser par le C919 )

avec le marché intérieur chinois et le potentiel à l'exportation.

* la montée en cadence de production sur de C919 ( équivalent A320 Neo ou B737 max)

* la montée en Recherche et Développement des nouveaux modèles équivalent A330 , A350 , Dreamliner

* autres ......

Une dernière info :

j'ai un ami très proche qui a travaillé sur le développement de l'ensemble des programmes allant de A300 ==> A380 qui me disait il y a 10 ans que la concurrence à Airbus et Boeing viendrait de Chine .

Encore merci pour votre site